Are you a sports fan?

Well, if you are, then you already know this.

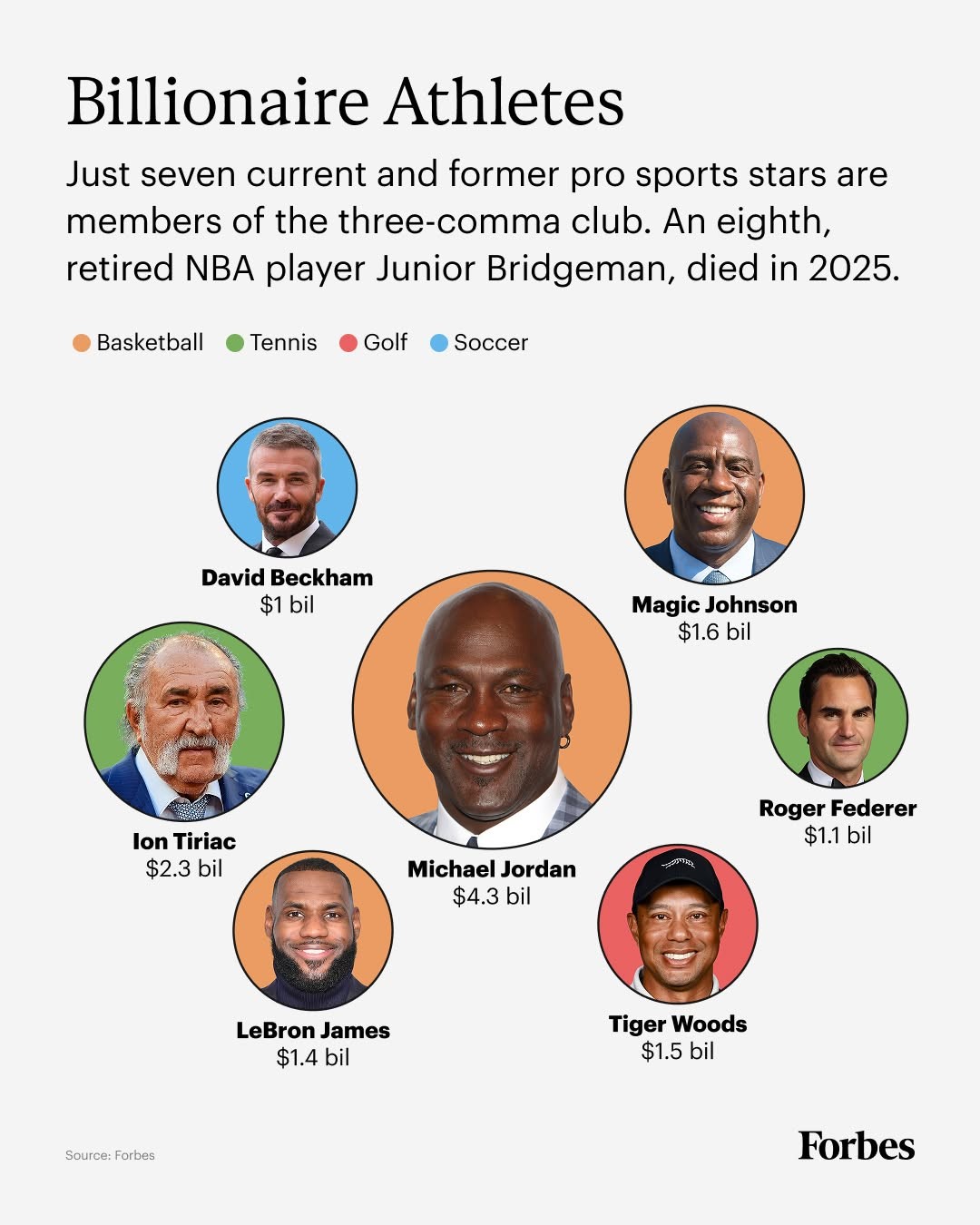

Michael Jordan is the wealthiest athlete of all time.

He has a net worth of $4.3 billion. That makes him richer than Tiger Woods. Richer than Roger Federer. Richer than David Beckham.

He beats them all by an astonishingly wide margin.

Source: Forbes / Facebook

Michael Jordan’s stellar career is well-documented:

- He enjoyed a 15-season run with the Chicago Bulls, where he developed a reputation for being able to deliver accurate shots from anywhere on the court. He was tough. He was resilient. He was adaptable.

- He won six championships, achieving a perfect 6–0 in the NBA Finals in 1991, 1992, 1993, 1996, 1997, and 1998. With 30.12 points per game, Jordan has the highest scoring average ever.

- More than any other player before him, you might argue that Michael Jordan was the man most responsible for turning basketball into a global sensation. His talent and charisma can’t be denied.

But I think this is the part of Jordan’s story that doesn’t get enough attention. At one point, his spectacular career was almost derailed:

- In July 1993, tragedy struck. His father, James, was shot dead by two men who robbed him of his car. It was a senseless murder.

