Unless you’ve been living under a rock, you’ll know that the New Zealand housing market is laughably expensive.

Frankly, you’d be lucky if you can afford a rock to live under.

Take, for example, this house in Kingsland. It was marked as a ‘total do-up’ and yet has sold for $1,362,000. According to the real-estate agents, over 70 groups came to view the property before it was sold.

|

Source: OneRoof |

One of the top highlights of the property was the big shed out back.

So, if the house is indeed uninhabitable, at least you could sleep in the shed.

Not too shabby for $1.36 million.

Or…if beautiful Pattaya, Thailand is more up your alley, you could get this eight-bedroom villa for about the same price.

|

Source: Thailand-Property |

Here’s a link if you don’t believe me.

But I get it — jacuzzies and beachfront property aren’t for everyone. Neither are landscaped gardens or three covered car parks.

Sometimes people just really like their sheds.

Welcome back, first-time homebuyers

The recent softening in the housing market has tickled the fancy of many new homebuyers, according to The NZ Herald.

Last month, one in every four houses sold were purchased by a first-time buyer.

That sort of activity hasn’t been seen in over a decade.

According to some of the mainstream commentators, a perfect storm of low interest rates and ‘predicted price falls’ have led potential buyers to take the leap.

How far have prices actually fallen? 2%? 5%? 10%? 20%?

According to REINZ’s August report, rates have moved exactly 0.0% since last month.

And, if you exclude Auckland, prices are up nationwide by 0.9%.

|

Source: REINZ |

Since this time last year, home prices are up 4.1%.

So, in other words, when the ‘experts’ proclaim that house prices are falling in New Zealand, they’re really just saying that prices aren’t climbing as quickly.

Stagnating…but staying out of negative territory. Hardly a correction, by any means.

So is this it? Or is a real correction still out there…looming just below the surface? [openx slug=inpost]

What do the pros say?

According to one of the most prestigious economic research firms in the world — Oxford Economics — New Zealand ranks as the fifth most at-risk housing market in the world.

The researchers got to that conclusion by measuring the housing boom, debt levels, and the type of debt. They looked all the way back to 1970 to see how these trends have developed.

And what they discovered was alarming.

- New Zealand has represented the highest increase in real prices over five years.

- New Zealand was the second most overvalued market behind Hong Kong.

- New Zealand was third in housing debt-to-GDP (89% — Yikes!).

All in all, the Kiwi market was placed as the fifth most at-risk housing market in the world.

What do they expect will happen?

Based on their historical research, they estimate a 75% chance of house prices falling over the following five years.

And if it doesn’t fall during that period, the odds increase for the next five years.

In typical economist-speak, they stated that, ‘…this points to many OECD countries seeing stagnant or negative real house price growth in the next few years.’

Or in normal-people-speak, ‘Buckle your seat belts. You’re in for a bumpy ride.’

The analysts at Australasian Trading Management reckon that the fall could be as much as 10%, if the Aussie markets are any indicator.

The Economist’s data team recently stated (emphasis mine):

‘Property bulls argue that heady home prices are merely a function of the fundamentals of demand, supply and the cost of credit. The amount of land in the world’s most dynamic cities is fixed, yet thanks to the continuing trends of urbanisation and globalisation, more and more people want to live in them. Moreover, historically low interest rates have enabled prospective buyers to offer sums that would previously have seemed outlandish.

‘Yet in the long run, prices must bear some relation to incomes: people can only increase the share of their earnings they spend on lodging for so long before they run out of money. And the most cramped cities may be approaching this tipping point: in London, rents average about half of a typical pay-cheque.’

In Auckland? Median weekly income was $997 in the June quarter. Median rent is $530.

That means over half of your average paycheque goes to rent. More than in London.

How far to fall?

Unfortunately, I think it’s hard to put a firm percentage on exactly how far the market needs to correct. New Zealand’s housing market is quite unusual…and is hard to compare to other historical crashes.

ATM’s estimate of 10% sounds pretty good.

But that’s what could happen. Not what should.

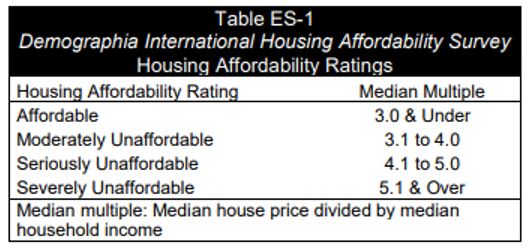

If we look at how New Zealand stacks up against similarly developed economies, the picture becomes grimmer. Let’s use the Median Multiple as our measuring stick. It’s what the UN, World Bank, OECD, and IMF all use.

It’s simple — just divide the median house price by the median household income.

And here is the guide for interpreting the result:

|

Source: Demographia |

In all of New Zealand, the median house price is $549,000 as of August 2018.

According to Stats NZ, median household income as of 2018 is $88,816.

That’s a median multiple of 6.18 — Severely Unaffordable.

To get back down to the ‘Affordable’ range, the median house price would need to be $266,457. That’s a 48% fall from current prices.

Or let’s just take baby steps. What about just moving back from ‘Severely Unaffordable’ to ‘Seriously Unaffordable’?

That would still require a 19% drop from current prices.

I’m not suggesting that markets will fall that far.

I’m just throwing it out as a reference point for what it could take for the housing market to be healthy again…and to show how full of bologna most of the overly-optimistic mainstream pundits are…as they praise the market’s health from their $1.3 million sheds.

Best,

Taylor Kee

Editor, Money Morning New Zealand

Taylor Kee is the lead Editor at Money Morning NZ. With a background in the financial publishing industry, Taylor knows how simple, yet difficult investing can be. He has worked with a range of assets classes, and with some of the world’s most thought-provoking financial writers, including Bill Bonner, Dan Denning, Doug Casey, and more. But he’s found his niche in macroeconomics and the excitement of technology investments. And Taylor is looking forward to the opportunity to share his thoughts on where New Zealand’s economy is going next and the opportunities it presents. Taylor shares these ideas with Money Morning NZ readers each day.