I’d been invited to Eden Park to hear John Key speak. That must have been about 12 years ago.

We’d finished breakfast and taken our seats. The MC stepped up, but there was still no sign of the Prime Minister.

‘Take a look up there,’ the MC said.

Heads turned skyward. A helicopter swept low over the stands, touched down on the turf, and moments later, Key was on stage, jacket straightened, ready to go.

His speech was casual, almost off the cuff. He gestured to the empty seats.

‘Eden Park holds about 50,000 people,’ he said. ‘That’s roughly how many New Zealanders leave for Australia each year.’

Source: Kiwi Flickr / Wikimedia Commons

He’d turned a stadium into a measure of national loss.

Shortly after, I left with my family for Europe.

Yes, we wanted wider opportunity and more professional development. But there was something heavier too. We’d enjoyed good housing in New Zealand. Yet it was becoming clear that the same certainty might be out of reach for our kids.

We returned before Covid.

At first, it was a joy — reconnecting with family, settling back into the Kiwi lifestyle, rediscovering the small things we’d missed.

Then came the other side of that time: the economic wreckage left in the wake of a government whose approach felt overreaching and ideologically driven.

Having recently read David Cohen’s Jacinda: The Untold Stories, I’m left with the impression that certain individuals who came to power were dangerous activists.

Businesses closed. Livelihoods disappeared. Education suffered. Mental health fell through the floor. Decades of debt were heaped upon the next generation.

Such was the damage that radical courage was needed to turn the ship.

In 2023 a new coalition government received a resounding mandate to make change. Unfortunately, its lack of courage has been more disappointing than the Key years were.

After 12 years working in richer markets, the lesson is clear. Turning the tide on Kiwi inertia — and halting our drift down the OECD income league — demands one thing above all else: courage.

Source: Michael Arouet / X

Source: Michael Arouet / X

Never waste a good crisis: Time for a tax-free threshold

Nicola Willis has moved to blunt the fuel spike by offering $50 a week to around 143,000 working families, paid for up to a year or until 91‑octane petrol drops below $3 for four straight weeks.

It’s a temporary patch that could cost up to $373 million — with no structural benefit to the economy.

In effect, 3.1 million taxpayers are being asked to chip in about $120 each so a smaller group can receive $50 a week — a payment triggered by high fuel prices but not tied to actual fuel use. Many New Zealanders hit by the same spike will subsidise others who may not be struggling at all.

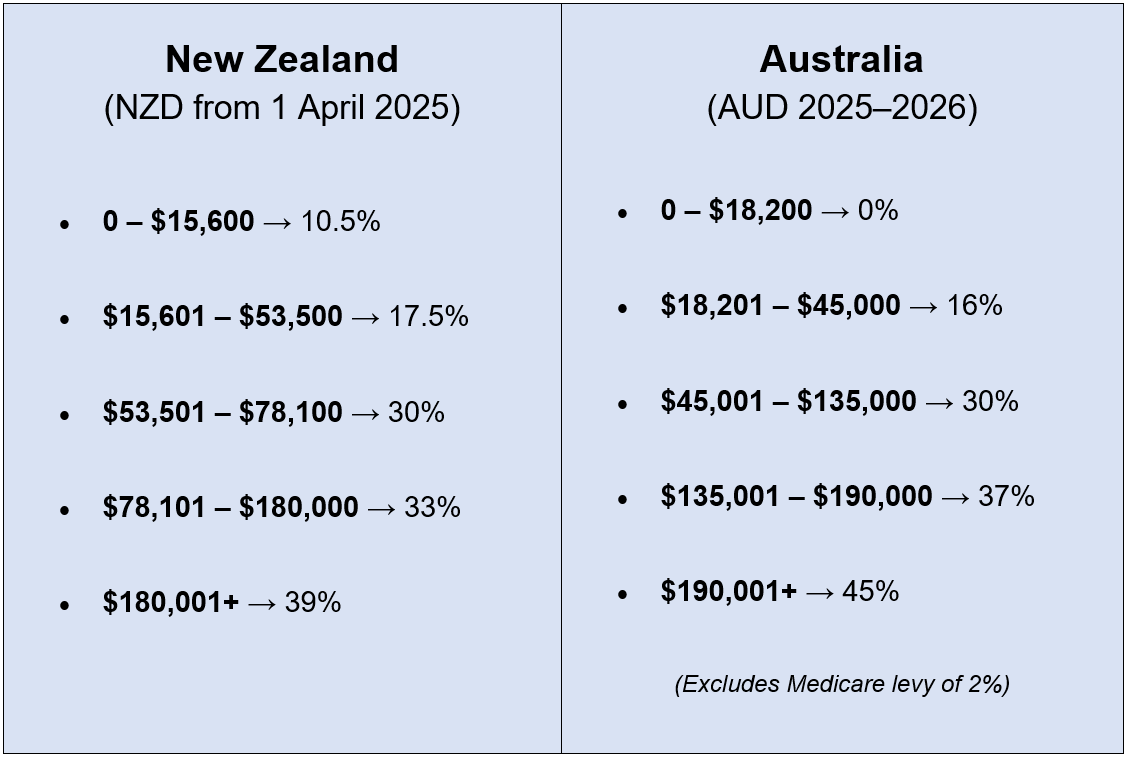

A far better response is structural: make the first tax threshold — the 10.5% band covering $0 to $15,600 — tax-free.

This would deliver permanent relief, reward work, and strengthen the incentives for people starting businesses or re-entering the workforce.

Tax what you don’t want, not what you do.