- This loss seemed to shatter Jordan. He was coming off three straight championships, and he started to buckle under the pressure. His motivation to play basketball was gone. Who could blame him?

- So, in October 1993, at the age of 30, he announced his retirement from the Chicago Bulls. He was burned out. He was exhausted. This seemed to be the end.

What happened next was intriguing:

- In February 1994, Jordan decided to pursue a new career in minor-league baseball.

- Why? Well, his justification for this is quite revealing. He said: ‘I want to go and play baseball. It’s something that I’ve always wanted to do, and my father had always wanted me to do. So I’m just living his dream right now.’

- In other words, Jordan wanted to honour his father’s memory. He thought the best way to do it was by pursuing a sport his father had always loved.

- And so, over the course of 13 months, he played 127 games for the Birmingham Barons. He performed poorly by professional baseball standards. He only had a batting average of .202 and three home runs.

This was an eye-opener. Michael Jordan had gone from being a superstar to a nobody, seemingly overnight:

- A shocking change? Yes, absolutely. It’s worth noting that his superior athleticism allowed him to excel on the basketball court. But it didn’t do much to help him on the baseball field.

- I think the answer for this is quite simple: Baseball is a completely different game from basketball. It requires different muscle groups. Different skills. A different mentality.

Of course, Jordan was a smart guy. He quickly realised that he was getting nowhere in baseball:

- But, still, perhaps this experiment wasn’t a total loss. It did give him time to grieve. To reflect. To gain a fresh perspective.

- So, in March 1995, Jordan made his return to basketball. He said: ‘I’m back.’

- With renewed passion and energy, Jordan led the Chicago Bulls to three more championship victories in 1996, 1997, and 1998. In doing so, he cemented his legacy as an all-time great. What a comeback.

Michael Jordan in 1997. Source: Steve Lipofsky / Wikimedia Commons

Now, even though I’m not a basketball fan, I must admit that Michael Jordan’s journey is an inspiring one:

- I can totally relate to it. Because the lesson here is not just about sports. It also applies to the world of investing.

- When you’re choosing a long-term strategy, I think it’s worth asking the question: What game are you playing? And are you playing the game that’s best suited to your ability and personality?

