‘It ain’t what you don’t know that gets you into trouble.

It’s what you know for sure that just ain’t so.’

—Mark Twain

Lately, I’ve been thinking a lot about risk.

Specifically, I’ve been thinking about the risk-to-return ratio.

It goes like this: How much risk are you willing to endure in order to achieve the return that you have in mind?

In theory, this should be a simple enough question to answer. People who are courageous lions should take on more risk and chase higher returns. Meanwhile, people who are scaredy cats should take on less risk and settle for lower returns.

This formula is easy enough to follow. Right? Right?

Well, no. Because when it comes to human psychology, it’s never that easy. Because people have a habit of making wrong calls. They do it all the time.

For example, I still remember the heady days of 2020. That’s when I met a friend who was bullish on Auckland housing. He said: ‘Property prices will never go down. They will only go up. Mortgages are risk-free.’

Risk-free? Really?

Well, I can’t blame him for thinking that way. Like most Kiwi millennials of a certain age, he had only known good times. He couldn’t conceive of the possibility that his confidence could be misplaced.

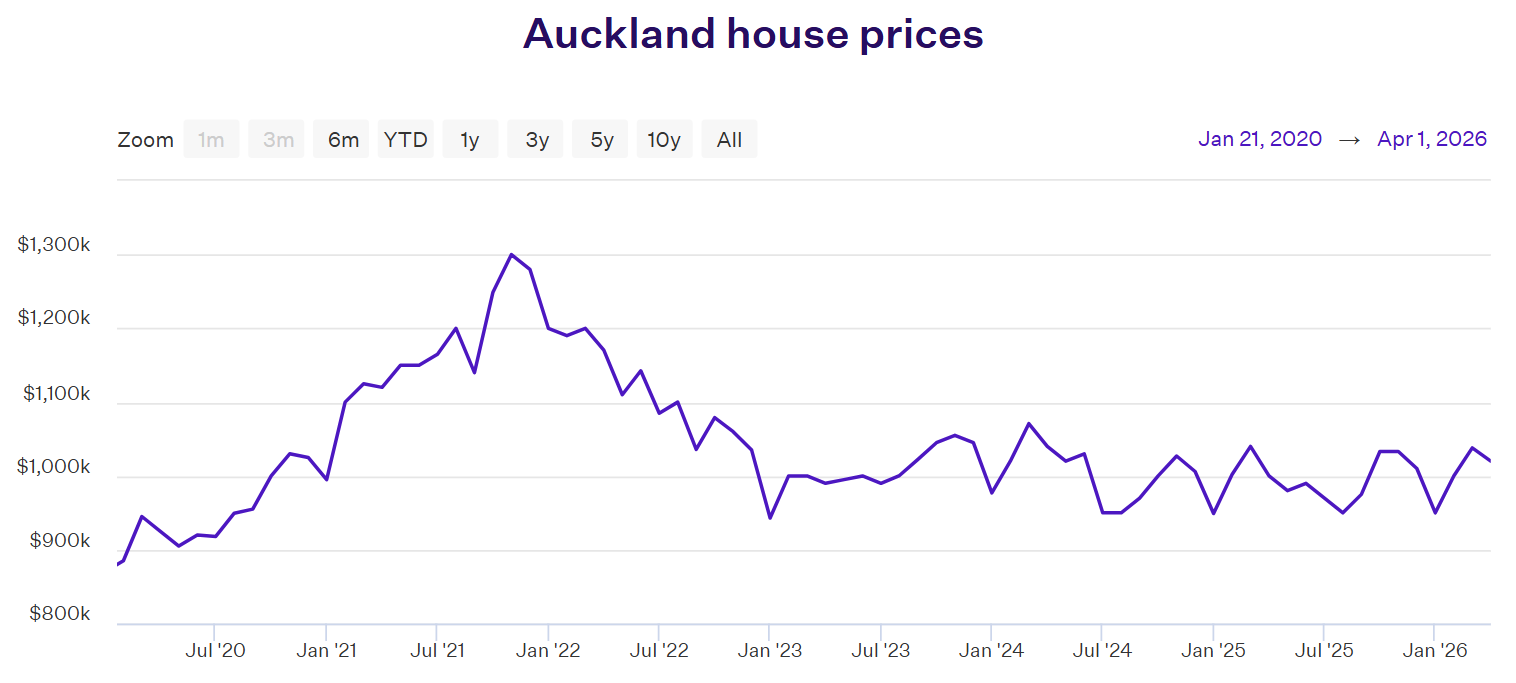

And then this happened…

Source: Opes Partners

Ouch. What happened here? Well, to make sense of the Auckland property market, you first need to understand how the sequence of events unfolded:

- In late 2020, the average floating mortgage rate dropped to a low of 4.19%. And house prices responded accordingly, escalating at a feverish rate.

- Not surprisingly, a lot of people were seized by FOMO. They rushed to commit themselves to large mortgages. They wanted to get in on the price action.

- Some of them bought close to the peak in November 2021. Just before prices softened and crumbled. It was devastating for them.

- To make matters worse, their pain and suffering were amplified when the floating rate effectively doubled. It reached a high of 8.55% by late 2023.

Since then, the rate has softened to 5.72%. But that doesn’t offer much comfort, does it? Because the damage to the national psyche has already been done.

- Right now, we are in Year 4 of the Great Kiwi Housing Disaster. Will this stretch into Year 5? Yes? No? Well, my feeling is that you won’t get any clarity from the economists.

- In 2023, they predicted 5–6% growth for the market. But nothing of the sort happened. In fact, we got quite the opposite. House prices continued to slide.

- Then, in 2024, some economists predicted 3–5% growth. Others were more optimistic, anticipating 7–8%. But nope. They were all wrong. The market stayed weak.

- In 2025, they made predictions of 5–10% growth. But guess what? Tragically, they were totally wrong again. The market remained anaemic.

Laurence J. Peter once said: ‘An economist is an expert who will know tomorrow why the things he predicted yesterday didn’t happen today.’

- Perhaps the truth is an uncomfortable one. Our housing boom is over. The speculative bubble has popped. And what follows could be a painful period of adjustment.

- If you have a stake in Kiwi property, then you will need to be prepared for what comes next. Here are 3 Urgent Signals, flashing bright red, that I’m watching right now…

Your first Quantum Wealth Report is waiting for you: