There’s a cost of money, you often forget.

‘Oh, I get it. You’re talking about interest? The cost of borrowing? Beware.’

No, it’s not a direct cost. But it’s very pertinent for investors.

Let me give you an example.

With summer around the corner, I’m looking forward to using more of our deck. BBQs. A glass of wine at the end of the day.

But this old deck is in need of replacement. Framing has started to rot. And the concrete tiles (not a good idea) are beginning to crack.

What does it cost in terms of money?

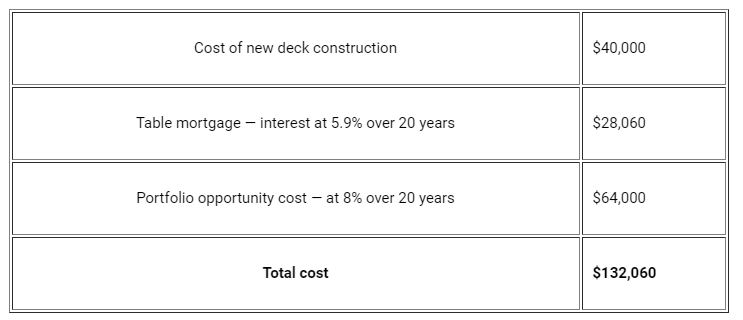

And so the quotes are in. The best I’ve received is around $40,000 to replace like for like, sans concrete tiles. Ouch.

Now, here’s the thing. Our portfolio over the last several years has produced an average annualised return of around 20%. Of course, there are no guarantees it may continue that in the future.

So let’s take a reasonable combination of dividends and some capital gain. Setting the target at 8% per annum.

The real investment in my deck involves an opportunity cost of $3,200 per year. Some $64,000 over the next 20 years, without even considering compounding reinvestment.

Thinking positive

‘Oh, but the deck will add value to your home, Simon!’

This is a line from the playbook of mortgage brokers and real-estate agents.

Yes, it will. But I won’t actually realise that value in terms of money until I sell. Or rent the property at a slightly higher yield.

Meanwhile, it produces no financial return at all. But it does subtract around $3,000 a year in opportunity cost.

Opportunity cost of money

This is what you give up economically in terms of money when you make one financial decision over another.

I could run $40,000 in the markets. Potentially generate $2,600 in dividends (at current running yield of the portfolio). Either watch that capital rise or fall — depending on the stocks and the market.

Or I could have a nice new deck.

In this case, I’m opting for the deck. While I enjoy investing and writing about it, I’m telling myself that refurbished outdoor space may give me more inspiration. And the ability to be more productive and profitable!

And so we justify our decisions. Especially when they cannot be measured in hard numbers alone.

All I’m saying here is before you make a financial decision — consider the opportunity cost. What financial opportunity are you giving up? And what is the overall cost of what you’re doing?

Remember, also, that debt will inflate all costs.

If I borrowed to pay for that deck, the total costs could be even higher:

Return on capital

To succeed in investing, you need to protect your capital and achieve the best possible return on it that you can.

In New Zealand, the biggest threats to personal capital are high housing, building and living costs — coupled with uneconomic debt.

In order to prop up economic growth, governments allow net migration to run at far higher levels than countries of similar size or development. Meanwhile, the housing stock can’t cope. Building and business activity is constrained by compliance and locked-up land.

Will prices in Auckland go up again? Or are they at bubble point?

Either way, housing affordability also needs to be assessed by the opportunity cost. If you want to buy a $1m house in Auckland, take my deck method above and run that across the purchase price.

Weighing things up

But you might say: ‘Wait! There’s the emotional consideration of owning your own home in a nice lifestyle city like Auckland. Better yet, in a nice part of Auckland. And there are high-paying jobs here.’

Well, consider what you’re working for. And perhaps consider the lines of Los Angeles poet Charles Bukowski, who described the equation thus:

‘How in the hell could a man enjoy being awakened at 6.30am by an alarm clock, leap out of bed, dress, force-feed, shit, piss, brush teeth and hair and fight traffic to get to a place where essentially you made lots of money for somebody else and were asked to be grateful for the opportunity to do so.’

Meanwhile, consider how you can get the best return on whatever capital you do have. And the risks involved obtaining that return. Optimise.

For now, my deck is due for demolition. And I will soon be staring into a large hole in the lawn. In preparation for the new. Ready to reinvigorate me with fresh ideas on investing and growing your capital.

Regards,

Simon Angelo

Editor, WealthMorning.com

PS: If you would like to learn how to trade shares and potentially build your wealth, we have just launched a new video-training module. Do check out our new Global Trading Masterclass.

Simon is the Chief Executive Officer and Publisher at Wealth Morning. He has been investing in the markets since he was 17. He recently spent a couple of years working in the hedge-fund industry in Europe. Before this, he owned an award-winning professional-services business and online-learning company in Auckland for 20 years. He has completed the Certificate in Discretionary Investment Management from the Personal Finance Society (UK), has written a bestselling book, and manages global share portfolios.