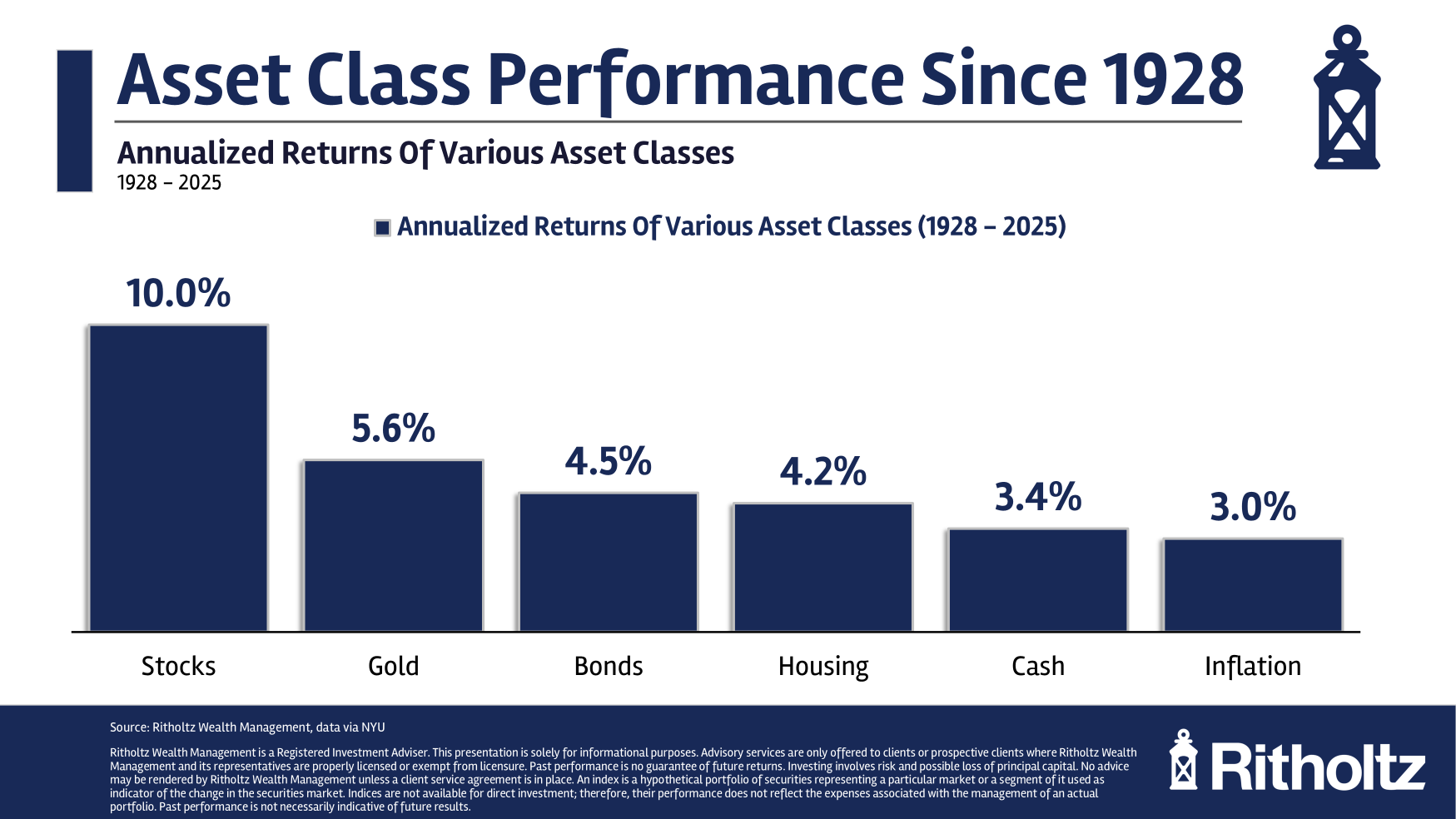

Source: Ben Carson / A Wealth of Common Sense

When you look back at a century of hard data, you can see the big picture. Different asset classes provide different levels of return:

- On one end of the spectrum, you have inflation. It’s been running at an average annualised rate of 3%.

- Meanwhile, at the other end, you have stocks. They’ve delivered an average annualised return of 10%.

- Then, in between, you’ve got everything else — gold, bonds, housing, cash.

Financial analyst Adam Kobeissi says: ‘Own assets or be left behind.’

- He hits the nail on the head, doesn’t he? If you sit by and do nothing, you’re allowing inflation to eat into your capital. Eroding your wealth. Destroying your buying power. You’ve already lost the game by default.

- Kobeissi is suggesting that you’re better off investing. The long-term numbers seem to back him up.

But wait. Numbers are one thing. Because when you’re talking about investing, you can’t ignore the other big factor, which is human emotion. This actually matters more than raw numbers. Here’s why:

- Some people are so risk-averse, so sensitive to volatility, that they can’t handle any kind of turbulence. They freak out any time they see a negative headline.

- This is the main reason why these people don’t invest. Sure, the long-term numbers may be compelling. But on an emotional level, they are nervous wrecks. They simply lack the confidence. They can’t bring themselves to commit.

Financial journalist Morgan Housel says: ‘You don’t need to know exactly what the future holds to know that some people will handle it better than others.’

- That’s so true, isn’t it? We all know that some people are simply braver than others. They have thicker skins. They can handle more stress. Therefore, the mileage that each person will get out of investing is going to be different.

- But having said that, is there a rational way to measure risk-taking? Well, yes, there is. We call it the risk-to-return ratio. It’s an equation that goes like this: How much risk should an investor take in order to get a potential return? It’s a matter of scaling up.

- So when you look at the different asset classes, this is why stocks have performed best over the long run. Stocks offer the highest possible ‘risk premium’. This means that investors are being paid a bonus to endure a higher level of uncertainty. This is how they can potentially capture higher returns. You might call it hazard pay.

Of course, I do recognise that not everyone has the stomach for volatility. The ability to bear it requires a certain level of mental toughness. Some people have it. Some people don’t:

- For example, I know of one person who panicked when Auckland property prices fell. The value of his house has plunged by over 30% in inflation-adjusted terms since November 2021. Lately, he seems to be afflicted with what war veterans like to call the ‘thousand-yard stare’. He’s emotionally devastated.

- Meanwhile, I know another person who has experienced multiple stock-market corrections over the years. I’m talking about drawdowns of 30–50%. But he doesn’t break a sweat. He keeps pushing on. Diligent and calm. Building his wealth through quiet compounding.

- It’s clear to me that everyone has different temperaments.

So I want to circle back to my original question: What game are you playing? And does it suit you?

- Please note that nothing I’ve said here should be construed as financial advice.

- My intention is for you to think more deeply about your understanding of risk, as well as your tolerance for volatility.

- After all, the investment journey is all about asking the right questions.

- Are you playing basketball? Or are you playing baseball?

We can create a game plan for you

Here at Wealth Morning, we run a night-trading desk. We focus on building up robust and profitable portfolios for our Eligible and Wholesale Clients:

- We seek to stay ahead of the curve and position our clients for income and growth for the next stage of the cycle.

- Are you interested?

Regards,

John Ling

Analyst, Wealth Morning

(This article is the author’s personal opinion and commentary only. It is general in nature and should not be construed as any financial or investment advice. Wealth Morning offers Managed Account Services for Wholesale or Eligible investors as defined in the Financial Markets Conduct Act 2013.)

John is the Chief Investment Officer at Wealth Morning. His responsibilities include trading, client service, and compliance. He is an experienced investor and portfolio manager, trading both on his own account and assisting with high net-worth clients. In addition to contributing financial and geopolitical articles to this site, John is a bestselling author in his own right. His international thrillers have appeared on the USA Today and Amazon bestseller lists.