I filled five sickness bags by the time we reached Douglas in the Isle of Man. The captain had slowed the ferry to counter the swell in the Irish Sea. And a nun sitting across from us declared it the worst sailing ever.

Crossing times can be much longer in rough seas. Source: Isle of Man Guide

We arrived on the island about 8.30pm.

There was an envelope waiting for us at the port desk. It had a key for the rental car which was in the parking lot outside.

‘You may need to fill it up,’ the man from the ferry company said. ‘They don’t start with much fuel, and the stations on the island close at 9pm.’

It was frozen outside and blowing a gale. We had at least a half-hour drive over the infamous mountain road to our accommodation in the north.

I hurried my wife and two children — then 7 and 2 — to the car outside. We found a petrol station in Douglas, and I filled the Mitsubishi ASX.

Now, in the Isle of Man, there is no distinction between the petrol and diesel pumps. Exhausted after the ferry journey and without instruction to the contrary, I filled the vehicle with petrol.

The wrong fuel

We left the town of Douglas. There is low taxation on the Isle of Man and perhaps as a consequence little road lighting. You are soon plunged into a chilling, wind-blasted darkness.

Then the Mitsubishi started to cough and splutter. A heavy burning smell wafted through the vents. The accelerator under my foot felt connected to a dying, heaving animal.

And the penny dropped. This was a diesel. I’d filled it with petrol!

I prayed. And turned into a dark country driveway.

No problem. We both had our mobiles. We’d call the rental-company breakdown number.

But since leaving England, our roaming Vodafone mobiles had failed to find any network. Then I recalled — they no longer covered the Isle of Man!

It was pitch-black. We were tired, frozen and stranded. There was a house with a light on at the top of the driveway. I walked up and knocked on the door.

As it happened, I’d turned into the right driveway. The owner ran a fuels business. And he knew the owner of the rental-car company. We arranged a taxi to the airport, picked up a tiny Ford Fiesta, and left the Mitsubishi to be salvaged.

Financial aftermath

In tricky situations, sometimes it’s just one person, one thing, one length of rope that saves you.

Yet — now hanging over me on that week of holiday — was what we might be up for to fix the Mitsubishi. Worst-case scenario, replacing the vehicle at a cost of around £15,000!

It was my fault. I’d put the wrong fuel in. This was not covered by insurance. But then nobody had told me it was a bloody diesel!

By the time we fronted at the rental-car desk at the end of the week, I’d prepared my case. They had to take some blame for the manner in which the car was supplied. We settled on half each over the £600 costs suffered flushing out the engine.

It could have been much worse.

I try to live by a simple motto. One that is very relevant for finances. And many complex situations in life.

‘Any situation can be improved by positive action.’

You can’t always take direct action. Sometimes you’re waiting for other people or a situation to evolve. Or there’s an obstacle in your way.

Your best action at this point is to make a plan. With action and a good plan, you can sleep easy. Maybe avoid the pump of worry that can burn out the engine.

When it comes to finances, we’re all in charge of our own journey. There are many unknowns. How a business or job will pan out. Whether investments will meet expectation. The ever-blowing winds of risk and change that can topple wealth or rocket it forward.

So you should make a plan. One robust enough to get you across whatever mountain road life may hold. And there are a few key things I’ve learned over the years that can help.

1) Begin with a specific financial destination

When we set sail on the Irish Sea, we were delayed hours. Then the car blew up. Everything went wrong. But we had a destination in the form of warm accommodation waiting near Bride. With a late supper of bacon and eggs from the farm.

A great financial plan starts with a clear destination in mind.

- Where do you want to live?

- What sort of lifestyle do you want?

- How much income will you need to support that?

- What ‘capital events’ do you want to cover?

Capital events cover large costs. A new SUV. Paying your daughter’s wedding. Helping your son into medical school.

As you would do with planning a trip, draw up the destination and cost it out. From where you currently stand and what you currently have.

Measure things with numbers. How much is needed to buy a home? To give you a passive income to support your lifestyle?

If you can preserve and grow your capital, future earnings may build to cover capital events.

2) Work out your capital allocation and do a financial stress test

Risk for a lot of people is a bit like your first girlfriend or boyfriend. You never understood them. And then it didn’t work out.

In New Zealand, most amateur investors we come across get focused on rental property. Returns over the past decade galloped — at least by capital gain. And property may be leveraged — generally more than stocks.

But in a low-interest rate environment, you may not be considering all the risks.

When looking at any new investment, do some stress-testing.

