New Zealand has burst on to the global news.

Volcanic activity on White Island has claimed lives and caused horrific injury.

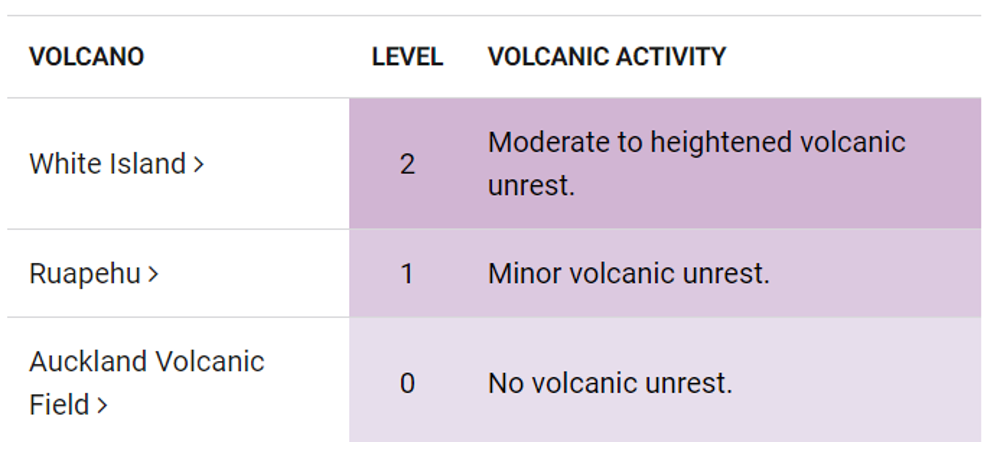

It is one of the world’s most active volcanic cones. In a continuous stage of releasing volcanic gas. The eruption on December 9 followed an increase to the volcanic alert level on November 18 to ‘2 — moderate to heightened volcanic unrest’.

So as an investor — vis-a-vis a risk practitioner — I ask the question: should there be tourism visits to White Island? Especially under an alert level of 2?

And in asking this question, I realise that many people, including investors, fail to correctly calculate risk.

New research finds that people tend to ignore the base rates of a risk. They apply an overlay of optimism to their individual situation. And overestimate the opinions and decisions of authority figures.

The danger of irrational thinking

For example, you’re a slightly overweight non-smoker of 50. Your doctor says you have an 8% risk of a heart attack. You may think, ‘Well, I don’t smoke, so it’s probably less for me.’

Or say you live in inland Hamilton and you’re told there’s a 2% chance that a climate-related catastrophe may strike. You may think, ‘Well, Hamilton isn’t near the coast, so it’s probably less for me.’

In both cases, you’ve made the mistake of reducing the base rate. The base rate of risk has already taken into account that you’re a non-smoker and Hamilton is not near the coast.

Then there is situational optimism and the role of authority figures. Perhaps you may think that if a registered tourism operator is happy to take tours to an area with Volcanic Alert Level 2, it must be fine.

Finally, the notion of ‘unlikely’ is frequently miscalculated. People often reveal their conception of an ‘unlikely event’ to be close to zero.

Underestimating your level of risk

Unfortunately, when you make an investment, these risk-calculation errors can worsen.

Here’s some examples:

- ‘It is unlikely White Island will erupt when I visit.’

- ‘It is unlikely the company the broker is recommending will go bust.’

- ‘It is unlikely I won’t find a tenant for my Auckland rental property.’

- ‘It is unlikely property values in Auckland could fall more than 20%.’

One of the reasons I do like shares is that many of the risks can be measured — including unlikely events. And it is easier to diversify across a range of risks.

In our Lifetime Wealth programme, we show investors how to invest globally. There is a powerful reason to do so from where I sit in Auckland.

Putting everything into context

Back in 1964, geology professor E. J. Searle of The University of Auckland calculated that the history of the city’s volcanic field ‘suggests that risk of further eruptions is of the order of 2 per cent chance per century.’

More recent studies suggest this risk could be increasing.

To put this into context, American studies show the average person has about a 1% chance of dying in a car accident within their lifetime.

In any event, while Auckland volcanic activity and road death generally is unlikely, it is not zero.

A worst-case scenario eruption in Auckland could wipe out 47% of the city’s GDP, as well as close the seventh-largest company on the NZX — Auckland International Airport [NZX:AIA].

As investors, how can we manage the risks and be aware of them?

There are two risks for stock-market investors.

- Market risk (systematic risk).

- Company or industry risk (unsystematic risk).

Systematic risk is almost impossible to avoid. If the entire market falls, it will impact your positions. But you can mitigate this in a high market by buying value, not overpaying for any security, and choosing dividend-paying businesses that are defensive.

One of the highest systematic risks right now is a sudden rise in interest rates. This can quickly deflate stock and property markets.

Company risk can be better controlled. Key risk flags I look for are around earnings, P/B (price-to-book ratio), industry outlook, and the margin rating your broker allocates to each stock.

How to diversify

For example, Auckland International Airport [NZX:AIA] currently posts a P/B of 1.7. This implies you are paying a 70% premium on the underlying assets. My broker provides margin lending of 50% on the stock — which should mean they see no major volatility concern.

Many larger NZX companies look fully priced to me. Yet, in Europe, we find property-based businesses with reasonable earnings ratios, P/Bs of less than 1, and margin rates of 50% in our Lifetime Wealth programme.

Diversification across different countries and currencies, alongside defensive allocation, could help mitigate systematic risk.

Meanwhile, diversification across different companies and industries will help to reduce unsystematic risk.

Risk analysis and stress testing

Once you’re invested, a good broker will provide you with a risk-analysis tool for your portfolio. Here, you will be able to stress-test a distribution of scenarios across your wealth.

Depending on your holdings, there will be risk of P&L (profit and loss) of +30% to -30% on your NAV (net asset value) in any particular year. So, on a portfolio of $1m, that could sit within a risk range of $700k to $1.3m.

Risk analysis would typically extend to currency gain or loss too.

Yields typically follow the risk range. Certain companies target particular yields and adjust dividend policies in line.

If your target dividend yield is 6%, your income risk range could be in the vicinity of $42k to $78k.

Looking at the big picture

I will probably remain living in the Auckland volcanic field — though I wish for the lifestyle of the outer countryside. And I will keep building smart, risk-managed portfolios that can provide a degree of financial security.

In the long-run, we are all dead. It’s how you manage the in-between that counts.

Regards,

Simon Angelo

Editor, WealthMorning.com

Important disclosures

Simon Angelo owns shares in Auckland International Airport [NZX:AIA] via wealth manager Vistafolio.

Simon is the Chief Executive Officer and Publisher at Wealth Morning. He has been investing in the markets since he was 17. He recently spent a couple of years working in the hedge-fund industry in Europe. Before this, he owned an award-winning professional-services business and online-learning company in Auckland for 20 years. He has completed the Certificate in Discretionary Investment Management from the Personal Finance Society (UK), has written a bestselling book, and manages global share portfolios.