Economics is a study of human behaviour. In particular, how we relate to and deal with money.

Spend any length of time in the discipline — as I did at Auckland University in the 1990s — and you will be left with a key learning. People are not always rational. When they act irrationally en masse, you can get bubble markets and devastating crashes.

Good government should ideally step in and work to address dangerous cases of market failure. But sometimes things are just too far gone.

So it is with housing in New Zealand, where prices no longer reflect the actual utility value of a home

It may be that houses in this country have become ‘positional goods’.

Economist Fred Hirsch used this term in the 1970s to describe products ‘whose price was determined by their scarcity and desirability rather than their underlying utility.’

When I bought my first home in Royal Oak, Auckland in 2000, it was around 3x my income. Although it was on a busy road, and hence presented first-home buyer discount, it was a convenient place to live.

It had utility value.

My 67% mortgage on that property was at 7.95% interest. That was easy to fully cover with two flatmates. So I had a very affordable place to live.

In 2021, that same house presents no such utility. As a multiple of average Auckland household income, it is now around 10x.

It is priced that way because homes (and land) in central Auckland are scarce. But that scarcity is exacerbated by debt.

The $300 billion question

This year, we project that by Christmas, New Zealanders will have paid out $18 billion in mortgage payments (around 40% principal and 60% interest). And that total mortgage debt will exceed $300 billion.

The problem with this is that total GDP is only $320 billion. Suggesting mortgage debt is 94% of this.

Although this number in itself does not mean a lot, it is useful on a comparative basis.

When it comes to a debt-fuelled housing market, New Zealand is near the top of the OECD list — though exceeded by Australia (120%) and Canada (100%).

You can access the full interactive map by the IMF here.

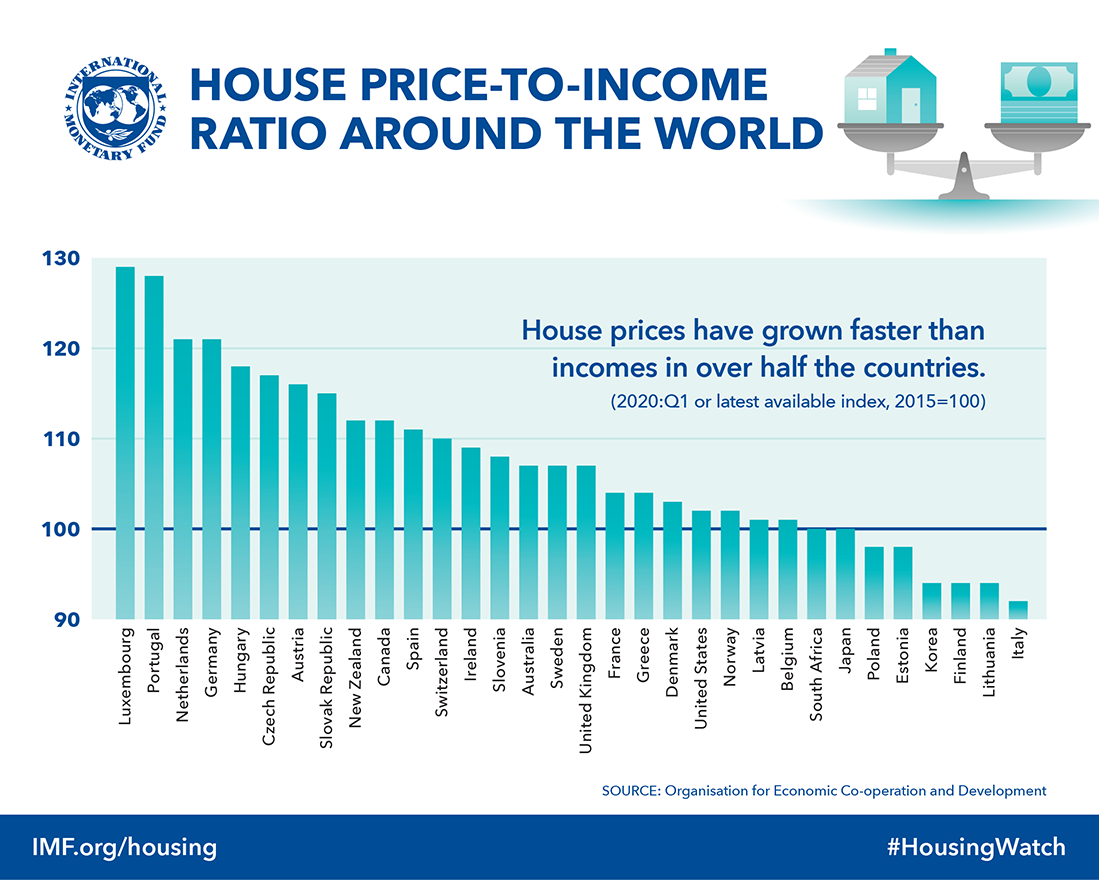

New Zealand is also in the top third of countries by house price-to-income ratio:

If you want true value in housing, Italy looks to be one of the best bets. And this may help to explain why a much greater portion of Italians are homeowners, compared to New Zealanders.

But here’s probably the most crucial reason: Household debt in Italy is only 41% of GDP. Less than half of what it is in New Zealand (where it’s 94%).

Meaning the property market in Italy is far less fuelled by debt.

My own experience in applying for a mortgage in Europe is that they are much harder to come by. In particular, I noticed:

- If you are renting the property out, there might not be any ability for you to deduct mortgage interest as an expense.

- LTV (loan-to-value) requirements tend to be lower. In Italy, maximum LTVs for some banks can be only 60% — meaning you must have a 40% deposit. In Britain, while higher LTVs are possible, they come with higher rates.

- You often have to pay an ‘arrangement’ or ‘booking’ fee, which can be as much as $2,000 for owner occupiers and $4,000 for buy-to-let.

- Banks are unwilling to lend at high DTI (debt-to-income) ratios. In Italy, DTI ratios are around 3x. In Britain 90% of lending is mandated at no more than 4.5x.

- There may also be stamp duty or other government taxes on taking out a mortgage.

Time for a forward-looking solution?

It appears that tightening credit can help rein in runaway home prices. And make homes more affordable. This may be an area where the New Zealand government and the Reserve Bank could reduce the octane currently fuelling the market.

And for the average person, the power of saving and investing is vital. Good savings habits and sensible investing in smaller growth assets like equities can help you build the best possible deposit. This will reduce the LTV ratio needed when it comes to buying a home.

Here at Wealth Morning, we’ve also been looking at other ways to improve housing affordability. And create investment opportunities.

We want to do something to help. For both younger homebuyers. And investors.

Our best idea is summarised in our new petition.

Do have a look (and sign it) here 👉 TheKiwiDream.nz

Regards,

Simon Angelo

Editor, Wealth Morning

Simon is the Chief Executive Officer and Publisher at Wealth Morning. He has been investing in the markets since he was 17. He recently spent a couple of years working in the hedge-fund industry in Europe. Before this, he owned an award-winning professional-services business and online-learning company in Auckland for 20 years. He has completed the Certificate in Discretionary Investment Management from the Personal Finance Society (UK), has written a bestselling book, and manages global share portfolios.