I’ve been an Infratil [NZX:IFT] [ASX:IFT] shareholder for the good part of a decade. As a value investor looking for balance sheet assets that deliver growth with income, it’s hard to look past this Company’s dynamic stable of infrastructure assets.

The acquisition, divestment, and management strategy has also turned out to be pretty good. During the time I’ve owned the shares, I’ve watched the Company make an excellent profit on Z Energy [NZX:ZEL] when it sold its 20% stake for $6 per share in 2015.

I’ve also seen it divest from ANU Student Accommodation, NZ Bus, Perth Energy, Snapper, and Aspire Schools over the past year.

When I first got into Infratil, more than 50% of the business was made up of its controlling stake in Trustpower [NZX:TPW]. It then had Wellington Airport, Australian Energy, NZ Bus, and a few others. Back in those days, it targeted an after-tax return to shareholders, over the long-term, of 20% per annum.

In the five years to 31 March 2016, it did just under 18% on an annualised basis. Including dividends, which were generally around 5%.

These days, the Company says (in its last Investor Day presentation) that it targets a return of 11% to 15% per annum.

The business has also become more diversified. But it has taken on some arguably more risky infrastructure investments.

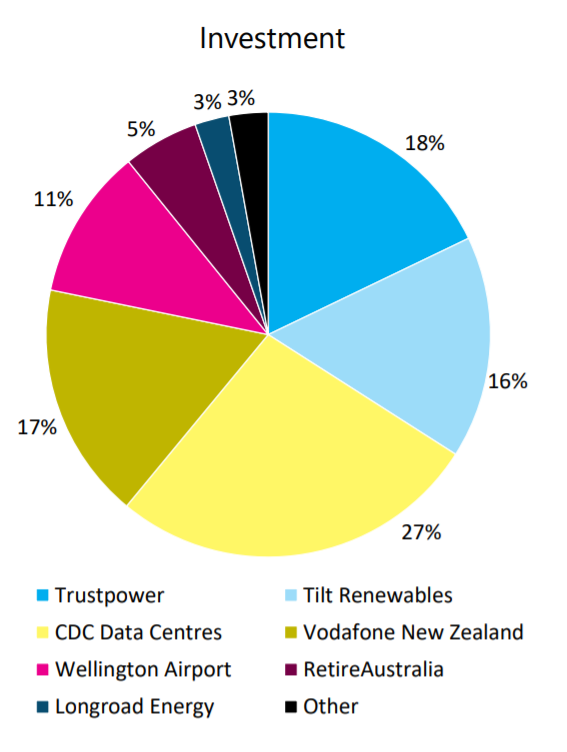

This is how its portfolio currently sits:

Source: Infratil Annual Meeting Presentation, August 2020

I was happy to participate in the capital raise last year to purchase Vodafone. And the share purchase plan in June to help provide more balance sheet flexibility to take advantage of development opportunities across the portfolio.

With some 37% of the portfolio now in renewable energy, Infratil also ticks some ESG boxes for many investors.

But there were also a few resentments with the Company, in my book. Targeted returns were reduced. While the overall risk profile seemed to have increased. Meanwhile, shareholders pay the Manager (H.R.L. Morrison & Co) significant management and performance — or incentive fees, as they call them.

These fees were set back in 1994. Earlier this year, major shareholder, the ACC, questioned the fairness of the fee structure. The management fee ranges from 0.80% to 1.125%, based on company value. The incentive fee is 20% of excess performance over a hurdle rate of 12%, applying to only non-NZ assets.

A November report by Fidato Advisory found that management base fees were in line with what other comparable funds charged. And that the hurdle rate was actually higher. While other funds assessed performance on all assets (not only those outside NZ).

On balance, I am more comfortable with the fee structure after this report.

But what is most pleasing is that the strategy we are paying for and the increased risk being taken is delivering. Not only by the conventional metrics, but as recently recognised by a big Australian super fund.

Why has the Infratil [NZX:IFT][ASX:IFT] share price risen?

At the time of writing, the Infratil share price is up nearly 20% in a single day. Australia’s largest superannuation fund — AustralianSuper — has made a cash offer of $7.43 per share, revised upward from a previous offer of $6.40. This revised offer represented a 22% premium on the previous share price of around $6.10.

Here’s what CEO Marko Bogoievski said in response:

‘Both proposals were unsolicited and materially undervalue our significant renewable energy and digital infrastructure platforms. We expect some of the additional value to be demonstrated in the near term with the recently announced strategic review of Tilt Renewables, which will continue, and ongoing appreciation of the value of CDC Data Centres’.

Where could Infratil [NZX:IFT][ASX:IFT] go from here?

The Company had a relatively successful FY20, showing a 13.5% growth in underlying EBITDAF.

Even after the big jump in share price, it trades on a P/E of around 23 and a P/B (price to book value) of around 2x. This does not seem unreasonable when portfolio assets could offer further growth — as the upcoming strategic review suggests.

Perhaps AustralianSuper wanted to tempt management with an offer before this review gets underway?

Since Infratil is now such a large part of my portfolio, I struggle to allocate further into it. Without overstepping my personal diversification guidelines of no more than 10% in a single business. Though you could argue that Infratil is really multiple businesses.

There is clearly more potential in Infratil’s current mix. Not only with Tilt and CDC, but also in Vodafone — poised to benefit from 5G. Plus, there’s recovery and potential development upside in Wellington Airport. And many of these interests are controlling interests which add further potential and premium.

Infratil has driven a fine road in delivering — and now exceeding the long-run shareholder returns it has been promising. Of course, past performance cannot guarantee the future. And the risk profile seems a little higher than I originally signed up for.

But you don’t get something for nothing.

Regards,

Simon Angelo

Editor, WealthMorning.com

PS: Infratil pays its interim dividend on 15 December 2020 (ex date 30 November) of 6.25c per share. Are you looking for more opportunities that could offer income and growth from quality assets? We are currently reviewing 20 more in our Lifetime Wealth Investor Portfolio.

(This article is general in nature only and expresses the author’s personal view. It should not be construed as any investment advice. Please seek independent advice for your own situation.)

![]()

Already a Member? Sign In Here

Simon is the Chief Executive Officer and Publisher at Wealth Morning. He has been investing in the markets since he was 17. He recently spent a couple of years working in the hedge-fund industry in Europe. Before this, he owned an award-winning professional-services business and online-learning company in Auckland for 20 years. He has completed the Certificate in Discretionary Investment Management from the Personal Finance Society (UK), has written a bestselling book, and manages global share portfolios.