Do you remember Lance Armstrong?

He was the role model athlete.

Through hard work and determination, Lance came back from cancer and won the most fiercely competed bike race on Earth.

We all later found out there was a little more than hard work and work ethic to help Lance win.

On the Oprah Winfrey show, Lance admitted to taking drugs.

It put a hold on his gravy train of sponsors.

He also ended up paying US$5 million in fines for this fraud.

One thing saved Lance, though. It was ‘too good to be true,’ Lance would later say.

All he did was give US$100,000 to Chris…

Picking winners like it’s nothing

Chris didn’t study engineering.

He had no formal training in business or computer programming.

Yet he’s arguably the most successful investor in the Valley.

During his college years, Chris started a business with his student loan.

It went belly up.

With the remaining cash he started trading stocks.

Helped by rising tech stocks and a whole lot of leverage, Chris turned about $20,000 into $12 million.

And like the highs of the NASDAQ in early 2000, Chris’s new-found riches were also short-lived.

As tech stocks crashed, Chris didn’t just lose his $12 million. Thanks to leverage, Chris’s brokerage account dipped into negatives.

It wasn’t all bad, though.

Anyone who turns tens of thousands into millions tends to draw attention. That’s why Chris started his own venture capital firm. And he was going to scour Silicon Valley for the next big thing…

[openx slug=inpost]

You’re not Chris Sacca. Don’t even try!

Chris Sacca is likely the furthest thing you could get from Warren Buffett.

The Oracle of Omaha likes to understand what he’s buying. He doesn’t like projections. He always buys with a margin of safety (price substantially below value).

Chris does none of these things.

Not because he doesn’t want to. It’s just incredibly hard.

Who can understand the 10-year trajectory of a tiny start-up?

How can Chris not rely on projections when backing tech firms? It’s all he has to go off.

There are just so many unknowns. It’s why venture firms don’t expect to make money on all or even a majority of their investments.

The goal is to pick the next big thing. And maybe get one or two of them right.

What’s amazing about Chris is how many winners he’s been on the other side of.

Chris was in names like Twitter, Google, Facebook and Instagram at early stages.

Of course, he did not know how large these heavy hitters would become. I think Chris would be the first to acknowledge luck played a huge role in his success.

Point is Chris’s investing methods work for the venture capital world. They don’t work out so well when you jump into the stock market and bet on things you think look good…

Growth isn’t always good

You might describe Chris as a growth investor.

He buys companies that are aggressively spending and aggressively growing.

At a certain point, Chris jumps out as others pile in.

Around the same time, entrepreneurs and businesses start to take notice of this growing start-up.

If the company is already profitable and the potential market is huge, then you can bet new competitors will start popping up all over the place.

It’s kind of what happened with Uber.

Uber rolled out all over the world. But in lock-step, other start-ups like Lift, DiDi and Ola emerged.

Now, this wouldn’t be such a problem if everyone was loyal to Uber. But that’s not the case, judging from their most recent quarterly results anyway…

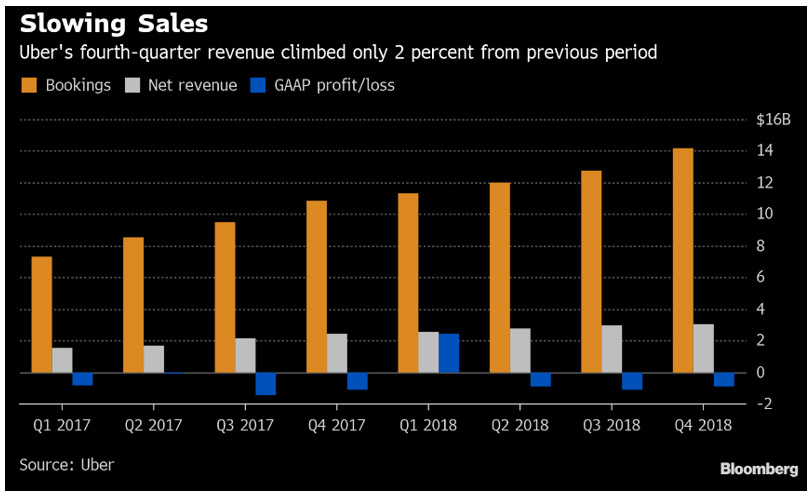

Source: Bloomberg

Sales continue to climb, yet the company continues to post losses. Here’s Bloomberg’s two cents on the results:

‘Losses were down 15 percent for the full year over 2017, but still reached an adjusted $1.8 billion. That could pose a challenge to investors trying to figure out Uber’s value in the public markets. Last year, bankers vying to lead the company’s initial public offering told Uber the market could value it at $120 billion. News that the company is still burning through more than $1 billion annually may give some investors pause.

‘…Like many unicorns, San Francisco-based Uber is emphasizing growth over profits. The company is investing aggressively in food delivery, logistics, electric bikes and self-driving cars. Last year, Uber bought Jump Bikes to help with its new mobility efforts, and it has a $1 billion budget for such projects this year.

‘Despite those investments, in the fourth quarter sales didn’t grow as fast as they have in the past. Of the $11.4 billion in net revenue the company generated in 2018, $3 billion came in the last three months of the year, up only 2 percent from the previous quarter.

‘That puts the company’s year-over-year quarterly growth rate at 25 percent. That’s high by many standards, but significantly lower than Uber’s third quarter year-over-year growth of 38 percent — a growth rate that was itself only about half the rate of six months prior.’

Clearly Uber is dropping prices to maintain their leading market share. They’ve also jumped into segments like freight, food delivery and electric bikes to chase growth for growth sake.

It’s a little bit like Amazon.com, Inc. [NASDAQ:AMZN].

The ‘Everything Store’ has jumped into everything, from home devices to the cloud storage. So far, investors have been convinced. Amazon is invincible.

Yet all they’ve done is prolong the inevitable.

There’s only so long you can continue running unprofitable divisions. There’s only so long you can continue to keep losing money.

Why you should steer clear from Uber

Uber needs to create a competitive advantage. Otherwise they’ll be just another hyped-up tech stock.

This word ‘competitive advantage’ gets thrown around a lot, so it’s worth clarifying.

It generally means you can do something that others can’t copy. Maybe you have access to demand (locked in customers) that others don’t. Maybe you have a cost advantage (more efficient).

Not only does Uber need a leg up on existing competitors, they need to create barriers to stop new firms from entering the market.

These barriers are usually made up of fixed costs. Maybe that cost is advertising. Uber, because they control a larger share of the market, can justify spending more on advertising.

This is a method Coca-Cola likes to use. They outspend every other soda brand (apart from Pepsi) many times over. And surprise, surprise, they’re the most popular cola in the world.

Or maybe that barrier is captive customers. If Uber can find a way to lock-in riders and drivers, new firms won’t be able to achieve scale in order to achieve profitability.

This is much like what Facebook does. They have an incredibly strong network that strengthens itself.

Any new competitor would find it extremely hard to chip away at their user base as a lot of these users are already locked in to the product.

It’s going to be a tough slog for Uber.

While they control most markets they enter, they have to keep prices low (resulting in losses) to keep everyone else out.

Any profits they do make will soon be met with competition (as long as they don’t have a competitive advantage).

Chris was one of the early investors in Uber. By proxy Lance also made millions from Uber.

But will you make money from this loss-making, puffed-up, soon to be listed taxi company?

I don’t think so.

Steer clear of Uber,

Harje Ronngard,

Editor, Money Morning

Harje Ronngard is one of the editors at Money Morning New Zealand. With an academic background in finance and investments, Harje knows how difficult investing is. He has worked with a range of assets classes, from futures to equities. But he’s found his niche in equity valuation. There are two questions Harje likes to ask of any investment. What is it worth? And how much does it cost? These two questions alone open up a world of investment opportunities which Harje shares with Money Morning New Zealand readers.