An old friend of mine should probably be on the Rich List. In case the NBR come looking, he’ll remain nameless.

He inherited money. But he also grew that money. Most notably, he grew the money by entering industries on the cusp of expansion.

First, Auckland property, following the movements of value in that market.

Then ageing and transport.

He has also managed so far to avoid a key business problem in New Zealand. The market is so small, you can soon saturate the market or come up against too much competition.

As strategic investors, we look to be in industries that are poised to grow. In the global markets, our reach goes beyond New Zealand.

Of course, the real money is made when you spot a company about to take off; a company that few others have jumped into. It’s cheap now, but tomorrow it could be worth a lot more.

The strategy I apply to the portfolios I manage starts from the top and works down.

The country and its case. The industry and its outlook. The profitability of businesses in that sector.

Which areas are expected to expand in 2019 and beyond?

Let’s look at some US numbers. Tax cuts are helping fuel strong US growth. Future Fed rate cuts could further expansion. In the first quarter of this year, GDP grew 3.1% on an annual basis. Certain states lead the charge. Last year, Texas’ GDP rocketed ahead 6.6%.

By comparison, New Zealand GDP grew 0.6% in the first quarter to March 2019 — with annual growth of 2.7%.

Our numbers appear strong. Up there with the US. Until you factor in the fact that our rate of population growth via immigration is about three times that of the USA’s. We appear to be growing our economy by bringing in more people, rather than building out the productive base.

I’d like to see more focus on the productive base, since our default path has led to unaffordable housing, clogged roads, and stretched public services. But that would require some hard changes. Kicking back the compliance culture that has come to strangle business. Lowering business taxes. Supporting and protecting industries to grow. More difficult options than simply selling off the country to new residents.

But we’re getting ahead of ourselves. As market investors, there are no limits on where we can put our money. And we can look to data in other economies as to which industries may hold promise.

Growth industries in the world’s largest economy

We’re looking for the highest rates of projected revenue growth.

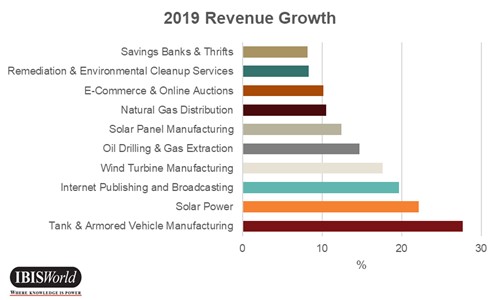

IBIS World projected the following top 10 industries for 2019 (US):

There are some themes here I suspect are global:

- Increased focus on renewable energy.

- Media moving evermore to the internet.

- World oil demand keeps rising.

- Traditional banks continue to grow.

The growing demand for oil is coming from the developing world. The other industries are domestically focused.

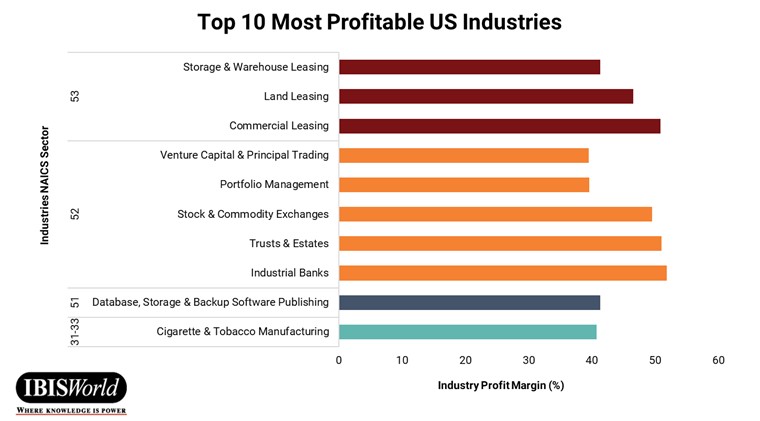

When it comes to assessing industry potential, revenue is not the whole story. We also need to consider profit margins.

IBIS World has assessed the top 10 most profitable industries in 2019 (US):

In terms of an overlap, with fast growth and high margin, we see the financial sector (banking). [openx slug=inpost]

Selecting stocks

Find the trend — then find instruments to profit from it.

I’ve been investing in two industries that match revenue growth with good margins and large and stable businesses.

Renewable energy and banking.

The investments have thus far been delivering in terms of growth and income.

The first is NZX-listed Infratil Ltd [NZX:IFT].

Having entered the stock at under $3.00, it’s been pleasing to see the price move north of $4.50. Along the journey, dividends have been around 5%.

The company has just completed a successful rights issue, where existing shareholders were able to top up holdings at $4. Although, the purpose to buy Vodafone is a future direction I’m less sure on.

Like my wealthy friend, Infratil has stuck to growth trend businesses. In particular, renewable energy and transport/aviation. These investments make up nearly 60% of the Infatil stable.

Would I buy more Infratil now? The rights issue made it reasonable. Let’s wait and see how the price rides as they get into the Vodafone deal.

As for banking, I’ve long thought a couple of the big Aussie banks represented value.

Commonwealth Bank of Australia [ASX:CBA] has been a good investment. We got in at around $65. Current price is $82. Dividends run in excess of 5%.

The business is strong in wealth management — the need for pension planning is growing at a fast clip in ageing Oz. And as the country’s largest bank, they also have the biggest home loan book. An area with great margins. Which may not be so pleasing to hear if you’re on their mortgage side.

CBA looks to me quite fully priced. Morningstar has a hold rating on it.

Westpac [ASX:WBC] may offer keener prospects. It’s Australia’s oldest bank. Currently priced at a P/E of around 14 and a dividend yield of around 6.5%. Again, the business does well in loan markets and allows investors to ride the continued growth in banking.

Both businesses are in recovery mode after a stinging Royal Commission of Inquiry on their practices. CBA seems to have moved on. Westpac will be one to watch.

And that’s investing. Keep watching the trends. Pay attention to the margins. Watch the board. Form your own convictions. And strike when the time is right.

Fortune favours the bold. And the on-trend.

Regards,

Simon Angelo

Analyst, Money Morning New Zealand

Important disclosures

Simon Angelo owns shares in Infratil Ltd [NZX:IFT], Commonwealth Bank of Australia [ASX:CBA] andWestpac Banking Corporation [ASX:WBC] via wealth manager Vistafolio. The value of shares may rise as well as fall, as may any income from them. No recommendation is given.

Simon is the Chief Executive Officer and Publisher at Wealth Morning. He has been investing in the markets since he was 17. He recently spent a couple of years working in the hedge-fund industry in Europe. Before this, he owned an award-winning professional-services business and online-learning company in Auckland for 20 years. He has completed the Certificate in Discretionary Investment Management from the Personal Finance Society (UK), has written a bestselling book, and manages global share portfolios.