Nearly two years after Brits voted ‘Leave’, Theresa May has finally negotiated a tentative Brexit agreement with the EU.

Now, make no mistake — we’re still a long way off from a final deal.

To get to the finish line, this agreement must make it through:

- A cabinet review this week

- A consultation between cabinet ministers and the prime minister

- A presentation at the EU summit in November

- A bilateral publication of the withdrawal agreement and political declaration

- A ratification process by British Parliament

- A ratification process by European Parliament

- Not to mention, several cabinet members have threatened to quit if the deal doesn’t fit their requirements. If that is indeed the case, there could be a turnover period as new ministers are appointed…and they conduct their reviews of the agreement.

It’s a long road ahead…but the deadline is on the horizon — 29 March, 2019.

One of the most complicated matters of the agreement is that of the ‘backstop’. This is a clause that will allow for a soft Irish border, even after Britain leaves the European bloc.

When cabinet ministers open the 500-page agreement, they’ll find out exactly what Theresa May has agreed to…and if it’s not what they’re wanting, you may see a wave of resignations in the headlines next week.

The whole situation has some interesting implications for New Zealand.

For one, we have important trade relationships with both sides of the Brexit issue.

We export over $3 billion and import $2 billion from the UK each year. That represents our fifth-largest trade relationship.

With the rest of the EU, we export $5 billion (mostly wine, fruit and meat) and import over $10 billion (mostly vehicles, aircraft and pharmaceuticals). They represent our fourth-greatest trade partner.

When Britain departs in March, we’ll immediately jump into a fresh free-trade agreement.

Fortunately, the UK has nominated New Zealand as one of their priority partners when it comes time to negotiate a new deal.

With the EU, we’ll simply continue the ongoing negotiations for a free-trade agreement, which is estimated to be concluded in 2020 or 2021.

In terms of trade, this is all good news.

As it stands, we currently pay tariffs out the wazoo for many of the products crossing these borders…

With an independent UK, we’ll finally be able to shake off those chains and step into a free-flowing trade relationship.

Then the EU will be incentivised to compete for our trade…perhaps fast-tracking the free-trade agreement on that end.

Kiwi importers and exporters could see their costs of transport go down…potentially decreasing the price you’ll pay at the counter.

Plus, lower costs mean fewer obstacles to entry for new businesses interested in overseas trade. In other words, Brexit could trigger a surge in new businesses here in New Zealand…and with British companies wanting to offer their products here. [openx slug=inpost]

Larger companies with existing trade flows could see the torrent of new competition creating a downward pressure on their prices and therefore profit margins.

Again, all good news for consumers…and mostly good news for business owners.

One of the most interesting developments we could see with new free-trade agreements is in the housing sector. We could easily see cheaper construction equipment and machinery coming in from the EU.

At the same time, raw materials — traditionally an NZ export — could become more cheaply available…perhaps decreasing construction costs and boosting building across New Zealand.

But, listen, this is all economic theorising…

Your mainstream talking heads — who seem to be generally anti-Brexit — could speculate just the same…and come up with opposite conclusions.

It mostly falls back to your perspective on the markets. Do you consider less regulation better or worse for consumers?

I believe history has proven that deregulation in the global arena has been generally good for people…but then again, there are some seriously smart people out there who would disagree.

Nobel Prize-winning economist Joseph Stiglitz is a good example. He believes that free-trade agreements can be ‘job killing’ by decimating wages for member countries.

There’s something to that. Free trade means more competition…more competition means lower prices…and that applies to labour just as much as it does for timber or bath towels.

But there’s an opposing force at work — prosperity.

And prosperity can lift the tide of a nation’s economy…cancelling out the temporary consequences of competition. Dartmouth economics professor Nina Pavcnik stated (emphasis mine):

‘It is virtually impossible to find cases of poor countries that were able to grow over long periods of time without opening up to trade. And we have no evidence that trade leads to increases in poverty and declines in growth.’

Instead, we see less poverty and more economic growth. How? Through the magic of free trade…

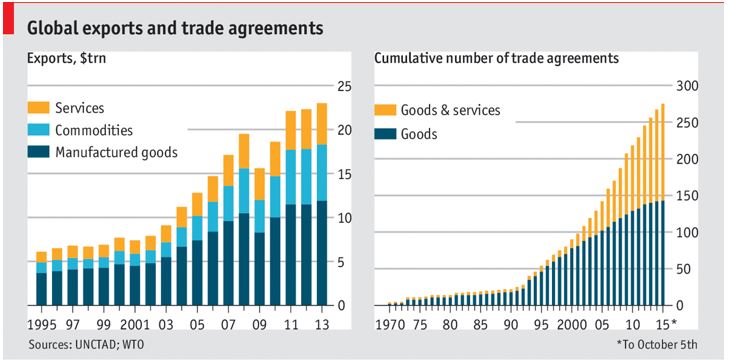

In fact, The Economist — a publication which regularly flip-flops on the topic — found there was a strong correlation between trade agreements and worldwide economic growth.

|

Source: The Economist |

For an export-driven economy like New Zealand’s, our prosperity is highly dependent on our ability to get our products overseas…and to stay competitive on price.

With tariffs, like those we currently pay to get our products on European shelves, we’re less able to do that…and that means fewer sales, less profits and less prosperity.

But soon, when these new free-trade agreements get signed off, we could see that switch flipped.

Godspeed, Theresa.

Best,

Taylor Kee

Editor, Money Morning New Zealand

Taylor Kee is the lead Editor at Money Morning NZ. With a background in the financial publishing industry, Taylor knows how simple, yet difficult investing can be. He has worked with a range of assets classes, and with some of the world’s most thought-provoking financial writers, including Bill Bonner, Dan Denning, Doug Casey, and more. But he’s found his niche in macroeconomics and the excitement of technology investments. And Taylor is looking forward to the opportunity to share his thoughts on where New Zealand’s economy is going next and the opportunities it presents. Taylor shares these ideas with Money Morning NZ readers each day.