As investors, our mission is outperformance while managing risk.

It’s all very well to outperform for years, only to then find that the chickens have come home to roost on the risk front, and key positions crumble away.

A darling of the NZX on the outperformance front has been Infratil [NZX:IFT].

It began in 1994 as one of the world’s first listed infrastructure funds available to individual investors.

The late Lloyd Morrison, the founder, believed infrastructure investment had a profound ability to improve lives.

As an investment, the sector has also offered very strong risk management characteristics.

Originally from Palmerston North, Morrison started his investment career as an analyst with Jarden & Co. He went on to form investment advisory Morrison & Co in 1988, launching Infratil in 1994.

Morrison & Co remains the manager of Infratil today — arguably one of New Zealand’s most successful and enduring listed companies.

Sadly, Lloyd Morrison died of leukaemia in 2012 at the age of 54, survived by his wife and five children.

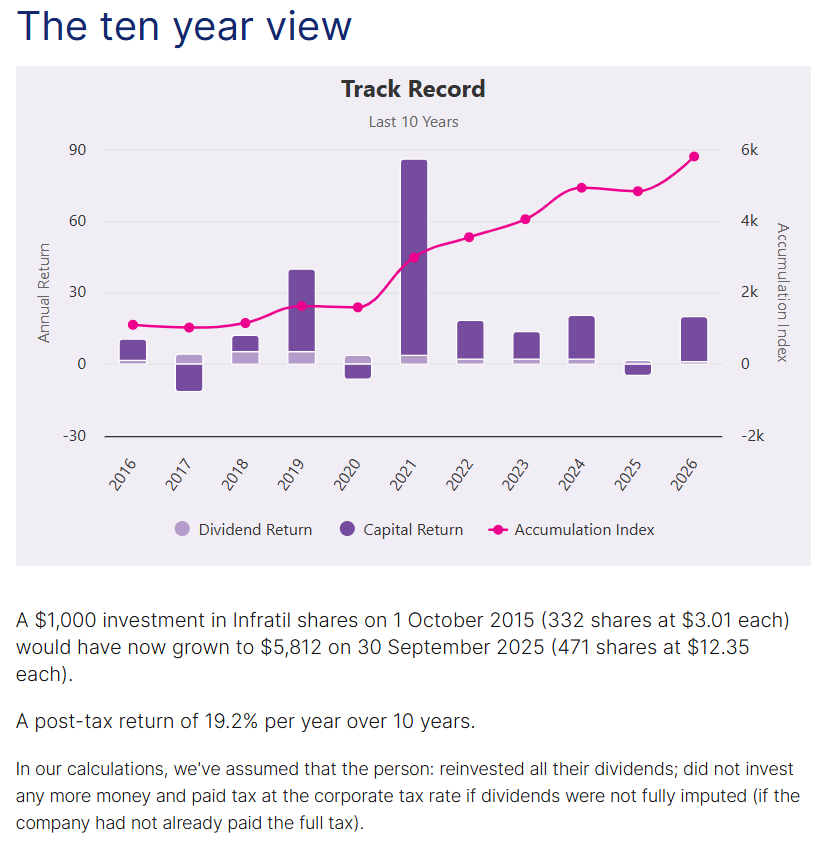

Over the years, I’ve continued to invest in Infratil. Today, it is my second-largest position, after an Italian real estate business. Its return over many years has been excellent:

Source: Infratil

These days, infrastructure investments are somewhat more competitive.

Over the past year, the stock has actually delivered over 18%, with a projected dividend of around 1.85%. Much of this came in the last month on the back of strong performance from CDC (Canberra Data Centres), where Infratil holds 49%. CDC signalled surging Australasian data centre demand, accelerated build out, and upgraded FY27 earnings guidance on the back of strong contracted capacity and geopolitical tailwinds.

However, it seems to me that with the increased digital infrastructure focus, the risk profile has also increased somewhat. Infratil previously had a 51% controlling stake in Trustpower, which made up around 23% of Infratil’s market cap (depending on share prices).

Since 2021, the business was already pivoting strongly toward digital infrastructure and renewables, with CDC Data Centres and Longroad becoming increasingly important drivers of valuation — far more than Trustpower, which was later demerged into Mercury and Manawa Energy.

Today, Infratil still has considerable power generation assets — including a 14.3% stake in Contact Energy [NZX:CEN].

This might deliver good, risk-managed growth based on the equity raise that took place in February.

These days, Infratil states: ‘We aim to deliver long-term shareholder returns of 11–15% per annum after tax, through a mix of share price increase and dividend returns.’

- They expect to achieve returns from the companies they invest in from 8% to 25%, using debt funding of 30% of assets at an interest rate of 6%.

- Most of their investments target 8% to 15%, with a smaller set of growth assets targeting 15% to 25%.

- Management costs each year (paid to Morrison, the fund manager) are around 1%.

- This enables the target return to shareholders of 11–15%.

Can Infratil continue to deliver these sorts of returns now that global infrastructure investment has become more competitive?

Are investors now taking on more risk to get these returns?

And what other diversified fund options compare?

Your first Quantum Wealth Report is waiting for you:

⚡🌎 Start Your Subscription: NZ$37.00 / monthly

⚡🌎 Start Your Subscription: US$24.00 / monthly

Simon is the Chief Executive Officer and Publisher at Wealth Morning. He has been investing in the markets since he was 17. He recently spent a couple of years working in the hedge-fund industry in Europe. Before this, he owned an award-winning professional-services business and online-learning company in Auckland for 20 years. He has completed the Certificate in Discretionary Investment Management from the Personal Finance Society (UK), has written a bestselling book, and manages global share portfolios.