‘The five ascending levels of intellect: Smart, Intelligent, Brilliant, Genius, Simple.’

Albert Einstein

If ever there was a time to ‘keep it simple’, it’s now.

The market calm of early 2019 is only a temporary lull in the market’s corrective process.

Luring the unsuspecting into believing the worst is over.

Wrong!

Expect to see a return of the volatility we witnessed in late 2018…but with a little more vengeance.

Why?

Based on historical values, the US share market has to shed at least 50–60% of its value. The ride to this much lower level will not be for the faint-hearted investor.

And when the process begins in earnest, those fancy new Exchange Traded Funds (ETFs) loaded up with glamour stocks, high-yield bond funds, leveraged products (private equity funds, hedge funds et al) are going to be subjected to severe market stresses.

As prices plummet, redemption requests (from panicked investors) come flooding in, liquidity dries up and the manager imposes a freeze on funds.

In the final wash-up, these once-sort-after bull market assets are worth cents on the dollar.

It’s a familiar pattern for anyone who’s been around markets for any length of time.

If keeping it simple is smart, then, by my reasoning, making things complex is dumb…and that’s certainly what I’ve observed.

In 1992, a well-known investment bank launched a ‘Currency Trading Fund’.

The fund’s operations were somewhat opaque.

The mystery surrounding FOREX (foreign exchange) markets only served to pique investor interest…even though they knew little about the asset class.

The fund was closed ended…meaning that once the capital raising was done, the fund was closed to new money.

Thanks to the fall in the Aussie dollar (from the high-US 70 cent level to the mid-US 60 cent level) the fund rewarded initial investors — in a short space of time — with a double digit return.

Back in the early 1990s, that sort of performance was extremely hard to come by.

By comparison, the share market was lacklustre (the tech boom was still a few years away). And, unlisted property trusts were in a state of deep freeze.

On the strength of this past performance, a second currency trading fund was launched. Money flowed in…chasing yesterday winner.

The complexity of the product — the fact that no one really understood what it did — was perversely part of its allure. The fund represented an opportunity to participate in the bounties of foreign exchange.

Questions that should have been asked, were not.

Questions such as…

On what criteria was one currency chosen over the other? Could the performance be replicated? Was there any hedging? What were the total operating costs and management fees? What were the downside risks?

These details mattered little at the time. In the minds of investors and advisers, the fund was a winner. What could possibly go wrong?

The Aussie dollar regained strength. The fund’s currency traders were on the wrong side of the trade…losses mounted up. Money flowed out. The funds closed. Never to be seen again.

The rise and fall of the currency funds was yet another lesson (after the ’87 crash and unlisted property trust disaster) in the need for transparency and understanding risks.

Something investors, amateur and professional alike, seem to place too little weighting on…until it’s too late.

What happened to the currency fund has been repeated many times over.

Rise. Fall. Liquidate. Lament.

People crave complexity

Keeping it simple helps minimise the risk of nasty surprises.

Yet, to my ongoing surprise, I found that people don’t want simplicity.

Money in the bank…boring.

Index fund (tracking the ASX 200)…boring.

Buy gold bars…boring.

Dinner party talk is far more stimulating when you talk about the stellar returns from your ‘currency trading’ fund. How exotic.

It seems that people (consciously or sub-consciously) crave complexity…believing (mistakenly) the more complex an investment, the closer they are to the inner sanctum of the ‘wheelers and dealers’.

Over the life of the investment cycle (rotating from rise to fall) complex investments rarely deliver.

Why? [openx slug=inpost]

In my experience, these products tend to be launched during the ‘rise’ phase of the cycle…appealing to investors’ need for greed. And, that’s a very lucrative ‘itch’ that institutions are only too willing to ‘scratch’. The more complex and opaque the fund, the more fees they can charge. That’s the simple formula institutions follow.

These products are what I call ‘good time Charlies’. The funds have never been stress-tested during the rigours of the ‘fall’ phase.

Over the years I’ve seen complex products come and go from the marketplace.

Investors never learn.

However, the lesson I’ve learned from more than three decades in this business, is the wisdom of keeping things simple.

To quote Einstein again…

‘If you can’t explain it to a six year old, you don’t understand it yourself.’

And the reverse holds true. If someone cannot explain something to me in lay person terms, the conclusions to draw are…

I’m dumb and they’re smart.

OR

They’re trying to baffle me with bulls**t.

To find out which it is, simply ask questions that begin with ‘why’.

Soon enough you’ll find out either how much they really know or how much you don’t.

Either way, if you (and the operative word is, you) don’t understand it…walk away.

Keep your money for another day and another opportunity…one that you do understand.

And there’s absolutely no shame in adopting a simple approach.

When you have the confidence to say, ‘I don’t understand what you’re talking about’, then you’re on the way to a superior level of intelligence.

I didn’t and still don’t understand cryptocurrencies. Not getting caught up in that fad saved me from losing 80% or more of my capital.

I don’t understand how a few extra percent of return is worth risking 50, 60 or even 70% of your capital. Makes absolutely no sense to me.

What I do understand are the simple principles of …

‘The higher you climb, the harder you fall’.

‘There is no such thing as a free lunch’.

‘The only capital guarantee worth diddly is one offered by a AAA rated Government — backed by its own printing press’.

‘Expansion and contraction, inhale and exhale, yin and yang’.

‘For every action there is an equal and opposite reaction’.

‘Reversion to the mean’.

‘Vested interest trumps your interest’.

‘You buy low and sell high’.

‘Trees do not grow to the sky’.

‘There is no new way to go broke, it is always too much debt’.

None of this home spun wisdom is particularly earth shattering or offers any great revelations. It just plain old common sense…a commodity that becomes less common in a boom.

What I can tell you — with absolute certainty — is that when the next crisis does hit, the number of hard luck stories you’re going read or hear about (lost fortunes, shattered dreams and the indefinite postponement of retirements) will ALL have one thing in common…ignorance or contempt for one or more of these simple time-proven principles.

Please permit me to leave you with…

One simple question

The investment industry has (repeatedly) stressed the importance of ‘buy and hold’…in the long run shares always go up.

Given the market’s sustained recovery since the dark days of 2008/09, investors are willing to embrace the ‘buy and hold’ philosophy.

That’s fine, but to find out how committed you are to this philosophy, ask yourself this one question…

‘After the market has wiped out more than 50 percent (or more) of your portfolio, how strong will your impulse be to change your philosophical approach and ‘cut and run’ for the safety of cash?’

Until you’re put under the pressure of a market in freefall, it can be a little difficult to create the emotional response to this hypothetical scenario.

But what we do know from the data is that when times get tough, those who were once tough get going…out of the market.

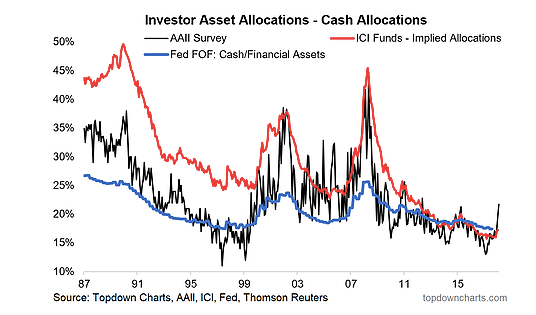

The following chart tracks three asset allocation indicators…

AAII — American Association of Individual Investors (black line)

Fed FOF — US Federal Reserve Flow of Funds report (blue line)

ICI Mutual Fund data (red line)

|

Source: Top Down charts |

Look at the spikes — especially in the red line of managed funds — in 1987, 2000 and 2008.

All times of historic collapses in the US market.

In times of market upheaval, investors — amateur and professional alike — abandoned their philosophical approach.

If your answer to the question is anything less than an unequivocal ‘I will absolutely stay the distance’, then in my opinion, your decision should be a simple one…sell up before the next major crisis hits.

Regards,

Vern Gowdie

Vern Gowdie has been involved in financial planning in Australia since 1986. In 1999, Personal Investor magazine ranked Vern as one of Australia’s Top 50 financial planners. His previous firm, Gowdie Financial Planning, was recognized in 2004, 2005, 2006 & 2007, by Independent Financial Adviser magazine as one of the top five financial planning firms in Australia. He is a feature editor to Money Morning NZ and is Founder and Chairman of the Gowdie Family Wealth and the Gowdie Letter advisory services.