I find it relaxing watching lifestyle shows about life in Italy.

Why? The good life is more affordable than in New Zealand.

This is Ristorante La Reggia on the coast at Galatone, Puglia. In the heel of Italy’s boot.

Source: La Reggia Restaurant

You can get a pizza laden with fresh prawns for €12 ($23.30), and a nice bottle of wine for €10 ($19.40). All up, about half what you may pay for less here in Auckland.

Then if you decide to stay, you could buy a five-room house in nearby Nardo for €135,000 ($262,000).

Source: Idealista

Now, what I’m failing to consider here is purchasing power disparity.

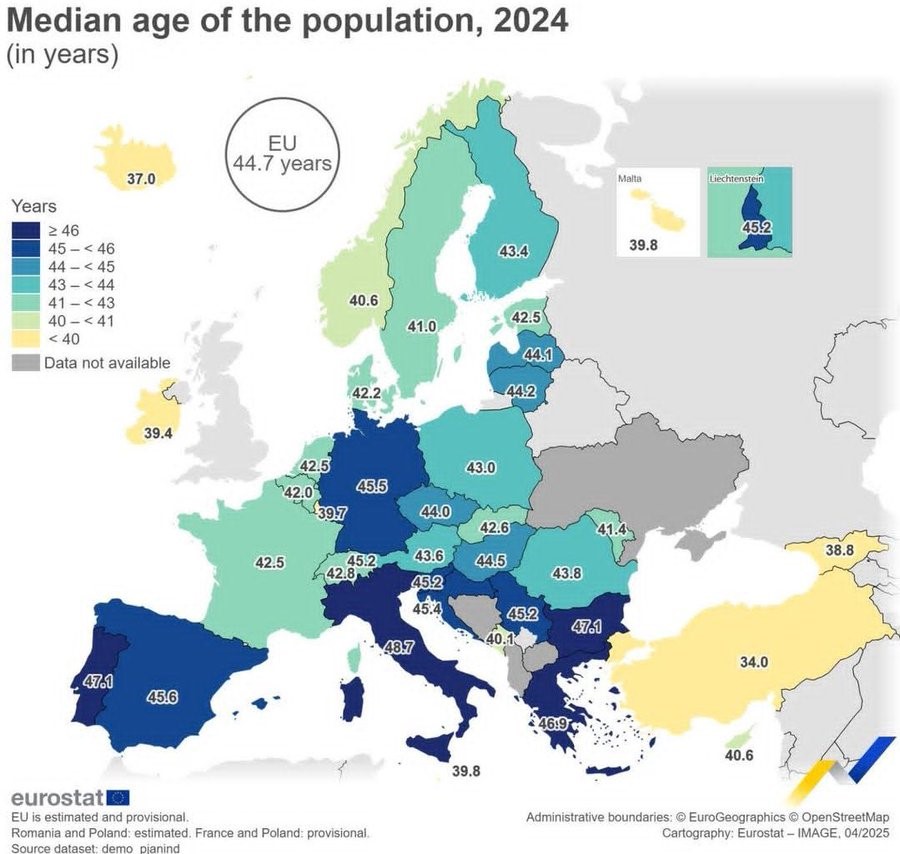

Even though the Euro is at historic highs against the Kiwi dollar, the typical New Zealander (or Australian or American) sees strong purchasing power in Italy. There are many reasons for this: from the property wealth effect to our GDP per capita being about 20% higher. This becomes more pronounced when visiting Southern Italy.

One overlooked reason for this is superannuation

Source: Michael A. Arouet / X

Today, superannuation in Italy takes almost 16% of GDP. The country skirts fiscal pressure with high debt.

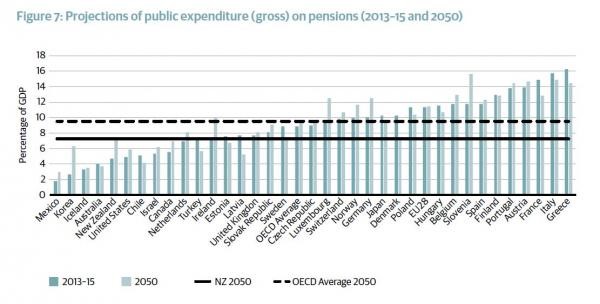

In New Zealand, the figure for Super is at around 5% of GDP. Over the next 30 years, that is expected to reach 8%.

Despite what we’re constantly told, NZ Super is relatively affordable. Compared to many other OECD countries, our pension costs and even projected costs are modest.

Source: The New Zealand Initiative / OECD

Of course, it’s important to understand that NZ Super provides only a basic level of income. It won’t be enough on its own to maintain the lifestyle many Kiwis are accustomed to.

There’s also a key difference in the way that pensions are funded.

For that reason, the Italian system is unlikely to collapse.

Italy has a ‘defined contributions’ style system

Because the dependency ratio is broken (too many older retired people versus younger working people), the system works on a ‘pension pot’ basis.

- Italians can claim a state pension at 67 after contributing for at least 20 years.

- The state pension is funded by social-security contributions from workers and employers. These take around 40% of the employee’s earnings.

- The employee puts in 10%, and the employer 30%. About a third of those contributions go toward the pension. (The rest is for unemployment, sickness, maternity, etc.)

- The calculation of your pension is complex. It depends on the contributions you’ve made to your ‘pension pot’, Italy’s GDP growth, and probabilities around death.

In other words, higher paid workers will have a larger pension pot. When they retire, this is annuitised and converted to a stream of payments. For those with insufficient pension pots, the state does step in to underwrite a minimal level of support.

Unfortunately, the extent of these taxes and contributions mean many workers have little left. While this, in part, explains why Italy seems affordable to visitors, it skews local incentives.

Younger skilled people emigrate. Those who remain often struggle to afford starting families of their own. Many remain living with their parents well into their 30s. Levels of tax evasion are among the highest in Europe — a practice some regard as ‘defence against the state’. Reports suggest evasion is as high as 27% of GDP.

The flip side is that, at some point, the older cohort will die out, the population will be smaller, and the dependency ratio is reset.

Meanwhile, there is economic opportunity from policies to attract migrants, draw high-net-worth individuals (who can fund their own retirement), and provide tax cuts for business and self-employment.

New Zealand has a ‘defined benefit’ style system

Superannuation is universal in New Zealand from age 65, providing you have lived here for at least 10 years since age 20. From last year, this is gradually going to increase to 20 years.

For a couple who both qualify, even if they are still working, the amount before tax is currently just under $50,000.

Unlike Italy (or Australia), there are no defined contributions or ‘pension pots’ with the state system. It is funded from the tax take.

Crucially, it treats all earners equally. Those with lower lifetime wages receive no less than those with higher incomes.

Lake Wanaka fishing. Source: Image by Sasà from Pixabay

Providing the dependency ratio holds up — there are enough workers to make the system economic — it can work very well.

Unfortunately, we too have an ageing population.

NZ Super is already 18% of the tax take. That’s expected to rise to 21% over the next decade.

Let’s not repeat Italy’s mistake: letting pension (and healthcare) costs choke growth

Sadly, that is exactly the path the Opposition seem to be progressing. They’re talking about capital gains — even wealth and inheritance tax — on the ground that ‘Super is unaffordable’.

This is a zero-sum game. You push productive and prosperous people overseas. High taxes make it less worthwhile to invest in businesses, farms, or family formation.

Eventually, the system breaks down. You are forced to move to defined contributions — ‘pension pots’. There is less incentive to invest privately, since the state forces growing contribution levels. Fairness in retirement evaporates.

Actually, if the previous government hadn’t overspent on its Covid response, the country would be facing a much lower interest bill and Super affordability would look better.

The universal system is a good one if you can incentivise growth amongst the earning population. Note: I said ‘earning’, not necessarily ‘working’.

In our business, we see individuals in their 70s and beyond still with significant investments and business interests. Yes, they receive NZ Super. Often, they are paying more tax than the pension itself. Then their pension is taxed at the top rate, 39%.

NZ Super is beautiful because it underwrites basic support in later life

For it to remain affordable, the key is GDP growth. Here are some key ways New Zealand can achieve this:

- Encourage household formation — crucially, by bringing housing costs down.

- Incentivise new industries and the economic benefits of our resources and commodities sector across a low population.

- Forget the climate emergency. There is nothing New Zealand can do anyway. Focus on the fertility emergency instead. Promote and incentivise the value of marriage and children to the economy.

- Cut company taxes, incentivising new businesses to start and move here.

- Tax what you don’t want — not what you do. So don’t tax capital, investment or exporting. Tax imported consumption.

- Encourage quality migration. Those with the wealth or skills to add to per capita GDP, not reduce it.

- Keep the state to the essentials, such as supporting our golden age, good health and public safety.

- Tax burden to GDP is over 43% in Italy, but their pensions are 16% of that, and debt servicing 7%.

- Tax burden in NZ is 34%, but pensions are only 5% of that, and debt servicing 3.4%. Clearly, we’re wasting money on a lot of unnecessary stuff.

So, if you believe in the fairness of universal superannuation and value its future, well, it might be time to DOGE Wellington and get back to basics.

Source: Michael A. Arouet / X

Are you looking to invest for growth and income beyond Super?

Here at Wealth Morning, our investment strategy is value-focused across developed markets, with a focus on opportunities beyond the usual radar.

We aim to build up strong and income-rich portfolios for our Eligible and Wholesale Clients. It’s a true partnership where the Principals’ own money is invested in the same strategy.

We’d love to get a sense of your investment journey:

- Do you have previous experience in investing?

- Are you a sophisticated investor?

- Or have you built significant wealth?

All these characteristics could qualify you as an Eligible or Wholesale Investor for a managed account under our strategy. The assets remain in your name, and you retain full ownership and custody of your assets.

We are currently offering free consultations on this opportunity.

Regards,

Simon Angelo

Editor, Wealth Morning

(This article is the author’s personal opinion and commentary only. It is general in nature and should not be construed as any financial or investment advice. Please contact a licensed Financial Advice Provider to discuss your personal situation. Wealth Morning offers Managed Account Services for Wholesale or Eligible investors as defined in the Financial Markets Conduct Act 2013.)