I grew up in the 1980s, learning that inflation was a bad thing. It peaked as high as 18%. And home mortgage rates followed…

Wages couldn’t keep pace with rising prices.

We had a mortgage on our home. By the weekend, there wasn’t even enough left for Mum and Dad to buy an ice cream.

Then there was the run-up in the share market, leading to a brutal crash and wealth wipeout in 1987.

Looking back, it’s hard to see the attraction of some of those shares. With P/E multiples of 50 or more. Against bank interest rates as high as 16%, if I remember correctly.

But it was a feeding frenzy. With fear of missing out, nearly half the adult population plonked their money in shares, many knowing little about what they were buying.

Then, in 1990, the Reserve Bank Act took effect, targeting inflation within a 0-2% band. Outside of a petrol price shock in 2008 and GST increase in 2010, it’s been stable and within this band ever since.

And economies do need a little inflation — just not too much. We need Goldilocks inflation: neither too hot nor too cold. But, still, the bears come — which we’ll get to in a moment.

Why do we need some inflation?

Buy a home for $600,000 and take a $500,000 mortgage, you’re heavily indebted.

Almost subconsciously, you expect some price inflation over the long-run. Over 10 years, you’d expect your $600,000 home would climb in value to be worth perhaps $800,000. Now, your debt to equity position looks much better.

Had you bought that $600,000 home in Auckland 10 years ago, it could well be worth $1.2 million.

And holders of company stock require the same in their positions, even with no debt. You assume companies will raise prices and grow their business over time. And the share value and dividends will lift.

Of course, too much inflation and price instability becomes unmanageable. It feeds on itself to erode economic confidence.

Turning the coin

This past year, we’ve been heading in the direction of Europe. Inflation is no longer the major threat. There’s a far more sinister threat at play — deflation.

Where prices go backwards. Where your $600,000 home becomes only worth $500,00. But you still owe $500,000 to the bank!

The OCR has been cut to 1%, the lowest on record. Growth in the property market has hit pause…and Auckland has gone backwards. We have an ageing population. And a growing culture of compliance, red tape and tax burden on anyone who tries to build or produce.

This looks and feels like the Europe I left. Although business taxes, at least in the UK, were lower.

The Reserve Bank is lowering interest rates to try and tell people to go out and spend and invest.

But, as in Europe, they’re not realising that these savers and investors are traumatised. They’re traumatised by 1987 and by 2008. They’d rather earn a few measly percent in the bank and shore up their savings in case of another meltdown.

In Europe, many are happy to earn just 50 basis points on locked-up savings (0.5% per annum).

We have our own version of ‘being safe’ in New Zealand. We buy houses and rent them out. At least, if other markets crash, you’ve got a roof and probably a tenant.

And there’s upside in doing this, provided the property market keeps going up.

But, like all markets, it needs its fuel. Strong migration. Buyers from around the world. Willingness to lend. Demand exceeding supply.

Those factors have been at play over the past decade. But will they remain?

Foreign buyers have largely been shut out. The government is embracing a more sceptical approach to immigration. And banks are being forced to tighten up. Meanwhile, you hear of plenty of empty homes on the periphery of Auckland.

But the biggest threat is probably the old chestnut: where Kiwis start leaving in large numbers again to Australia. And this will happen if a global slowdown, led by China, starts upping New Zealand unemployment.

Price stability can be very fragile. The concerning factor is that even with low interest rates, we’re still not yet hearing of any major swing in confidence.

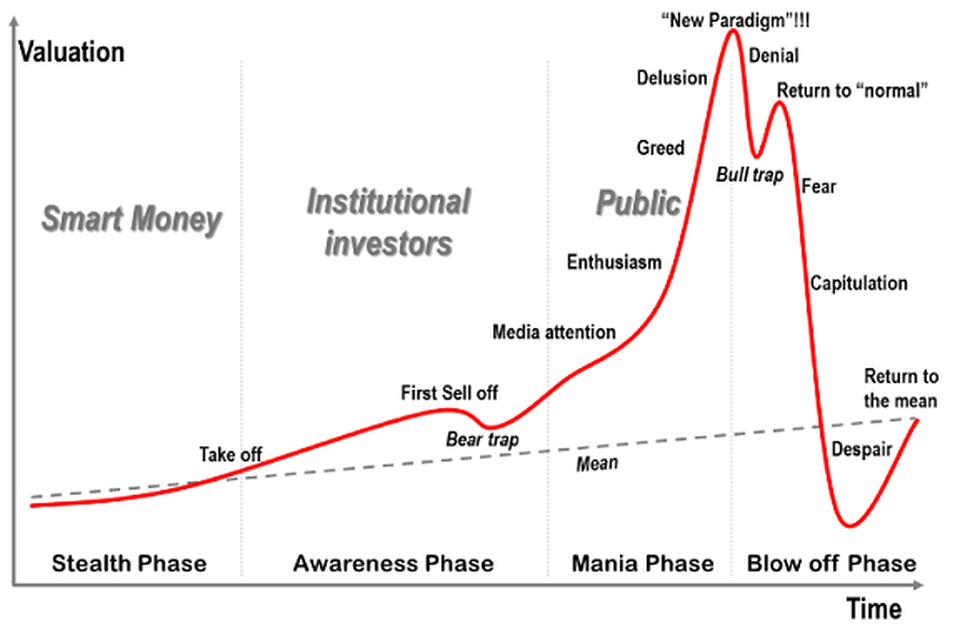

If we are now in a speculative property bubble, here’s the deflationary spiral that could come to pass:

This looks oddly like the Auckland run-up since 2002, with the ‘First Sell off’ in the ‘Bear trap’ of 2008. Reaching the ‘New Paradigm’ this year. Then a blip of upswing as we come out of winter.

In the end, there’s a final fall to fear.

Seems unbelievable?

In the mid-2000s, Ireland experienced a property crash, where values fell 75%. Vacant homes and estates were bulldozed.

Japan’s had two deflationary decades in asset markets. Many homes in Japan become valueless over time. Streets of empty housing are routinely bulldozed.

The economic forces behind inflation, deflation and population growth can be tenuous. And they can change fast in a small country.

Good investing comes down to finding margin of safety in whatever you buy. Because you make money when you buy.

Margin of safety is where the market price sits quite a bit lower than the intrinsic value.

Right now, I’m not seeing a margin of safety in Auckland property. But some people are seeing it in some distressed situations in the commercial and land space. And more of those situations may appear should market conditions continue to buckle.

But I’m not an expert on how to develop property to maximise its value. Nor do I have the time. And Auckland is just a minor world city in the greater scheme of things.

I like finding stocks around the world, where valuation and outlook offer some margin of safety. And, ideally, I look for those that pay a dividend while I wait for the value to be realised.

If I can target a running yield of 6% and see the upside of potential long-run capital growth of another 5-15% per year, I’m happy.

Of course, some risk is involved.

We explore these opportunities in our premium newsletter — Lifetime Wealth Investor.

Stay ahead of that curve.

Regards,

Simon Angelo

Editor, WealthMorning.com

Simon is the Chief Executive Officer and Publisher at Wealth Morning. He has been investing in the markets since he was 17. He recently spent a couple of years working in the hedge-fund industry in Europe. Before this, he owned an award-winning professional-services business and online-learning company in Auckland for 20 years. He has completed the Certificate in Discretionary Investment Management from the Personal Finance Society (UK), has written a bestselling book, and manages global share portfolios.