Yesterday, Canterbury-based dairy company Synlait Milk Ltd [NZX:SML] stole headlines by posting a remarkable 89% increase in its annual net profits.

Their bottom-line profits shot up from $39.5 million in 2017 to $74.6 million this year.

A fantastic result for the company…and rewarding news for investors.

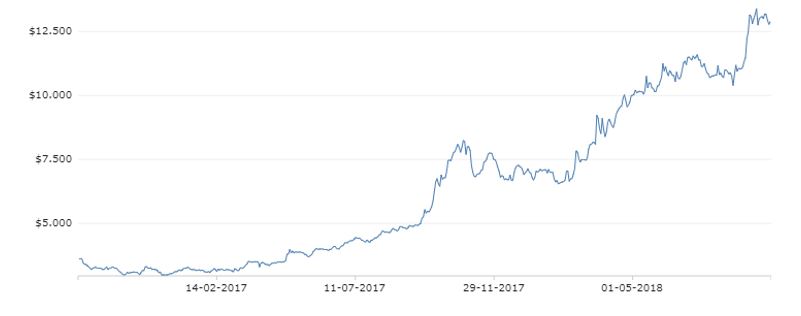

Two years ago, you could have purchased shares in Synlait Milk for a mere $3.62.

Today, that stock is worth $12.78.

|

Source: New Zealand Stock Exchange |

A 353% gain in just 24 months

And the company doesn’t intend on slowing down. It has announced plans to acquire Talbot Forest Cheese and also recently purchased 28 hectares of land in Pokeno.

That’s the sort of aggressive growth strategy that we like to see.

Plus, their leadership team just signed on former Fonterra exec Leon Clement as CEO. Who better to manage Synlait’s maturation in the dairy industry than someone who sat on the court of New Zealand’s largest dairy company.

Why is Synlait doing so well? Especially while much of the world’s dairy markets are sliding?

It’s simple — Synlait supplies a2 Milk with its wildly successful baby formula.

And that formula has become extremely popular in China over the past couple years.

It has doubled a2 Milk’s profit and stock price.

It’s part of a growing trend that we’ve identified in the Chinese market for premium Kiwi products, especially dairy and meat.

But the tide hasn’t lifted all boats.

Fonterra, Synlait’s giant neighbour, recently took a huge hit on its Chinese venture.

They recently posted a loss of $196 million, the first loss in its history. And most of the losses were associated with Fonterra’s Chinese venture, Beingmate. We discussed it in more detail last week.

So the question is — why did the Synlait/a2 partnership make a killing in the same market that killed Fonterra’s profits?

Both sides focused on infant formula. Both sides targeted the Chinese middle-class with their selling proposition based on New Zealand’s reputation. Both sides were supplied by Kiwi dairy farms.

So what went so right for Synlait and so wrong for Fonterra?

We believe it had to do with misunderstanding the Chinese consumer.

Right market, wrong approach

In July, we issued a report, ‘China’s New Boom: Three New Zealand Investments Primed to Soar in 2018 and Beyond’, that identified a growing interest in New Zealand exports in the developing Chinese market.

Among other reasons, we reckoned that China’s young, newly-wealthy middle-class would be interested in high quality imports to replace their domestic purchasing habits.

In other words, ‘Made in China’ wasn’t going to cut it in the new China.

Like the US car industry in the ‘70s, consumers transitioned to preferring Japanese brands over domestic US companies. They’d buy a Toyota, Honda or Datsun over a Ford any day. For Americans in that time, Japanese imports were a new luxury…made affordable to the middle class.

The same thing is happening in China today. Instead of their normal old Chinese milk, they’re opting for ‘premium’ New Zealand milk. And that phenomenon can be expected to occur across most industries.

So back to Synlait and Fonterra — what happened?

Well, I believe the market researchers at Fonterra made a serious mistake. Instead of a New Zealand-produced export, they decided to partner with an existing Chinese producer, Beingmate.

Effectively, they tried to slap a 100% Pure sticker over a Made in China sticker…and consumers didn’t buy it. Consumers didn’t see Beingmate as a NZ company operating in China. They saw Beingmate as a Chinese company funded by a New Zealand one.

So, the products were viewed as the same, inferior domestic products that the new middle-class were eager to dismiss.

A2 and Synlait, on the other hand, dove feet first into the premium NZ concept.

Their milk products aren’t from Chinese cows or Chinese dairy farms. They’re sourced from the pure dairy farms in the rolling hills of Canterbury.

And like French champagne, Kobe beef or Swiss watches…the connection between the exporter and premium quality was made.

Don’t cry over spilt milk

So what’s keeping Fonterra from doing the same?

I believe it’s their cooperative structure. They can’t just raise capital and build new factories like normal companies. Debt is a bit trickier.

It’s allowed them to grow and become a national superstar, but at the same time, it appears it’s made Fonterra a lumbering giant who makes long, slow steps instead of quick, agile sprints.

Synlait on the other hand can jump from project to project and quickly convert capital into profits.

Newsroom reports:

‘Over the past six months, investments have included an $11.2 million blending and canning facility, an $18.4 million wetmix kitchen, and an R&D centre in Palmerston North…At Synlait Dunsandel we expect to spend $125 million on an advanced liquid dairy packaging facility and at Pokeno we will spend $260 million to establish our new nutritional powder manufacturing facility.’

It’s that sort of quick development that allows for early movers in an industry to find — and potentially capitalise on — new opportunities.

Yet instead of doubling-down on their NZ export approach, Synlait has been dabbling with Chinese partnerships.

To me, that’s a mistake…and a lesson that Fonterra has recently learned.

But Synlait is going for it anyways.

Chinese-based Bright Dairy owns a majority stake in Synlait. So far, that hasn’t done anything to change Synlait’s strategy…but it could undermine Synlait’s reputation if consumers make the connection.

At the same time, Synlait made a deal with Sichuan-based New Hope Nutritionals. The Chinese company will supply Synlait with components to their infant formula, which will be blended and canned in New Zealand.

It could be a reputation-killer. But for now, the partnership hasn’t seemed to affect sales.

We’ll continue to watch the whole situation carefully and keep you updated.

Best,

Taylor Kee

Editor, Money Morning New Zealand

Taylor Kee is the lead Editor at Money Morning NZ. With a background in the financial publishing industry, Taylor knows how simple, yet difficult investing can be. He has worked with a range of assets classes, and with some of the world’s most thought-provoking financial writers, including Bill Bonner, Dan Denning, Doug Casey, and more. But he’s found his niche in macroeconomics and the excitement of technology investments. And Taylor is looking forward to the opportunity to share his thoughts on where New Zealand’s economy is going next and the opportunities it presents. Taylor shares these ideas with Money Morning NZ readers each day.