Monthly, we update our wholesale investors on what’s happening in the market. Running what’s probably the only late-night trading desk from New Zealand, we’re well-positioned to feel the pulse of the market’s direction.

We end the year of 2022 down 2.84%.

Not bad in the context that 2022 saw the worst sustained drawdown since 2008. When the GFC rocked financial markets.

Also, not bad in the context that property in Auckland fell 18.1%.

This country’s top KiwiSaver Growth fund was down around 9% (as of 30 November).

And our MSCI EAFE benchmark index was down 13.59%.

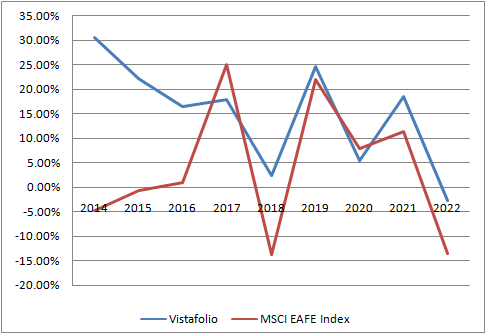

Against our benchmark, the Vistafolio model portfolio has outperformed the index since inception:

Outperformance of index: 100.18% (consolidated, since inception)

Vistafolio performance

For the month of December 2022, we were down 2.55% across the composite portfolio (total aggregate return across all portfolios following the strategy).

This brings our overall return for the year to –2.84%. And our average annualised return since inception at 14.91% p.a.

Please see our performance chart for more details.

![]()

💰 Our Exclusive Managed Account Service

👉 Click Here to Find Out More

A year in review

Let’s be fair. I’ve never seen a year with so much downside since the GFC.

Where do I start?

- We had to pay for the overbearing Covid response. Joyous alcoholic money printing ended up in rehab.

- That rehab saw interest rates spiking very fast, roiling markets.

- The Ukraine war stoked recessionary fear in Europe as jumping energy and food prices savaged households and industry.

- China’s economic growth slumped as it grappled with lockdowns and then a frightening run-up in Covid cases.

But the burn-off also revealed a lot of value we were able to target:

- Property-based stocks showed discounts of 20% to 60% on their underlying property values.

- Projected dividend yields on entry prices for our targets reached almost 7% in the UK alone.

- Many of our favoured targets were available at P/E (earnings multiples) of 10 or less.

I don’t see this much downside again for 2023.

By definition, it’s time to get in now for the inevitable upside:

- Average targets for the S&P 500 see that ending 2023 up 6% (based on a Bloomberg poll of 22 analysts).

- Two years of consecutive falls are extremely rare. With most bad news priced in, 2023 should see some good news getting priced.

- China’s easing of Covid rules might see supply chains bounce back.

- UK markets (where we are active) continue to present a value hedge. The FTSE 100 was steady this year and that outperformance could continue.

- Most economists see the Fed and other central banks easing up on rate hikes.

Well, British dustmen once famously out-predicted economists. And it’s tough to make predictions — especially about the future!

One certainty is volatility looks set to continue. Q1 could still head down as we wait on those easing interest rates.

Yet, on balance, the downside vs upside equation that jilted investors in 2022 is likely to reverse.

Which makes it a great time to invest now.

If you already hold an account with us, I encourage you to add more funds so we can put them to work.

Those who have funds available for investment across the market cycle tend to capture the most opportune results.

If you don’t have a portfolio with us and would like to try a managed account, I encourage you to review this option in more detail.

2022 got tough and dark for everyone.

2023 shows a clear, bright light at the end of the tunnel. Especially for long-run value seekers.

I’m looking forward to it. I’m licking my lips.

Happy New Year!

Regards,

Simon Angelo

Editor, Wealth Morning

Past performance is not an indicator for future performance. Your actual portfolio will differ from the composite portfolio mentioned. The information contained in this document does not constitute an offer to sell or a solicitation to buy an investment, nor should it be construed as investment advice. Vistafolio investment services are available to Eligible Investors and Wholesale Investors (not to Retail Investors) as defined in the Financial Markets Conduct Act (2013).

Simon is the Chief Executive Officer and Publisher at Wealth Morning. He has been investing in the markets since he was 17. He recently spent a couple of years working in the hedge-fund industry in Europe. Before this, he owned an award-winning professional-services business and online-learning company in Auckland for 20 years. He has completed the Certificate in Discretionary Investment Management from the Personal Finance Society (UK), has written a bestselling book, and manages global share portfolios.