Turners Automotive Group [NZX:TRA] [ASX:TRA] will be known to many readers who have bought and sold cars over the years. The Company provides automotive retail, finance, and insurance services. It is mostly known for its car auction business.

Turners has a market cap approaching $200m. The Group was formed in 2014 through the merger of Turners Auctions — New Zealand’s largest vehicle and machinery retailer — with Dorchester Pacific, a consumer finance and insurance business.

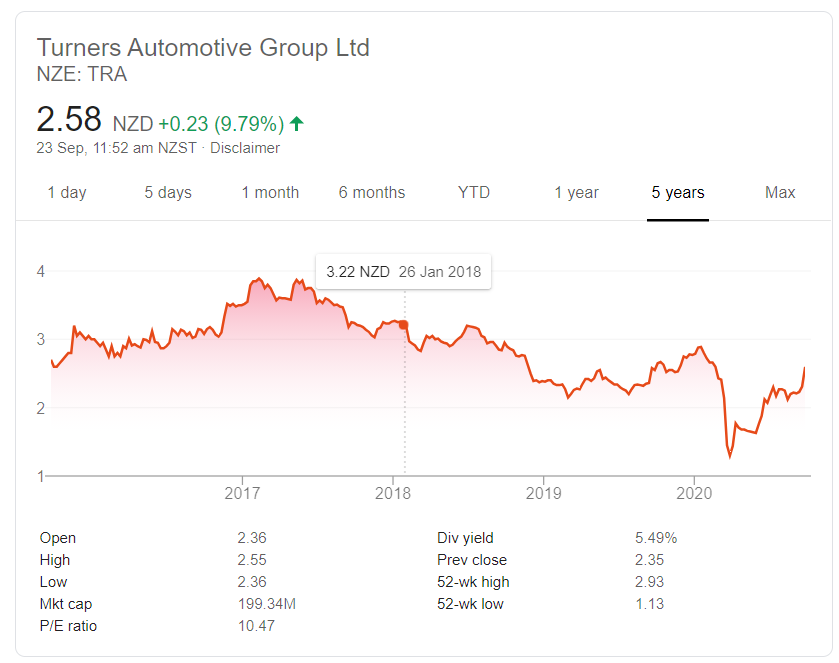

The share price experienced a dramatic plunge during the worst of the coronavirus fears in mid-March. It has since recovered from a low of $1.13 to around $2.58 today.

Why has the [NZX:TRA] [ASX:TRA] share price risen?

Today, Turners held its virtual annual meeting. The presentation made available to the market summarises the progress the Group has made over the past year:

- ‘Robust’ improvement in earnings and dividends was reported.

- According to the company, Turners has the 3rd highest dividend yield currently on the NZX. (Though we haven’t verified this — the payout looks to be only around 5.5% p.a. on current price).

- Used car sales demonstrated strong resilience following COVID-19 lockdowns. Turners is a trusted brand in the marketplace.

- The finance and insurance units contributed to the defensive nature of the business during lockdowns. Since they continued to provide annuity income.

- Although FY20 revenue was down –1% YoY to $332.7m, underlying net profit before tax (NPBT) was up +11% to $28.8m.

- Guidance for FY21 NPBT (net profit before tax) to be in the range of $28m to $31m. ‘Conditional upon no further substantive lockdowns occurring before year end.’

Where could [NZX:TRA] [ASX:TRA] go from here?

Turners appears a very well-run business that has structured itself into a defensive and profitable group. It is a business that many investors may have overlooked due to its small market cap. And also a mistaken belief that a lot of automotive retail and insurance trade has moved online.

In actual fact, buying or selling a car is a sensory experience. Being able to visit one of Turners’ nationwide locations provides an effective and efficient customer experience.

The stock is reasonably priced at a P/E ratio of around 10. The dividend yield and policy is attractive. The demonstrated resilience to economic downturn is favourable. Book value per share looks to be around $2.60. Net margins around 8%. And return on equity around 10%.

Net debt to equity sits around 95% — though this has come down in recent years.

However, this is not an entirely sunny story. Since early 2017 — when the share price was around $3.80 — Turners shareholders have seen awful erosion of value to the March low of $1.13.

Source: Google Finance

Now, the business seems to be on a recovery track. Certainly, it could have been a great buy in March. Will the growth story continue? Next year’s stable guidance with little NPBT increase suggests this is a yield story as opposed to a growth one.

Personally, I like the business. But for the risks inherent in any small cap, I’d probably be hoping for a bit more growth at the current earnings price.

Regards,

Simon Angelo

Editor, Wealth Morning

PS: There are some growth and income companies we like even better. Do check out our Lifetime Wealth Investor research newsletter:

![]()

Already a Member? Sign In Here

Simon is the Chief Executive Officer and Publisher at Wealth Morning. He has been investing in the markets since he was 17. He recently spent a couple of years working in the hedge-fund industry in Europe. Before this, he owned an award-winning professional-services business and online-learning company in Auckland for 20 years. He has completed the Certificate in Discretionary Investment Management from the Personal Finance Society (UK), has written a bestselling book, and manages global share portfolios.