The financial year drew to a close at the end of June. The ASX 200 increased 8.6% over the year. Add on around 4% in dividends, and you get a very decent return of 12.6%.

Want to beat the market in financial year 2019?

The Australian Financial Review tells you how…

‘Australia’s top equity strategists agree the best way to beat the market in the 2019 financial year is be long resources and wary of banks and the high-flying growth stocks which lit up the bourse in 2017-18.’

Wasn’t being long resources and short the banks the way to beat the market in FY18? Does lightning strike twice in the same place?

It’s a little too obvious to do the same thing this year and expect to beat the market again. You can only beat the market by doing something different. Often, that requires you to take a position in companies that ‘the market’ thinks are dogs.

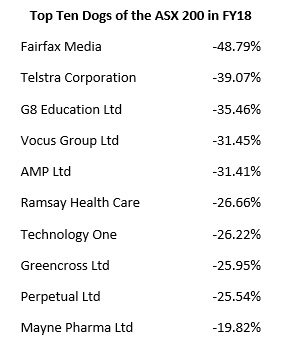

So in that spirit, let’s have a look at last year’s dogs of the ASX 200. Taking a small stake in these stocks could probably give you just as good a chance of outperforming as taking a stake in the top performers, and expecting them to do the job again.

Source: marketindex.com.au

[Click to open new window]

Fairfax is unfairly at the head of the pack. It spun out its online real estate business, Domain, in November last year. Given this is Fairfax’s only growth business, the share price fell sharply after Domain left the stable.

Even so, it’s an unlikely looking portfolio. Hardly the type you’d expect to provide your portfolio a decent boost throughout the year.

But that’s the point…

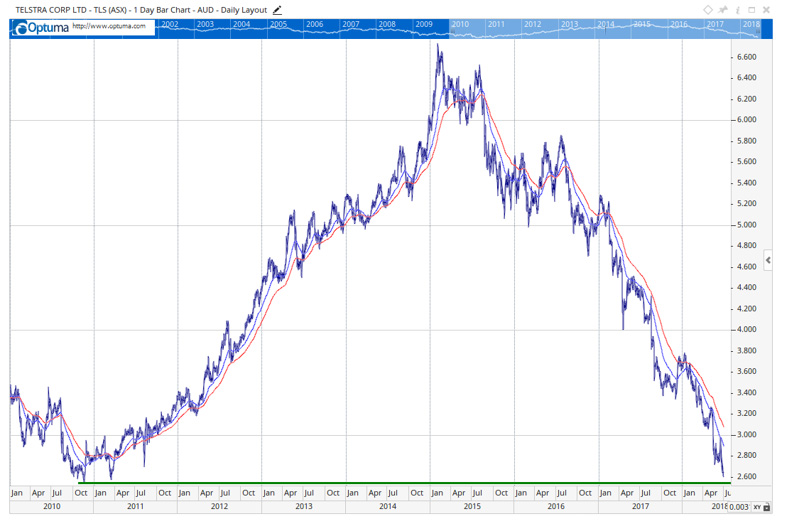

One stock I’ll be watching closely is Telstra. In my view, it’s now getting into good value territory. The company has finally launched a credible plan to move forward in a competitive environment. It’s finally getting rid of its bloated, bureaucratic employment structure.

All it needs to do now to completely reset is adjust its dividend lower to recognise both weaker earnings over the next few years and higher capital expenditure needs.

The thing I like about Telstra now is that it’s nearing the capitulation phase as far as investor sentiment goes. An announcement of another dividend cut will probably do the job completely. That should bring it back to its all-time lows, around $2.50. If it does, it will have been a long-term round trip, as you can see in the chart below:

Source: Optuma

[Click to open new window]

The interesting thing with Telstra is that it has a large ‘retail’ investor base, who own it for the dividend. But when a company pays out all or most of its profits as dividends, it means it’s not growing via reinvestment. Therefore, it’s not as valuable a company.

So if Telstra cuts its dividend, in order to have more profits for reinvestment, it actually improves the valuation of the business. But ironically, another dividend cut would probably see many investors dump the stock.

While I think Telstra is now in good value territory, that doesn’t mean I’d be buying here. One of the core investment rules of my advisory, Crisis & Opportunity, is to never buy stocks in a downtrend, regardless of how good the valuation looks. You just never know how far the trend will extend to the downside.

Your best bet is to wait until the trend turns higher.

Let me show you an example from the list above. I profiled Mayne Pharma for Crisis & Opportunity readers in February this year. But as the stock wasn’t in an uptrend, I said to just keep it on the watchlist. My instruction was to buy on a break above 80 cents, as that would indicate the start of a new upward trend. You can see how this played out in the chart below:

Source: Optuma

[Click to open new window]

Mayne broke higher in early June and continued to run. It then corrected slightly, but found support at the breakout point, which is a bullish sign. The moving averages have also crossed to the upside, another bullish sign.

I don’t know whether it will keep rising. But I do know the odds are now on my side, as opposed to buying into a downtrend and hoping things will work out.

That’s why I wouldn’t be buying Telstra now, or AMP, or Ramsay Healthcare for that matter. But if the trend changes, they may just provide your portfolio with a solid boost in 2019.

Regards,

Greg Canavan

Greg Canavan is a Feature Editor at Money Morning. He likes to promote a seemingly weird investment philosophy based on the old adage that ‘ignorance is bliss’. That is, investing in the Information Age means you have all the information you need at your fingertips. But how useful is this information? Much of it is noise and serves to confuse, rather than inform, investors. And, through the process of confirmation bias, you tend to read what you already agree with. As a result, you often only think you know that you know what is going on. But, the fact is, you really don’t know. No one does. The world is far too complex to understand. When you accept this, your newfound ignorance becomes a formidable investment weapon. That’s because you’re not a slave to your emotions and biases.