Yes, the 10.5% band represents roughly 10% of all personal income tax revenue. But that’s precisely why it’s powerful. Returning that money to low and middle-income earners doesn’t vanish. It recycles through the economy, lifting GST, supporting small businesses, and boosting labour force participation.

A tax-free threshold is not a cost. It’s a reallocation – from government spending to household and business dynamism. It improves incentives where they matter most: the first dollar earned, the first client invoiced, the first step back into work.

Australia understands this. Its tax-free threshold and wide middle brackets give workers far more take-home pay at the lower and middle end. That’s one of the quiet structural reasons Australia grows businesses and attracts talent at a scale New Zealand struggles to match.

New Zealand taxes work from the first dollar. Australia rewards it.

Eliminate the wastage campaigned upon

Some will argue that Australia can afford lighter income tax because it has a capital gains tax. But that logic collapses under scrutiny. Australia’s CGT sits alongside stamp duty and a heavy bureaucratic load — all of which suppress productive investment.

Non-mining business investment is weak, productivity growth is flat, and capital deepening has stalled. A CGT hasn’t saved Australia from structural stagnation.

New Zealand doesn’t need to copy Australia’s mistakes. We can improve productivity not by taxing more, but by spending less on what produces nothing. The solution is hiding in plain sight: eliminate the wastage successive governments have campaigned against but never confronted.

Last year, the Taxpayers’ Union identified potential savings of $35 billion. You don’t need to agree with every line item to accept the broader truth: Wellington has become a waste machine.

A tax-free threshold doesn’t require a revolution — just modest savings of around $5 billion. That’s a fraction of what even one serious efficiency review could uncover.

This is the real contrast with Australia. Their advantage isn’t CGT. It’s that workers keep more of their first dollars earned, giving them the confidence to spend, invest, and participate.

If New Zealand wants to stop losing 50,000 people a year, the answer isn’t subsidies or crisis cheques. It’s opportunity — the kind that starts with letting people keep more of what they earn, build more of what they want, and invest in a country that invests in them.

End the housing and migration scams

A lot of young New Zealanders leave because they fear they’ll never be able to buy a home here. They worry the Kiwi dream is dead. And they’re not wrong to worry.

Most New Zealanders don’t want their suburbs turned into bunker blocks with no parking, no sunlight, and no character. Yet that’s where current policy pushes us.

The focus must shift away from intensifying people into shoeboxes they don’t want, and toward unlocking land, reforming planning rules, and incentivising construction of single-family homes — the type of housing Kiwis actually aspire to.

Why does the government want mass migration and intensification?

Kiwis say not so fast. Source: Newstalk ZB / X

It makes no sense to bring in more people than the country can house, train, or absorb in short order.

The focus must be on quality — people with capital to invest or those with very high skills that the country genuinely needs.

New Zealand should be pro‑immigration — but selective. Our system is upside-down. An investor needs $5 million to come here, but someone can get a work visa from an ‘accredited employer’ running a vape shop, nail bar, or pizza outlet. After a few years, they may be supervising the pizza outlet and qualifying for residence.

This isn’t a skills strategy. It’s a loophole.

New Zealand needs fewer people in higher skilled areas, plus those investing significant capital. That’s how you lift productivity, wages, and housing affordability.

Become a true safe haven for capital

Having worked in offshore finance, I’ve seen firsthand what a low-tax, investor-friendly jurisdiction can do.

It meant a new state-of-the-art hospital under construction, generous funding for local university students, and a pipeline of high-value jobs.

When capital feels welcome, it builds things.

New Zealand is already a geographic safe haven. A fact that becomes even more significant as nuclear risks rise amid the Iran conflict.

Could we also be a financial safe haven?

Yes — but only if we set the right foundations. That means enabling tax neutrality for companies and trusts, supported by strong but light-touch regulation.

Tax neutrality simply means wealth can be based in New Zealand without being penalised. Today, we fall short of that. The FIF regime, for example, actively discourages globally invested people from bringing their portfolios here — even though local residents can still enjoy certain advantages under the current rules.

Company tax is one of the smallest contributors to our overall tax base. Reducing it — or moving toward a neutral structure — could attract far more financial activity than we lose in headline revenue. With the right settings, the system pays for itself.

The offshore experience is clear: when you create a competitive tax and regulatory environment, banks and other high-margin industries shift real activity — operations, teams, and investment. Think cloud computing firms, global marketplaces, R&D labs, asset managers, fintech, advanced manufacturing. These sectors seek stable, neutral, lightly regulated jurisdictions.

And once they arrive, capital follows capital.

That means more high-wage jobs here at home. Not subsidised jobs. Not temporary crisis cheque jobs. Real, durable, globally competitive jobs.

This is the long-term play New Zealand keeps missing. We have the geography, the stability, the rule of law — but not yet the policy settings.

Become a true safe haven for wealth and the benefits will compound for decades.

Regards,

Simon Angelo

Editor, Wealth Morning

(This article is the author’s personal opinion and commentary only. It is general in nature and should not be construed as any financial or investment advice. Please contact a licensed Financial Advice Provider to discuss your personal situation. Wealth Morning offers Managed Account Services for Wholesale or Eligible investors as defined in the Financial Markets Conduct Act 2013.)

Simon is the Chief Executive Officer and Publisher at Wealth Morning. He has been investing in the markets since he was 17. He recently spent a couple of years working in the hedge-fund industry in Europe. Before this, he owned an award-winning professional-services business and online-learning company in Auckland for 20 years. He has completed the Certificate in Discretionary Investment Management from the Personal Finance Society (UK), has written a bestselling book, and manages global share portfolios.