Got a spare moment?

A simple pleasure for me is a pain au raisin and cappuccino. It reminds me of my time in Europe.

The pastry is not quite as good here in New Zealand. But the coffee makes up for it.

Sometimes I pop into a French café a few suburbs north of my home. Looking forward to this treat…

Source: Erasmusu

One Monday, I am confronted with the café in darkness.

There’s a handwritten sign from the owner taped to the glass:

‘I am 63 years old. I cannot continue working 60 hours a week for the equivalent of less than $15 an hour. I cannot find the staff I need. Sadly we will now close on Mondays…’

While this is disappointing, it relates to a key question people keep asking me…

‘Is a recession coming?’

Technically, we’re in recession following two negative GDP quarters.

So, in New Zealand, not yet. We’ve only had one negative quarter.

The definition of a recession I prefer is: ‘When your neighbour loses his job.’

A depression, according to Harry Truman, was ‘when you lose yours’.

Perhaps, you may think, a recovery is when Grant Robertson loses his?

But is there anyone with any better ideas to take his place?

On whether a recession is coming in the US, Federal Reserve Chair Jerome Powell has said, ‘It’s a possibility but not inevitable.’

But central bankers don’t seem to really know, do they?

Back to my favourite French café…

I call in on a Tuesday. It is full. All the seats are taken. The staff are swept off their feet.

It’s hard to see a recession coming when businesses are humming and there is a shortage of workers.

A normal recession sees people losing their jobs.

Right now, we see many businesses crying out for workers.

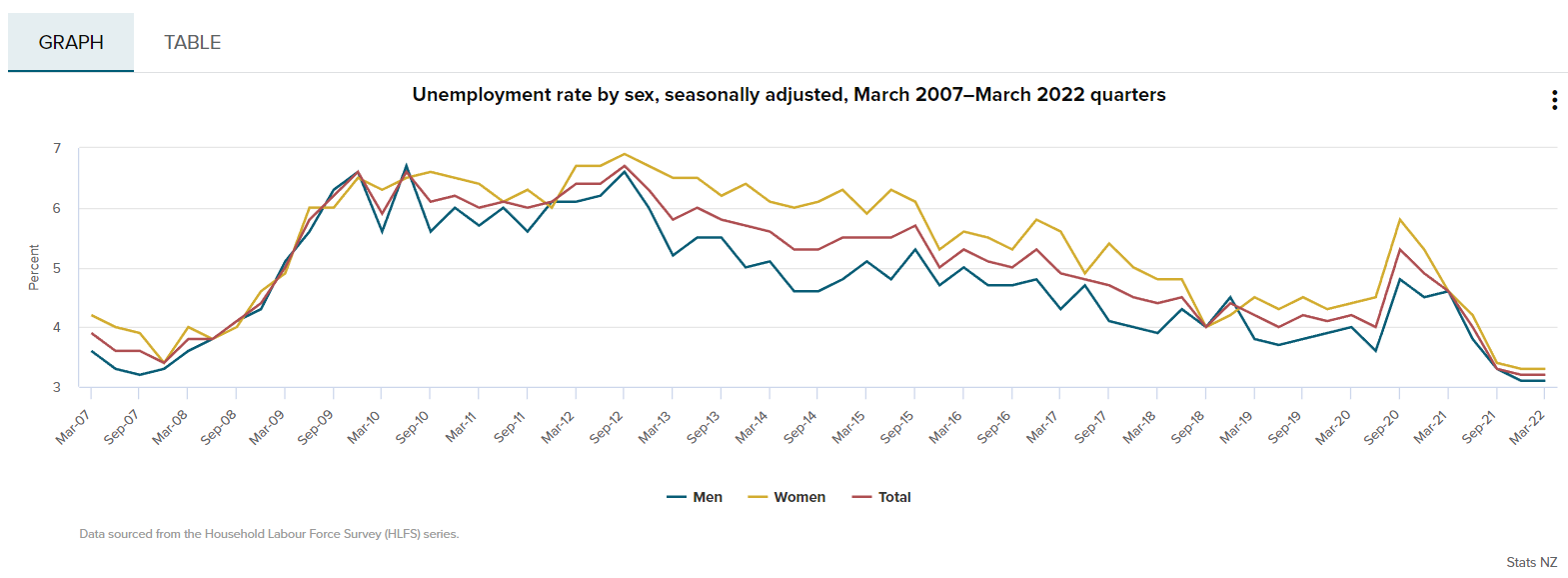

- The last published unemployment rate in New Zealand was 3.2%.

- The underutilisation rate (which sums both unemployment and underemployed) has remained steady at around 9.2%.

- Australia’s unemployment rate was 4.0%, with underutilisation at 10.3%.

- In the US, unemployment remained at 3.6% in June 2022.

So, it seems strange to fret over an impending recession when jobs are strong and shortages in some areas are critical.

The rapid rise in inflation also tells us there’s plenty of demand. Just not enough capacity.

Of course, the fear is that when central banks hike interest rates, all this turns on a knifepoint.

As high interest rates bite, people curtail both borrowing and spending. They’re also incentivised to save.

The last time we had a meaningful and lasting jump in unemployment was during the GFC in 2008:

It took a long time to bring unemployment down.

