With the property gravy train slowing in New Zealand, more and more investors are looking to shares to drive income and growth.

They often start with the local NZX — soon realising the opportunities are limited, with the best picked bare.

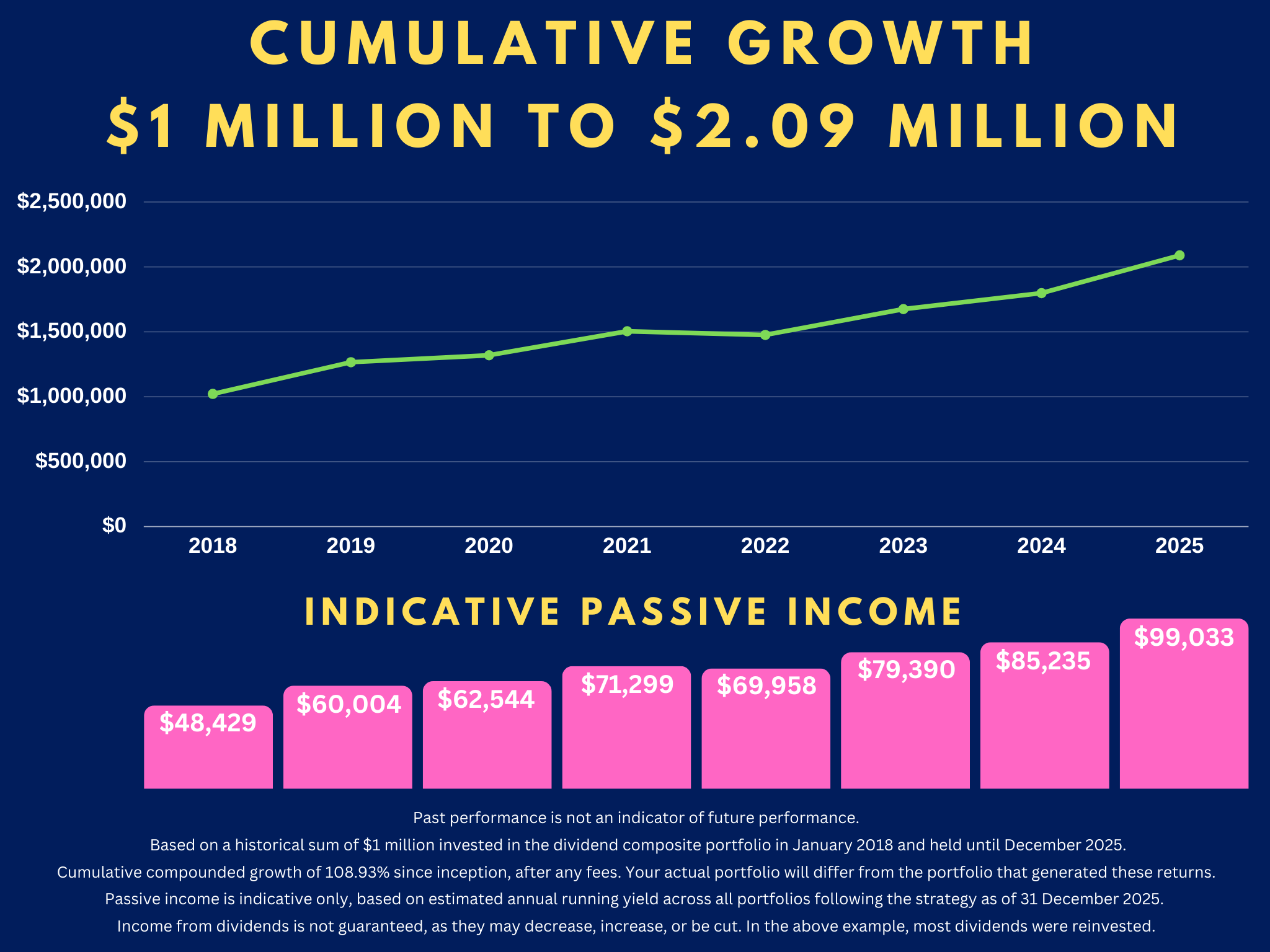

Global markets can turn the world into your oyster, with many exciting and resilient businesses.

Of course, this presents risk. Even in developed markets, selection and allocation require skill and experience. And it also means understanding the tax implications.

Here in New Zealand, once you have a significant portfolio of global equities, you’ll likely come under the FIF (Foreign Investment Fund) regime.

For many Kiwi investors accustomed to property, the FIF regime is unfamiliar. Some are put off by it simply because they don’t understand it. But once you look under the hood, what seems complex can actually reveal meaningful opportunity.

Tax optimisation, after all, is a key part of achieving financial independence.

How FIF tax works

For individual investors and family trusts, there are two main calculation methods:

- Fair Dividend Rate (FDR): Assumes a 5% return on the value of your global portfolio at the start of the tax year (e.g., 1 April).

- Comparative Value (CV): Calculates the actual gain or loss on your portfolio over the tax year.

Most investors use FDR, but the ability to switch to CV in certain years can be advantageous.

How can you optimise the FIF regime?

One approach investors consider is targeting an average dividend yield near the 5% FDR rate across their global holdings. In practice, this means:

- You are effectively taxed on what you would have paid for dividend income anyway.

- The tax payable under FDR is easily covered by the dividends received.

- Under current rules, any capital gains above that 5% deemed-return amount are not taxed.

This is where the upside lies. Some offshore REITs and other quality businesses, for example, currently yield above 5% and may be undervalued — making them particularly tax‑efficient under FDR.

In years when markets fall sharply — as we saw during Covid and again in 2022 — investors may be able to switch to the CV method and pay no tax if their portfolio shows an overall loss.

What about capital gains tax?

Labour has signalled its intention to tax capital gains on most rental properties. Once implemented, the scope could expand to shares.

However, the FIF regime is likely to remain outside any future CGT. The 2019 Tax Working Group recommended taxing capital gains more broadly, but it also stated:

‘The FDR method should be retained as the main method for taxing income from FIF interests… the fall in risk‑free rates of return since 2007 could indicate that a 5% FDR rate may now be too high.’

This suggests that FDR is seen as a stable, enduring framework — and possibly one that could even be adjusted downward over time.

Managed funds vs direct or managed-account investors

Many managed funds deduct FIF tax automatically, which is convenient. But direct or managed‑account investors may enjoy advantages that funds cannot offer:

- Funds generally cannot switch between FDR and CV, meaning they still pay tax on 5% of the opening balance even in a down year.

- Funds must use the average balance over the year, whereas direct investors use the opening balance — a clear advantage when markets rise.

- New direct investors often enjoy a ‘first‑year tax holiday’, since their opening balance on 1 April is zero. PIE funds do not offer this benefit.

These differences may improve long‑term after‑tax outcomes for direct or managed-account investors — depending on market conditions and their individual situation.

Wealth Morning Managed Accounts

For Wholesale or Eligible Investors seeking exposure to global markets, we develop resilient portfolios optimised for global taxation and mobility.

We are currently offering a free consultation to Wealth Morning readers.

Do request your free consultation here.

Regards,

Simon Angelo

Editor, Wealth Morning

Simon is the Chief Executive Officer and Publisher at Wealth Morning. He has been investing in the markets since he was 17. He recently spent a couple of years working in the hedge-fund industry in Europe. Before this, he owned an award-winning professional-services business and online-learning company in Auckland for 20 years. He has completed the Certificate in Discretionary Investment Management from the Personal Finance Society (UK), has written a bestselling book, and manages global share portfolios.