Here are some key stress areas you may like to consider:

- Mortgage or margin lending rates increase by 20%, 50% or 100%+

- Your rental property is vacant for 1-to-6+ months

- Your rental property is damaged and the tenant disappears

- The stock market experiences market drawdown of 20%+ (market crash)

- An invested company gets into difficulty and the stock plummets

- Dividends get reduced or cut

Once you run a stress test over your individual situation, you can work out how much you can bear. And how to mitigate the stress.

With stocks, we use diversification.

Concentrated high-conviction portfolios can generate the highest returns — but also concentrate the risks.

Stocks also provide a lot of ways to diversify. You can do it by country and region. By industry sector. By size of business.

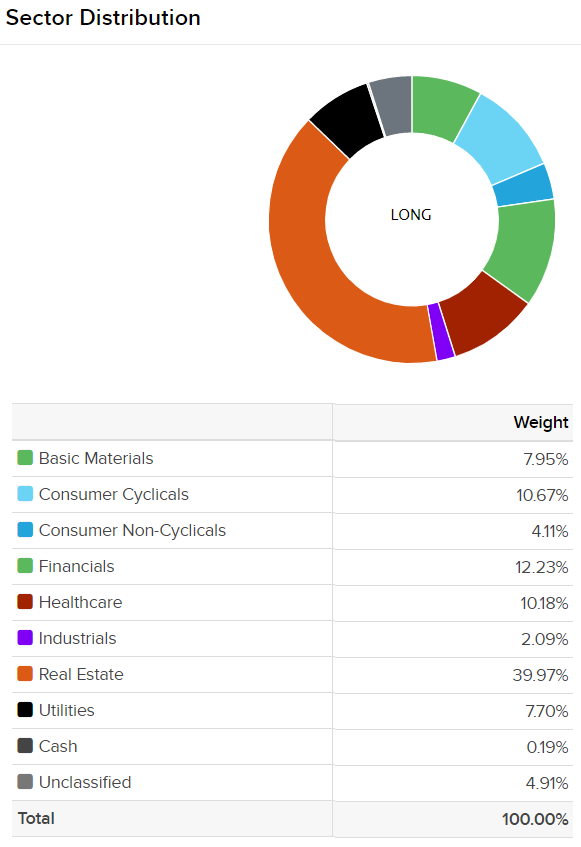

Here is a sample allocation for a global, income-focused portfolio:

Return in 2019 (capital appreciation + dividends) = 21.19%

[Note: for more exclusive details on how you can build a premium portfolio like this one, please visit our Lifetime Wealth Investor programme. There’s never been a better time to get started!]

Our portfolio has a current focus on Europe (59%) and Australasia (28%), taking advantage of opportunities based on a global developed-market remit.

It is skewed to real-estate-based companies due to market opportunity this year and a target yield of 6.5% p.a. With the expected rise of property markets (for example post-Brexit), the investors may take profit and rebalance the portfolio in coming years.

This strong growth has occurred in a low interest-rate environment.

Remember: with shares, rising interest rates are often the enemy of the stock market. Generally, the market will fall when interest rates increase.

And rising interest rates could have dramatic negative effect on highly geared property markets. Such as in New Zealand and Australia.

3) Develop a high-conviction financial strategy and invest opportunely

The financial plan mentioned above is for a family trust and its beneficiaries. It is focused on:

- Holding a comfortable family home debt-free.

- Targeting income (6%+ p.a.) and opportune growth (6%+ p.a.) from a globally diversified, high-conviction, managed-risk stock portfolio.

- Possibly using some lending margin to acquire another lower-cost property with maintenance income and for potential family use.

- Using income as needed to enjoy a desired lifestyle while not touching the capital.

Now, in this example, the investors could add risk with a more aggressive, leveraged approach. But this goes beyond what’s needed for their desired destination. Which makes heightened risk questionable.

Wealth beyond a certain level has slim correlation with happiness.

Hopefully this can give you some starting points to consider your own financial plan. And maybe begin the conversation with an independent advisor.

Whatever starting point you’re at, a clear vision of your destination and a sustained plan can help get you there.

This does not necessarily guarantee you a smooth journey. But it does help give you the freedom to choose one.

Regards,

Simon Angelo

Editor, WealthMorning.com

Disclaimer:

This article is general in nature and not intended to provide any financial or investment advice. Please speak to an Authorised Financial Adviser to discuss your unique situation.

Simon is the Chief Executive Officer and Publisher at Wealth Morning. He has been investing in the markets since he was 17. He recently spent a couple of years working in the hedge-fund industry in Europe. Before this, he owned an award-winning professional-services business and online-learning company in Auckland for 20 years. He has completed the Certificate in Discretionary Investment Management from the Personal Finance Society (UK), has written a bestselling book, and manages global share portfolios.