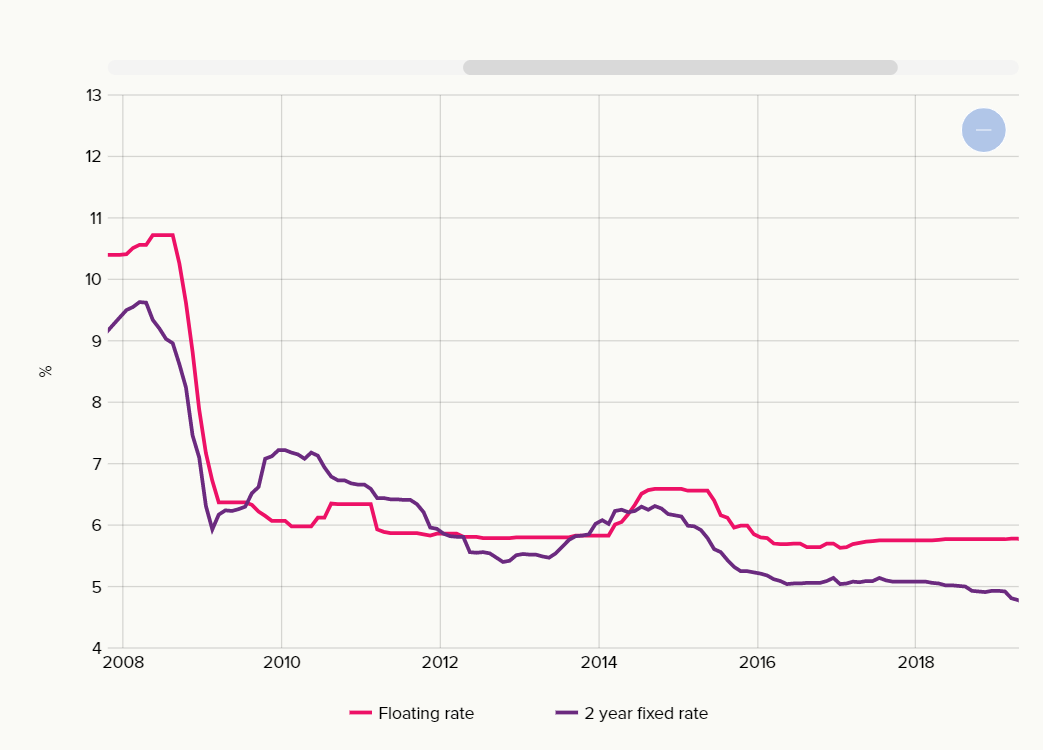

But in 2008, we had interest rates dropping like a stone:

Source: RBNZ

Clearly, there’s more to a recession than rising interest rates to try and curtail demand. (Or lowering them to try and spark it).

The snowball effect of layoff after layoff (as we saw during the GFC) is far more causal.

The impact of raising rates

Interest rates may also have less impact these days.

Our population is older. And it’s ageing.

As people get older, they might not have a mortgage — or much of a mortgage. They’re unlikely to borrow to start a new business.

The overwhelming phenomenon much of the developed world faces is this: the baby boomer generation — the largest and most prosperous generation ever — is now retiring. And the follow-on generations are much smaller.

The baby boomers are also spending far more in retirement than their predecessors. And they’re living longer.

By definition, as the generational shift is upon us, we’re running out of working-age people. Capacity constraints mean a tight labour market. And inflation.

I don’t see a strong recessionary, deflationary force anytime soon.

I see the once dismissed Phillips Curve making sense again. The trade-off for high employment is inflation.

Expect ongoing inflation. Ongoing growth. Ongoing capacity constraints.

And ongoing opportunity for businesses that can become more efficient via productivity gains or technology.

Will the current course of interest rate hikes kill growth?

The link between higher interest rates and economic activity is incredibly tenuous.

In a tight labour market, wages may rise to offset inflation. Though we’re not seeing wages keep up with inflation, when inflation nears 10%.

Maybe part of the very high inflation we’ve seen will soon pass. Bond buyers tend to be signalling this as yields on long-run rates have fallen.

War in Ukraine has contributed to oil and food price hikes.

Pandemic stimulus is still working its way through the economy.

Production, shipping, and in particular travel, are still recovering from the disruption of lockdowns.

Property prices

One more obvious link is that high interest rates do tend to depress asset prices. Especially property.

In a small housing-focused economy like New Zealand, this could have more widespread and very negative effects. Especially on sentiment.

Kiwis are used to their home values growing ever upward. The inevitable change to that story will depress many.

Maybe it’s time to pivot?

In the wider, global economy — where we run Managed Investment Accounts for Wholesale and Eligible clients — we’re seeing deep opportunity.

Opportunity to enter stocks with global real estate exposure. And defensive business models ready to rise when the cycle turns.

The bottom line

Right now, I’m not convinced any recession will be deep and lasting.

At least not until unemployment starts growing.

And my French café is open again on Monday. With more staff and pastry.

Regards,

Simon Angelo

Editor, Wealth Morning

(This article is general in nature and should not be construed as any financial or investment advice. To obtain guidance for your specific situation, please seek independent financial advice.)

Simon is the Chief Executive Officer and Publisher at Wealth Morning. He has been investing in the markets since he was 17. He recently spent a couple of years working in the hedge-fund industry in Europe. Before this, he owned an award-winning professional-services business and online-learning company in Auckland for 20 years. He has completed the Certificate in Discretionary Investment Management from the Personal Finance Society (UK), has written a bestselling book, and manages global share portfolios.