Back in the days when I was a personal financial advisor, I often had trouble getting through to one particular client.

The thing is, he’d always call me back…eventually.

‘Ryan! Sorry, mate! Missed ya call!’ It was a true-blue Aussie accent if ever you’d heard one.

He’d ride on horseback for miles to call me from a payphone in the middle of the desert! He mustn’t have ever bought any calling credit for his phone. We’d also get handwritten letters from him.

This bloke was the definition of old school. He had land worth almost $10 million, and yet got around on a horse, didn’t have a mobile phone, and had probably never heard of email.

I used to think: ’How does this guy live?’

Now, that thought rings truer than ever. I can’t imagine not having internet banking or being able to buy things online.

Most people in modern societies these days baulk at the very idea of not owning a smartphone.

But this is how our parents lived. This is how some of usused to live. And it was a pain in the rear, right? Long waits in the branch, fiddling with cash, deposit envelopes you had to handwrite, stamped receipts in your wallet, five days for a cheque to clear….

Of course, not everyone agrees.

We all know somebody who still insists on carrying around a cheque book.

Somebody who still lines up outside the bank to pay bills.

Somebody who, quite frankly, doesn’t like this new world of ‘tap-and-go’ technology, internet banking and Apple Pay. Never mind the recent explosion of interest in cryptocurrencies, which might as well be an alien language to them.

It can be easy to make fun of those people, but the truth is there has been a massive paradigm shift. I’m not surprised a few folks are suffering from whiplash.

Not even 30 years have passed since the World Wide Web came onto the scene. And now, all of this money is kind of just floating around in space — on the internet, in the ‘cloud’, and now in invented currencies.

But make no mistake, this is the way things are going. And its not slowing down. In fact, it’s just getting started…

Fintech is rapidly emerging as an industry to be reckoned with. And it’s not just influencing the way we bank or pay for things. It’s revolutionising the way you do business, send money abroad, get a loan and invest your hard-earned money.

I’d give it only ten to twenty years before absolutely everyone’s on board, including our old mate on horseback, if he’s still around.

Business Insider UK said in a recent report:

‘The increasing importance of technology-enabled products and services within the financial eco-system means the global fintech industry isn’t going anywhere.’

I think most of us would agree.

But let’s back-peddle a moment. [openx slug=inpost]

What exactly is fintech?

Broadly speaking, fintech refers to technology-led solutions being applied to the financial services sector in the 21st century.

In other words, where finance and technology converge, we have fintech.

In recent times, these sorts of companies have skyrocketed in numbers. And not just in the west.

Last year alone, investments in Hong Kong fintechs more than doubled, African fintech startups received over US$100 million in investment, and in 2016 China’s mobile payment market was worth US$5.5 trillion by volume.

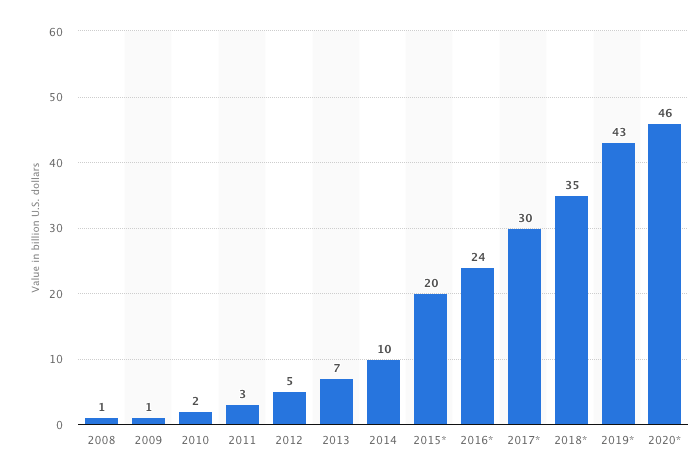

Worldwide, in 2016 fintech startups received US$17.4 billion in funding. That number has grown astronomically since then.

Check out the total value of fintech investments from 2008–2020 below:

|

Source: Apptechcorp.com |

But the fintech universe is not without its sceptics.

Banks are feeling threatened, reluctantly improving their technology offerings to try and compete (after all, they had a cosy monopoly until their uppity disrupters arrived).

Regulatory bodies are cautious of the new risks fintech will present, and they have a large stake in shaping the fintech landscape.

But fintech hubs like Silicon Valley and London aren’t fazed. While they used to distance themselves from banks, they’re now being spoken of as bank alternatives.

With blockchain technology also adding to the disruptive trend, these changes herald exciting times ahead for investors.

Why investors should be interested

Fintech is not a buzz word. It’s here to stay.

So, if you’re looking to invest in a fintech stock, you can be assured that it’s not just a passing trend.

Remember, some people used to think of cryptocurrency in that way. I’m sure they’ve spat out their coffee more than once while reading the news in recent years.

Just like crypto, fintech companies are working to revolutionise finance. According to CEO of UK fintech Kantox, Phillipe Gelis:

‘Fintech is changing the finance sector just like the Internet changed the written press and the music industries. In what is a stagnant sector monopolised by banks, finance is ripe for innovation and fintech is unquestionably the catalyst needed for change.’

How quickly our world will accept that change is anyone’s guess. But consider this…

You know how when you’ve got a question, people say ‘just Google it’? A recent news story reported the rapid growth of millennials saying ‘just Afterpay it.’

Afterpay Touch is an online payment solution company that allows people to pay in instalments. If we’re seeing fintech companies insert themselves into our everyday vocabulary, just like Google did, then it’s safe to say that people are pretty eager to adopt all of this disruption.

At least, that can be said of the younger generations.

My focus is on identifying the next big fintech giants so you can get in early and ride the exponential wave. Are you ready to put the down the cheque book?

Good investing,

Ryan Dinse

Ryan Dinse is a contributing editor at Money Morning New Zealand. He has worked in finance and investing for the past two decades as a financial planner, senior credit analyst, equity trader and fintech entrepreneur. With an academic background in economics, he believes that the key to making good investments is investing appropriately at each stage of the economic cycle. Different market conditions provide different opportunities. Ryan combines fundamental, technical and economic analysis with the goal of making sure you are in the right investments at the right time.