Quantum Wealth Summary

- Following supply chain disruptions from Covid, global manufacturing is changing fast.

- Additive manufacturing and 3D printing are among the fastest growing areas.

- Why ship components around the world when you can print them flexibly and more cheaply as needed?

- This infant industry is projected to grow over 1,200% over the next 10 years.

- We profile 3 listed manufacturing companies that could be poised to profit.

Wander around the old centre of George Town, on the island of Penang, Malaysia, and you will soon be absorbed.

A UNESCO World Heritage site since 2008, the bustling streets form a townscape of pre-war buildings, with a unique blend of Asian and British colonial styles.

The streets bustle with activity, tropical heat, and the various rich aromas of Southeast Asian delights.

Woo Hing Brothers Rolex Shop (left), Penang, Malaysia. Source: Pak-Thai Blogspot

Reach Campbell Street (Lebuh Campbell, as it is known) and you’ll come across the Woo Hing Brothers Rolex shop.

I have visited this store a couple of times over the past 20 years. My last was in 2018, when it had been refitted to luxurious and exacting standards.

My wife’s uncle’s family has owned this shop for over 70 years. It started out as a simple watch-repair business.

In 1950, it became the first and only Official Rolex Retailer on the island. A position it holds to this day, now spanning four generations.

During this time, it has weathered the Japanese occupation, the independence of Malaysia, and enjoyed rising prosperity in the country.

When I first visited in the early 2000s, business seemed to be humming at the shop.

In 2018, change was afoot. The store was quieter, though more beautifully appointed. The son was mainly running the business. And both father and son told us how business was changing. In 2018, with so much online and airport shopping, the business had become more about relationships with clientele.

Business and industries are always changing. That creates threats and opportunities.

You may not realise it, but Rolex is originally an English brand that started in London.

- Hans Wilsdorf and Alex Davis started Wilsdorf and Davis in 1905 with the goal of providing ‘high-quality timepieces at affordable prices.’

- They registered the name ‘Rolex’ in 1908, and the Company became the Rolex Watch Co. Ltd in 1915.

- Following World War I, Britain saw heavy post-war taxes levied on luxury imports and high export duties on the silver and gold used for the watch cases.

- Hans Wilsdorf moved the Company to Geneva, Switzerland. It became Montres Rolex S.A.and later Rolex S.A.

- On the death of Hans Wilsdorf in 1960, the company has been owned by the Hans Wilsdorf Foundation. A private family trust that donates around 90% of profits from the Company’s $5.2 billion in revenue to charitable causes, including the largest scholarship endowment in Europe.

Rolex likely moved to Switzerland after the war, not only for reasons of tax, but to take advantage of the concentration of skills and expertise in the burgeoning Swiss watch industry.

This industry itself has seen many changes. As the Swiss industry came to lose its dominant perch.

The development of the pin-lever movement led to the mass production of inexpensive American watches, such as Timex. By 1970, Timex was reputed to be the world’s largest watch producer by unit volume.

Then both the American and Swiss industries lost major ground to Japanese producers in the 1970s after the Japanese invented the quartz watch. Seiko, Casio, and Citizen took significant market share.

The Swiss watch industry fought back with the quartz-based ‘Swatch’ of the 1980s. Yet the watch industry is changing again with the advent of smartwatches such as Apple Watch.

Industries are always on the move. As investors, we need to find companies that maximise the potential upside while minimising the risks. We seek opportunities at the edge.

Seiko may have been such an opportunity in 1970. These days, as I write, its 2021 share price is about back to where it started in January 2000.

Source: Google Finance

The future of manufacturing

We’ve seen two decades of growing prosperity. Except for a short liquidity meltdown in 2008, property and other asset prices have climbed steeply upwards. It’s been historic.

And for good reason. Globalisation has seen hundreds of millions of workers in the developed world join the global supply chain. It’s created new markets. And it’s reduced the price of nearly every manufacturing good you buy, use, and replace on a regular basis.

I challenge you to try and find a toaster or coffee machine not made in China these days. Even by the Italian brands.

In countries like New Zealand, we’ve seen incomes grow at strong rates since the 1990s. China has provided an endless export market for our produce. While the wider Asia-Pacific has provided a source of prosperous and cashed-up migrants.

It is little wonder, in a tightly regulated housing market, that Auckland now has some of the highest property prices (by median income) in the world. It’s a safe haven for money from the globe’s fastest growing region.

By net worth, Australasians are now among the world’s wealthiest citizens. The Swiss of the Pacific. The golden barometer for a changing world.

Yet, since Covid-19, this world is changing again.

Developed economies are now questioning what two decades of globalisation has really got us:

- Ethical issues with global mass production, including climate damage and unethical labour conditions.

- Wholesale rip-off of intellectual property.

- Fragility of world supply chains now brought to light by Covid disruption.

- Key supply chain shortages of protective equipment, pharmaceuticals, and electronic components.

- Hollowing out of American manufacturing and working-class jobs.

- Recognition of the rivalry that now exists between the old Western powers and China.

- Much higher wage costs in China now reducing the cost attractiveness for manufacturing there.

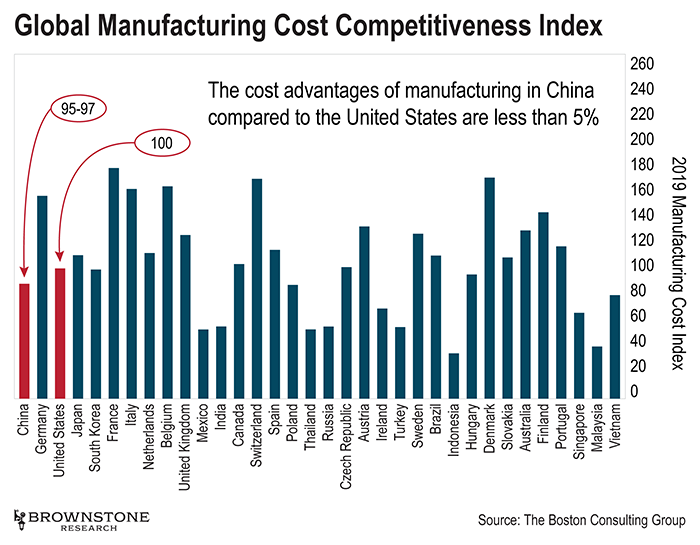

When it comes down to the business of manufacturing, it comes down to cost. Beyond political concerns, China is no longer as viable as it once was.

In 2019, a Boston Consulting Group study found the cost advantages in China weren’t much more than in the US.

We believe this advantage has eroded even further since Covid.

But China does have an overhead advantage. The tooling is set up and ready. Few locations can compete with the factory infrastructure there.

But change is afoot. And it is in this change we may see the next big investment opportunity…

Simon is the Chief Executive Officer and Publisher at Wealth Morning. He has been investing in the markets since he was 17. He recently spent a couple of years working in the hedge-fund industry in Europe. Before this, he owned an award-winning professional-services business and online-learning company in Auckland for 20 years. He has completed the Certificate in Discretionary Investment Management from the Personal Finance Society (UK), has written a bestselling book, and manages global share portfolios.