I hope you’ve been enjoying Simon’s articles lately…I sure have. If you missed his big predictions for 2019, it’s worth your time to take a look here.

I was in the States last week for the funeral of my grandfather. He was 80 years old, but sharp as a tack and fit as a fiddle.

I’m not talking fit as in 500m strolls down Tamaki Drive. I’m talking daily jogs, regular walks, and playing basketball against 25-year-olds in the local league.

He was in excellent shape.

So when he passed suddenly, it took everyone by surprise. We all figured that he’d outlive us!

But, alas, he was taken by pneumonia and taken far too soon. Apparently, fitness doesn’t matter when it comes to pneumonia; it’s more about staying properly vaccinated.

So I’d like to take this quick opportunity to urge you to stay up-to-date on your pneumococcal vaccinations…especially if you’re retirement age. If you’re unsure where you stand, please give your GP a call. A couple of minutes could buy you a few years.

Swiss balderdash

If there was anything positive for me last week, it’s that I managed to miss the World Economic Forum completely.

In Davos, Switzerland — coincidentally just around the corner from where my grandfather lived in Geneva — the world’s elite came together to clink glasses and eat fondue…under the pretense of bringing the world’s most pressing issues to light.

This year, the topic was ‘Globalization 4.0: Shaping a New Architecture in the Age of the Fourth Industrial Revolution’

In attendance were about 2,500 well-established academics, wealthy businesspeople, powerful politicians, and famous celebrities.

Nassim Taleb, the guy who came up with the black-swan idea, nailed it when he told Bloomberg that World Economic Forum is really ‘chasing successful people who want to be seen with other successful people. That’s the game.’

Fun fact: each attendee pays over US$600,000 to attend.

Worth the money?

Not a chance.

You see, the idea behind the forum is something you can probably get behind — gather all the world’s big decision-makers together to make positive changes for humankind.

But, unfortunately, there’s lots of talking about big changes…and not so much implementing those big changes. Rather, as Taleb described, it’s more of a pissing contest for the rich and powerful.

World economic order?

Here’s the idea I’d like to discuss today — does the world need a unified economic order?

Or, in other words, is globalism a good thing?

(Don’t get globalism confused with globalisation. Globalisation refers to how international commerce is growing. Globalism is the ideology that calls for worldwide regulations. The World Economic Forum often includes a bit of both.)

To help us come up with a response, let’s picture what end-game globalism would look like…

Imagine a global regulator…let’s call it Econpol. These guys have the capability to create and implement regulations across the entire economic arena. And when a country fails to act in accordance, they have the power to prosecute.

(Most international agreements lack that element these days…) [openx slug=inpost]

Now, Econpol has no vested interests in the economies it governs. So it’s able to act completely independently…but at the same time, that means they have no incentive to promote the best interests of those that it represents.

Econpol could pursue whatever goals it deems worthy.

Perhaps, for example, it raises the minimum wage to $15 per hour for every single country on earth, theoretically counteracting poverty and third world wage gaps.

For New Zealand, no biggie. That’s about where it is for us now anyways.

But for African country Seirra Leone, this would destroy their economy in a millisecond. Their current federally mandated minimum wage is $0.02 per hour.

So jumping to $15 per hour would be a 75,000% increase…and would be real tough on the few employers in the country struggling to make do.

But, on the flip side, maybe Econpol says the minimum wage is now $2 per hour.

Imagine trying to pay your $400-per-week rent on that kind of income. It’d be impossible. You’d introduce either widespread homelessness or a market crash.

Probably both.

And that’s the problem with this fantasy global regulation concept — every market is unique and has its own specific capabilities and interests. Trying to standardise the diverse economies of the world can only result in endless tampering, and a downward spiral in the standard of living.

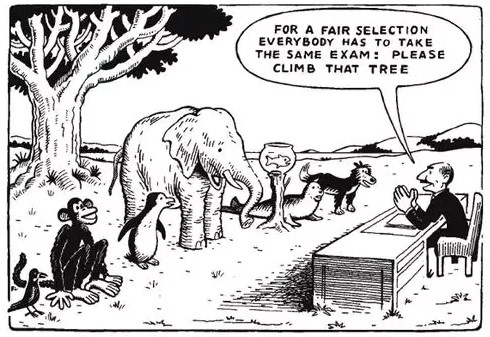

A good way of describing this problem is through the quote below often attributed to Einstein:

‘Everybody is a genius. But if you judge a fish by its ability to climb a tree, it will live its whole life believing that it is stupid.’

|

Source: Quora |

You may have seen that comic in the terms of standardised education, but I believe it’s just as relevant for standardised economics. Individual people and economies are both unique…and will have different paths to success.

The future?

Perhaps you’re wondering how this applies to you…after all, we’re a long way from Davos.

The truth is that the world is quickly heading in the direction of an Econpol…and leaders like our dear Jacinda are jumping into it feet first. (See her comments at the Swiss event here.)

We’re seeing international regulatory bodies emerging successfully…and as their power grows, so too does the risk of creating imbalances in markets around the world, including ours.

But perhaps I’m wrong…that these elites in Davos are capable of pulling the levers of the global economy and running it better than Smith’s ‘invisible hand’.

Maybe their Ivy League educations and private jets are what the world needs to improve. Maybe through their après-ski strategy sessions, these folks can fix everything…and we’ll all be sharing a big fondue pot together in no time.

Maybe…or maybe not.

What do you think?

Reach me at [email protected]

Best,

Taylor Kee

Editor, Money Morning New Zealand

Taylor Kee is the lead Editor at Money Morning NZ. With a background in the financial publishing industry, Taylor knows how simple, yet difficult investing can be. He has worked with a range of assets classes, and with some of the world’s most thought-provoking financial writers, including Bill Bonner, Dan Denning, Doug Casey, and more. But he’s found his niche in macroeconomics and the excitement of technology investments. And Taylor is looking forward to the opportunity to share his thoughts on where New Zealand’s economy is going next and the opportunities it presents. Taylor shares these ideas with Money Morning NZ readers each day.