One of our wholesale clients raised an interesting question recently.

Why is actual wealth and feeling wealthy very different things?

He then gave an interesting insight on the psychology of wealth:

‘Having never had great swathes of cash rolling in, I still feel on a knife-edge financially despite the net [worth] being theoretically good. I have a hardship mindset, which is so ingrained; I would probably not feel financially secure at 10x my current wealth.’

I suspect many Kiwis feel this way. I have a hardship mindset — growing up in Taranaki in the ‘70s and ‘80s will do that.

The elephant in the room is housing investment

New Zealand wealth has been built on it. Our property values are among the highest in the world, especially in our major cities.

Yet home values don’t seem the surefire path to prosperity they once were.

Further, coming back to hopes for ‘swathes of cash rolling in’ — our propensity to invest in housing has actually operated as a form of forced saving, with little income growth.

Let me explain. I bought my first home in Royal Oak, Auckland in 2000 when I was 25 years old. With my Taranaki mentality in place, I took in flatmates and worked like a demon to pay off the mortgage.

Source: Author

When I got married and moved to the North Shore some years later, we borrowed on Royal Oak to fund a bigger home with a sea view. Royal Oak became a rental investment and a form of forced saving. But in hindsight, compared to investing in shares, it was probably cash-weak.

- Approximate value (at time of rental): $480,000

- Rent: $480. Gross yield: 5.20% p.a. ($24,960)

- Mortgage: $320,000. Average rate: 6.5% p.a. ($20,800)

- Assume 2% capital allowance for maintenance and rates: ($9,600)

- Net cash flow = –$5,440 or –1.13% p.a.

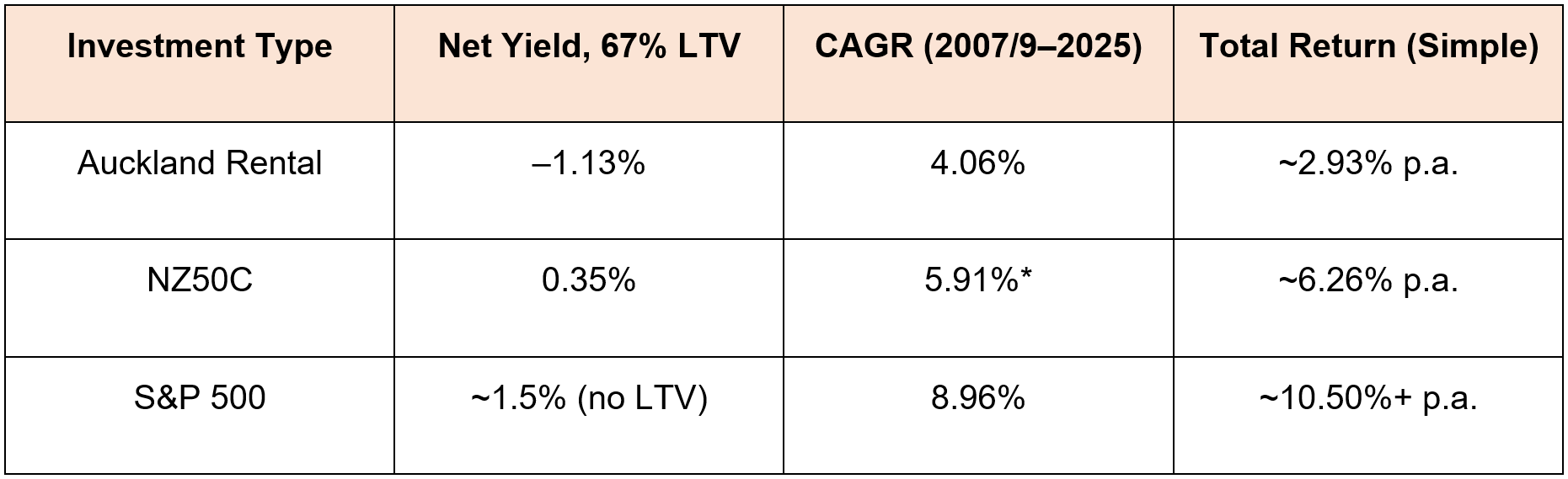

- CAGR of property 2007 to 2025: 4.06% p.a.

This investment had a net return of roughly 2.93% p.a.

Considering the property is now worth $980,000 and was last rented at $750 (gross yield of 3.98%) the forward scenario might be worse.

Compare that to buying and holding value shares

For simplicity, we’ll look at the NZX 50 Capital Index:

Source: NZX 50 Capital Index / Google Finance

Taking into account fluctuations, a reasonable estimate for the average dividend yield across the NZX 50 from 2009 (since figures available) to 2025 would be approximately 4.6%–4.8%

- Assume average dividend yield has been 4.7% p.a.

- CAGR of index price 2009 to 2025: 5.91% p.a.

- Assume margin lending at 67% (as per property) at 6.5% p.a. leaves net yield of 0.35% p.a.

This investment could hypothetically have had a total simple return of 6.26% vs. 2.93% p.a. for the ‘prime location’ Auckland rental. Note: this is hypothetical, as lending ratios on stocks vary, are generally lower, and may add significant risk. Margin lending is for experienced investors.

Further, global markets have outperformed New Zealand. For example, the S&P 500:

Source: Google Finance

While the dividend yield is lower, the CAGR is almost 9%. (The S&P 500 has a long-term average yield of around 1.5%.)

To summarise this:

(Hypothetical scenarios only. Actual returns may differ. *NZ50C from 2009–2025)

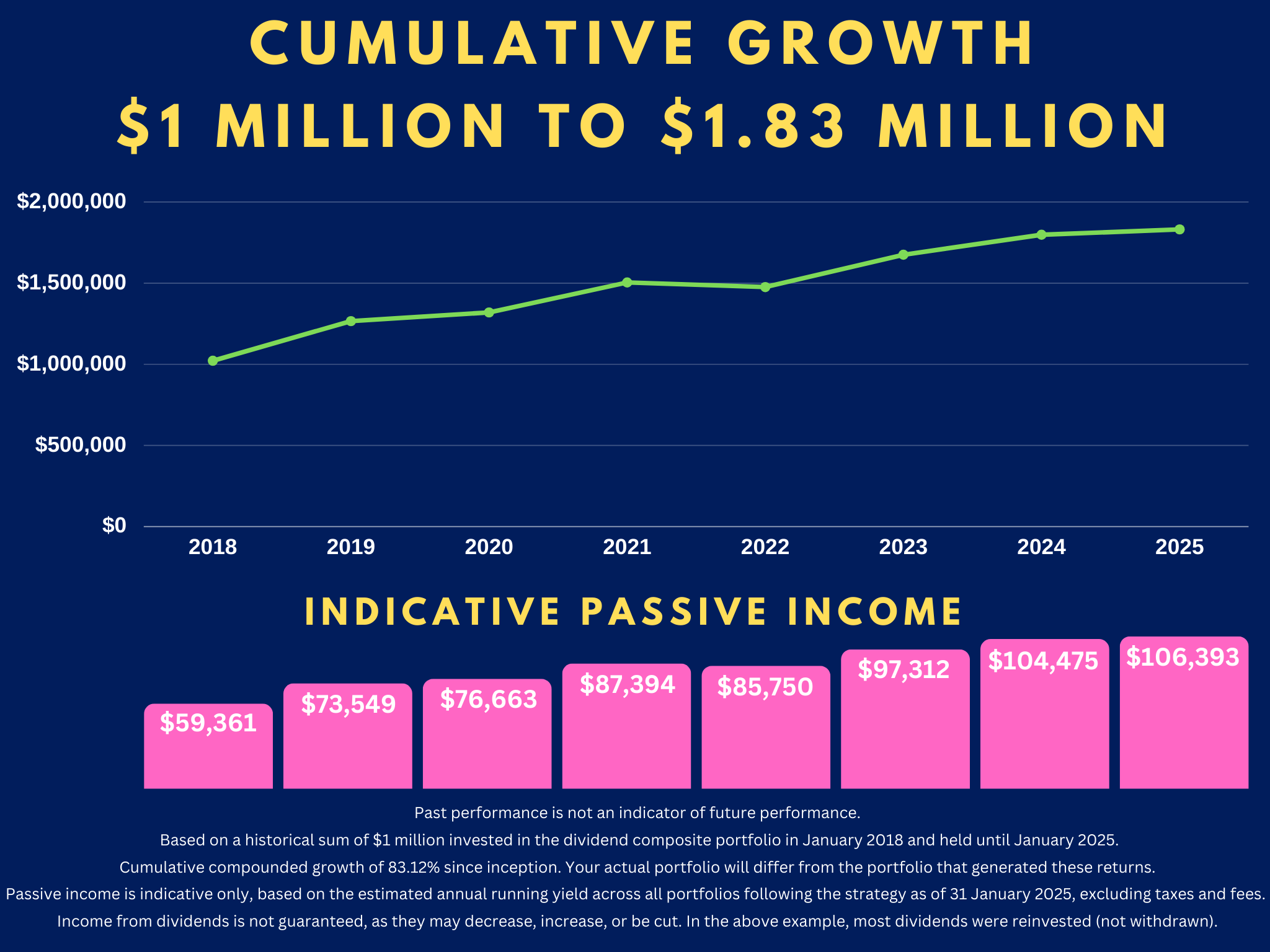

In our wholesale strategy, focusing on the best value and income picks we can find across global markets — we are targeting quite a bit more.

Many investors focus on capital growth over dividends. I would argue dividends can form a significant part of the long-run returns, particularly when allowed to compound. The above analysis has focused on simple returns only.

Shifting beyond the hardship mindset

You can’t deny that property, for many Kiwis, has been a good investment from a capital accretion point of view.

As I mention, it’s often been a form of forced saving. You don’t often see ‘swathes of cash’ until the properties are sold. It’s hard to see meaningful passive income until mortgages are paid down. Even then, yields still seem low when you consider maintenance costs. Not to mention your time.

For many, the emotional security of bricks and mortar outweighs the mathematical case for diversification.

As term deposits drop into the 3% band, the search for meaningful passive income becomes more important.

Personally, I managed to shift out of my hardship mindset by building a share portfolio.

This involved calculating the income needed to sustain a certain lifestyle.

Then building the investment strategy to underwrite that. The same approach we have replicated for our wholesale clients.

Once the portfolio is in place, the surplus becomes something to enjoy — so long as the compounding of capital remains uninterrupted.

Are you looking to invest for financial freedom?

Here at Wealth Morning, our investment strategy is value-focused across developed markets, with a focus on opportunities beyond the usual radar.

We aim to build up strong and income-rich portfolios for our Eligible and Wholesale Clients. It’s a true partnership where the Principals’ own money is invested in the same strategy.

If this resonates with your own investment journey, we’re happy to explore how our strategy might align.

- Do you have previous experience in investing?

- Are you a sophisticated investor?

- Or have you built significant wealth?

All these characteristics could qualify you as an Eligible or Wholesale Investor for a managed account under our strategy. The assets remain in your name, and you retain full ownership and custody of your assets.

We are currently offering free consultations on this opportunity.

Regards,

Simon Angelo

Editor, Wealth Morning

(This article is the author’s personal opinion and commentary only. It is general in nature and should not be construed as any financial or investment advice. Please contact a licensed Financial Advice Provider to discuss your personal situation. Wealth Morning offers Managed Account Services for Wholesale or Eligible investors as defined in the Financial Markets Conduct Act 2013.)