This time last year, the NZME share price was in the doldrums. Hit by Covid-19 fears over a decline in advertising. Still smarting from the Commerce Commission’s refusal to allow them to buy rival Stuff.

Fellow investors were telling me they saw no future for the Company.

I heard comments such as…

‘It’s traditional media.’

‘Traditional media is being fragmented and cut out by social media.’

‘They’re struggling with debt and bleeding print revenue.’

‘Sell!’

Fortunately, there were a few things that caused me to ignore this noise. And keep my shareholding.

- Their flagship radio station, Newstalk ZB, continued to post strong ratings growth. As a listener to ZB, I could see ongoing relevance to listeners and demand by advertisers. Competitors had fallen by the wayside.

- Herald Premium — the digital offer — appeared to be working and growing very well.

- Certain institutional funds were buying into the Company.

- NZME has a degree of moat, controlling key print and radio media in a small but lucrative advertising market.

- A compelling digital strategy was emerging, including a focus on the growth of OneRoof property.

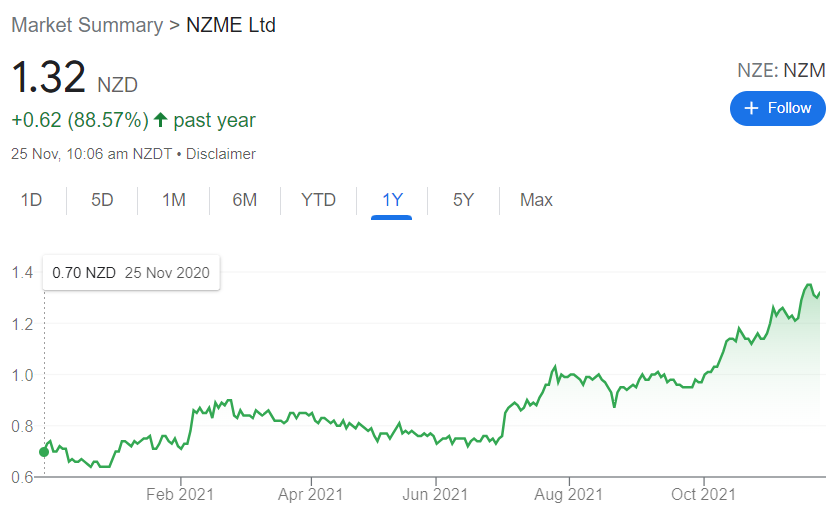

NZME has performed beyond expectation.

In fact, it has outperformed the market by nearly 90%!

The NZX 50 grew barely 1% over the past 12 months:

Source: Google Finance

Over the same period, NZME’s share price has grown almost 89% (at the time of writing):

Source: Google Finance

Why has the NZME share price risen?

The Company’s rapid recovery and share price growth has been aided by some key developments:

- In the half year to 30 June 2021, the business declared EBITDA growth of 4% to $30.1 million despite the pandemic.

- This did include government subsidies of $8.6 million.

- The dividend was reinstated with an interim dividend of 3cps declared.

- Net debt was reduced to $18.6 million (down $15.2 million).

- Digital revenue increased 145%.

Last month, NZME’s cash position strengthened even further with the sale of GrabOne for $17.5 million.

I thought it was time to sell GrabOne. In my opinion, this brand was looking a bit tired and needed a new owner with the ability to specialise in the deal space. Competition was also emerging from First Table, Groupon, and others.

We now potentially see a no-debt media business with some moat in key assets. And rapidly increasing digital revenue.

In fact, last week, NZME CEO Michael Boggs confirmed the debt position. And that golden acknowledgement of excess cash — the intention to return some to shareholders via a buyback in early 2022:

‘NZME’s balance sheet is in a strong position, with net debt having been reduced to zero, well below our target net debt range. This has allowed the Board to support a distribution of up to $30 million to shareholders, with an on-market buyback being the most effective method.’

Where could NZME go from here?

For investors interested in the future potential of the Company, I encourage you to check out the recent Investor Day Presentation.

This outlines the strategy going forward which has strong focus on audio assets, the Herald, and OneRoof.

With a P/E ratio now of around 15 at the current share price, NZME is no longer cheap. Though there is little else prevalent at reasonable value on the NZX.

In any case, with NZME, the market seems to have moved on from concern over print bleed and is seeing value in the digital-led growth.

The New Zealand media environment is still highly competitive. And I see alternatives with social media and a host of other providers.

NZME management has proven itself very adept. The return to favour with investors is well deserved. Though government support has played a role — arguably worthy, too, since journalism is important, and that same government denied their ability to consolidate with Stuff.

Given the price and risks, I’m seeing NZME as a ‘hold’ right now. Given my desire for income, a very positive ‘hold’, even ‘buy’ at a sharper price.

My opinion only, of course.

But there will be many investors who consume NZME media. Listen to ZB. Read Herald Premium. Look for property on OneRoof. They may like some strategic exposure to this country’s leading media business.

Of course, there are opportunities further afield that could offer higher growth potential. We cover those for our premium subscribers in our Quantum Wealth Report.

Regards,

Simon Angelo

Editor, Wealth Morning

(This article is general in nature and should not be construed as any financial or investment advice. To obtain guidance for your specific situation, please seek independent financial advice.)

Simon is the Chief Executive Officer and Publisher at Wealth Morning. He has been investing in the markets since he was 17. He recently spent a couple of years working in the hedge-fund industry in Europe. Before this, he owned an award-winning professional-services business and online-learning company in Auckland for 20 years. He has completed the Certificate in Discretionary Investment Management from the Personal Finance Society (UK), has written a bestselling book, and manages global share portfolios.