Let’s take a trip down memory lane.

Do you remember where you were in 1996?

Do you remember what life was like back then?

Well, in 1996, I was just starting high school in Malaysia. It was a new educational experience. A new social circle. A new phase of life.

I didn’t know it at the time, but I was experiencing the midpoint of what National Geographic would come to call ‘The Last Great Decade’.

The Cold War was over. The global economy was accelerating. And pop culture was filled with bubbly enthusiasm.

During this period, I remember watching the sitcoms that were running on television.

Seinfeld. Friends. Frasier. Home Improvement. Everybody Loves Raymond. The Nanny. 3rd Rock from the Sun.

What did these shows have in common? Well, they explored the American dream: life, liberty, and the pursuit of happiness.

You had a community of family and friends. Tight-knit, loyal, devoted. Figuring out the journey together. The comedy was funny, yes, but the moral message was even better: all our human problems were ultimately fixable, even if it took a few humorous errors to get there.

This sunny optimism seemed to extend to the world of finance as well.

I recall that the influence of one man — a central banker — loomed large over that decade.

He was the wizard with a magic wand, sprinkling fairy dust, enchanting the world with positivity. This made him more relevant than any celebrity. More powerful than any politician.

Source: The Bureau of Engraving and Printing / Wikimedia Commons

Yes, that’s right. I’m talking about Alan Greenspan. Perhaps the most dominant Federal Reserve chairman ever.

- His famous ‘Greenspan put’ was the idea that the Fed would act as the ultimate safety net. The ultimate shock absorber. Always stepping in to cushion the market from any turbulence. This was responsible for easy-money policies, extending a legendary bull run that first started in 1990.

- Inflation was low. Borrowing was cheap. Consumer spending boomed. It was the perfect combination, delivering tailwinds that supercharged the American economy.

- Yes, these were buoyant years. Where you could step outside your comfort zone. Take a risk. Invest in a business. And chances are, it would pay off handsomely.

But then, in December 1996, Alan Greenspan gave a televised speech. Surprisingly enough, he appeared to tap the brakes a little bit on the risk-taking. Here’s what he said:

‘Clearly, sustained low inflation implies less uncertainty about the future, and lower risk premiums imply higher prices of stocks and other earning assets. We can see that in the inverse relationship exhibited by price/earnings ratios and the rate of inflation in the past. But how do we know when irrational exuberance has unduly escalated asset values, which then become subject to unexpected and prolonged contractions as they have in Japan over the past decade?’

Oh boy. It was like a gunshot had gone off. Greenspan’s words were thick with complicated jargon, but it was enough to cause an emotional reaction.

- He used a curious phrase: ‘irrational exuberance’. This was elegant Fedspeak, which translated into plain English, could be interpreted to mean ‘speculative bubble’.

- At this point, imaginations went wild. The pessimists and permabears pounced on Greenspan’s phrase. They said that it was a sign that doomsday had arrived. A devastating crash was imminent. Absolutely. Guaranteed.

But, of course, timing the market is never that simple, is it? Here’s how the timeline played out:

- 1996 came and went. There was no apocalypse. The market kept climbing.

- 1997 rolled around. No catastrophe. The market kept climbing.

- 1998 slid past. Everyone shrugged. The market kept climbing.

- 1999 arrived with balloons and confetti. A new millennium beckoned. The market kept climbing.

- But then along came March 2000. And that’s when the market finally — finally — peaked. The dot-com bubble burst. Large-cap tech stocks, in particular, suffered a sharp decline.

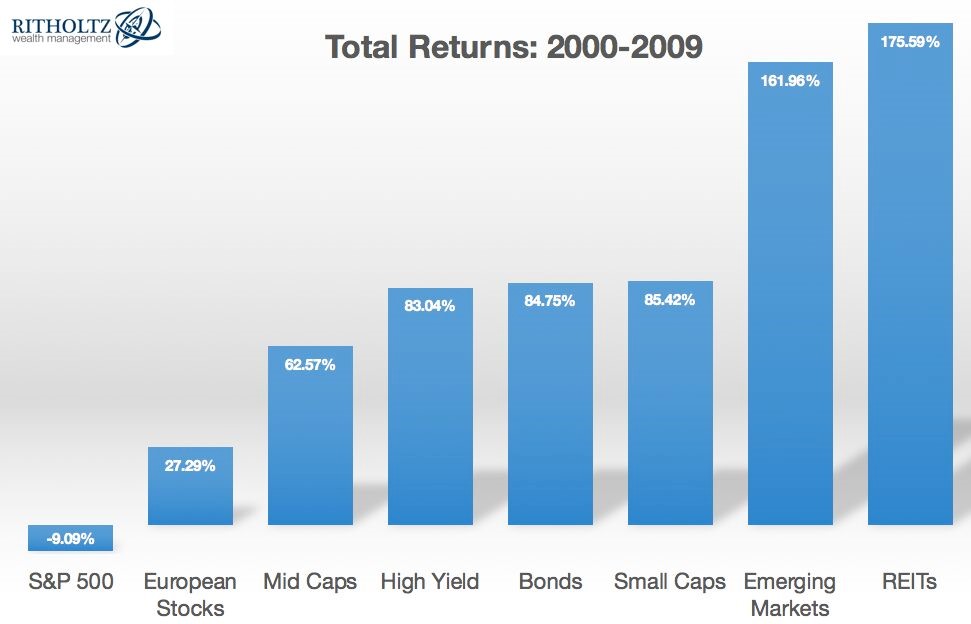

Source: Ben Carlson / LinkedIn

So, was this an ‘aha moment’? Was this the disaster that the prophets of doom had been forecasting? Well, not quite.

- You see, the bursting of the dot-com bubble wasn’t actually the end of the story. It was actually about turning a fresh page. Starting a new chapter. Embracing new opportunities.

- While the large-cap S&P 500 floundered, other asset classes stepped in to fill the gap. What we saw was a remarkable rotation from growth stocks into value stocks.

- In other words: the transition from the 1990s to the 2000s wasn’t a catastrophe. It was simply the next stage of the cycle. And investors who caught this new wave were ideally positioned to prosper.

Of course, with the benefit of hindsight, you can already see that talking about economic cycles is a lot easier than predicting them in advance.

- At the moment, in 2025, we’re in the midst of an AI boom. Tech stocks are soaring. Capital expenditure is projected to run into the trillions.

- So it’s worth asking: is this another dot-com bubble? If so, are we closer to 1996 or 2000? And more importantly, is it time to embrace a rotation into value stocks that could outperform beyond this current cycle?

- Well, if you’re a forward-looking investor, here are 5 Urgent Signals you can’t afford to ignore. The trend lines here are incredibly revealing. You need to study each one closely…

Your first Quantum Wealth Report is waiting for you: