Of course looks matter.

An attractive woman or man is irresistible at first.

Anything and everything they say is interesting. And the fact that so many other people think so too, makes them that much more attractive.

I’m sure you have felt this before. And hopefully you still feel the same way if you’re in a long-term relationship.

But looks only last for so long. If there’s no substance behind that pretty face, then it might be hard to keep the embers burning at night.

They might seem smart and witty at first. But now you think most of what they say is garbage.

Worse yet is if you didn’t wake up to the warning signs early. Now it’s five to 10 years down the track and looks aren’t cutting it anymore.

You need someone who shares the same goals and values as you.

Choosing a partner is probably the most important decision you’ll ever make.

And I suggest you take the same approach to investing.

Let me explain how.

Should you get serious with Qantas?

We all have our type don’t we? Features that float our boat.

Well it’s the same with businesses.

You don’t want just any old business. You want one that has potential to grow. Maybe it’s got healthy margins to start off with. And it’s probably got a lot of other investors knocking on its door.

But often investors will just go for the good looking business and not bother to find out more about the details.

I’ll use the airline business as an example. Take a look at Qantas Airways Ltd [ASX:QAN].

When you think of Aussie airlines, Qantas is probably the first name that pops into your head.

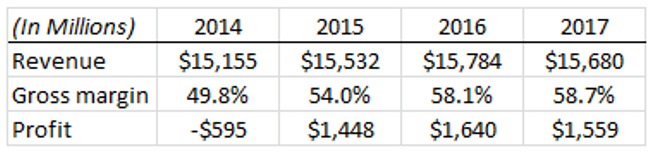

Since 2014, the group has shown tremendous growth. Sales have been more or less the same. But Qantas has managed to reduce the cost of sales (gross margin) and grow profits in a big way.

Source: MorningStar

[Click to open new window]

Better yet, there could be more growth around the corner. According to Bloomberg, not only are pilots in short supply, but so too are runways.

From Bloomberg:

‘With global passenger numbers forecast to almost double to 7.8 billion by 2036, runways, airports and even airspace could rapidly become too crowded to cope. In Asia, which will contribute more than half of the extra flyers, many terminals are already full to bursting.’

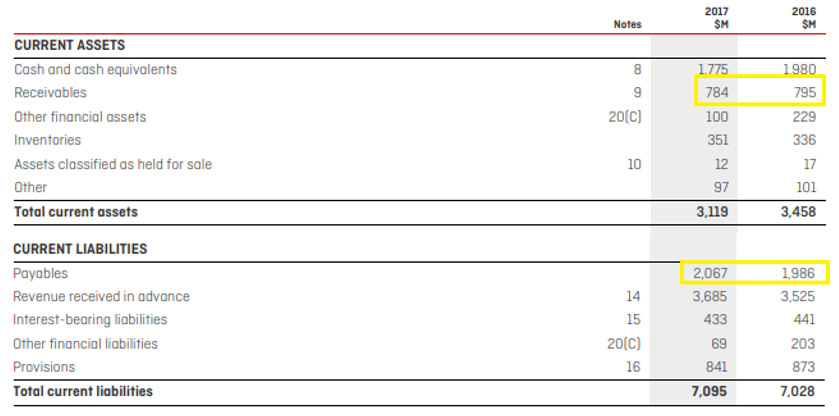

What’s more, Qantas’ accounts look great.

They can receive ticket sales up front, and then pay costs at a later time. You can see this from the difference in receivable and payable accounts.

Source: Qantas Airways 2017 Annual Report

[Click to open new window]

And because Qantas can rent planes instead of own them, they’re able to earn a very decent return on equity (shareholders capital).

Clearly Qantas is an attractive company. It’s why investors have bid up the stock 325% since late 2014.

Yet if we look at the company over a longer period (since inception), there’s a lot to be desired.

The stock is up around 78%. Over 19 years that’s a 3.1% return annually.

Surely if Qantas was a wonderful business, they would be up far more than that?

But that’s because Qantas, and most other airline companies, have crucial flaws. They’re selling a service where price rules above everything else.

Every airline enjoys the same benefits as Qantas. They all collect sales up front. They can all lease their planes instead of owning them.

The aim of the game is to capture as much of the market as possible. And to do that, airlines have to lower their prices.

It essentially boils down to a race to zero.

The way I see it, Qantas is beautiful, but not something you want to hold onto forever.

Look for businesses that get better with age

So how do you then pick a company with personality?

Well, they don’t necessarily have to look the best. But they do have to have a business which gets better over time.

Take REA Group Ltd [ASX:REA] (owner of realestate.com.au) as an example.

REA Group has the best of both worlds. They look amazing, plus their business gets better over time.

Consider what happens when REA increases their network of buyers and sellers. With more people on their platform it gives existing users more choice.

It also encourages more potential buyers to jump onto their site, encouraging more sellers to jump on as well.

For REA, the aim of the game is to build the strongest network possible. If they can do that, they win. Buyers and sellers will automatically look for and list property on their site.

And because they’re essentially locking in this network, they can raise advertising revenues at will.

So not only is REA growing sales, earnings and equity at an amazing rate. It’s also a business that gets stronger over time, which increases the certainty of future earnings.

All you have to figure out whether companies like REA Group are worth the price they’re trading for.

Your friend,

Harje Ronngard

Harje Ronngard is one of the editors at Money Morning New Zealand. With an academic background in finance and investments, Harje knows how difficult investing is. He has worked with a range of assets classes, from futures to equities. But he’s found his niche in equity valuation. There are two questions Harje likes to ask of any investment. What is it worth? And how much does it cost? These two questions alone open up a world of investment opportunities which Harje shares with Money Morning New Zealand readers.