Rod was interested in DIY investing. He had a good business and a mortgage. But wanted to get ahead faster. So when a new broker from Australia set up in the local market, offering low-cost access to global stocks, he jumped at the chance.

Halifax New Zealand was widely promoted. It offered access to a deep pool of financial instruments and markets.

Yet, for the past two years, clients have been waiting for some or all of their money back. After the Australian headquartered firm went into liquidation in March 2019.

Rod is just one of many of those clients who had thousands of dollars tied up with Halifax. He is unsure how much money of his money he will get back. And when that will be.

You can imagine the stress. The disappointment. And the impact on his other financial goals — such as being able to pay down his mortgage or invest elsewhere.

What went wrong?

When you buy financial assets through some brokers, they may act as your ‘nominee’. This means they hold those assets for you. On your behalf. In the case of shares — it is the broker’s name that appears on the share registry. They might be holding parcels of shares in various companies for thousands of investors.

Now, the assets such broker holds for you would normally be held in ‘segregated accounts’. Often in a separate custodian company. The accounts of that custodian should be audited on a regular basis.

Unfortunately, in the case of Halifax, liquidators reportedly found comingling of accounts.

In other words, Rod’s money — that should have been in a segregated and protected account — could, in fact, have been mixed in with other funds used to try and bail out the business.

How do you avoid this and protect your money?

The nominee situation may not be ideal. It ultimately means you do not directly own the financial assets in your name. They are being held for you by the broker.

But if you’re investing globally — outside of New Zealand and Australia — it is usually the most cost-effective way. And in jurisdictions such as the UK and North America, the nominee system is the normal method.

Yet, these jurisdictions have compensation arrangements — which I’ll come to in a moment.

When buying shares in New Zealand and maybe Australia, I see no need to use nominee arrangements

At least one major bank broker here affects direct trading. Meaning, when you buy shares, you own those shares directly in the company on their share registry.

This option is only a little more expensive than some of the nominee arrangements promoted here. For example, by certain gamified apps that promise to make investing available to all.

Investing is already available to anyone with just a few thousand dollars.

Buying shares direct on the register — through a bank-broker, for example — essentially removes broker risk. The only risk you run is that the broker makes a mistake with your order. But the sole risk to the actual ownership of your shares is if the company in which you buy shares in gets into trouble. And, of course, you’d normally diversify across many companies to mitigate that.

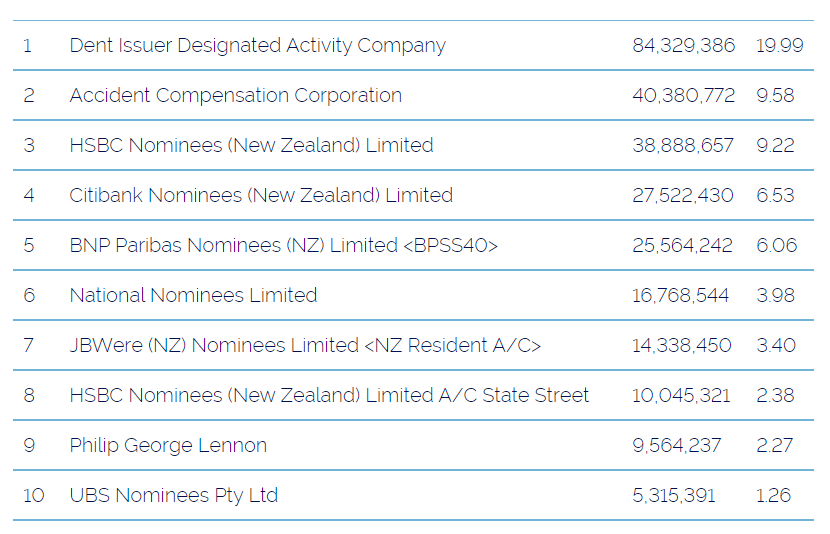

Here’s an example of direct v. nominee holdings referencing the top 10 shareholders of Tower Insurance [NZX:TWR] as at 26 March 2020:

Source: Tower Investor Centre

Above, we can see some direct registry shareholders such as the Accident Compensation Corporation (ACC) and Philip George Lennon. We can also see some broker nominees (holding shares for many investors) such as HSBC Nominees and JBWere Nominees.

Global investing will typically require you to use a nominee

When investing outside Australasia, there may not be a direct-broking service available. You will need to use a nominee service through one of the banks or large electronic brokers.

You then need to make these checks:

1) How financially robust is the broker you plan to use?

Review their years in business. Their financial rating — by a ratings agency such as Standard & Poors. Their registration with the local regulator such as FINRA in the US or the FCA in the UK. And their financial health — in particular, any long-term debt they’re carrying.

Many of the larger brokers are themselves listed on stock exchanges. Meaning you can easily review their financial information.

2) Ensure the broker uses strictly segregated accounts

This is usually ruled by the regulator. But it can pay to make additional investigations and ensure that your assets will be in a segregated account and custodial arrangement away from the broker business. You need to be sure there can be no comingling across any part of the business — as was allegedly the problem with Halifax.

3) Review compensation and insurance arrangements in place

Where does the buck stop?

Having worked in offshore finance, it remains shocking to me that New Zealand does not offer compensation arrangements for clients of brokers or banks.

If a broker or bank goes bust and they have taken funds from segregated accounts — which they can access — you may have little further recourse except via the liquidation process. Halifax again.

I came across one firm that offered brokerage services. On closer inspection of the custodian, I found that they were using a Chinese brokerage firm as the nominee. Given China is a communist nation, and there is the potential for government influence in private business, this should arouse caution.

Brokers in developed financial markets such as the US or the UK will typically offer compensation arrangements via SIPC (Securities Investor Protection Corporation) or FSCS (Financial Services Compensation Scheme).

In the event of broker failure in the US, investors with SIPC registered members are covered up to USD 500,000 regardless of country of residence.

And in the UK, FSCS registered firms cover up to £85,000.

The bottom line

When investing overseas, it can pay to make the three checks mentioned above. This will help you go some way to reducing any broker or custodian risk.

There are potholes and cliffs when investing for wealth and financial independence. No road in life is guaranteed safe. A smart investor considers all drivers of risk. From the investment itself. To the method in which it is held and deployed.

Do not be swayed by pretty, easy-to-use apps. Glossy marketing. Or the false sense of security that comes from a well-known or ‘famous’ name.

Bernie Madoff was one such famous name. Apparently, SIPC is covering some of the claims against the failure of his New York based firm. But, at this level, many investors may have held far more than $500,000 with Madoff.

So, if investing locally, it may be smarter to invest direct on the register and avoid nominee brokers. Which may carry some custodian risk without any compensation arrangement.

If investing globally, you may have to use a nominee broker. In that case, you need to make checks and be sure you’re happy for them to hold your money. And consider the worst-case scenario in every choice.

Regards,

Simon Angelo

Editor, Wealth Morning

PS: Wealth Morning works with a Global Managed Account service called Vistafolio. It is for Eligible and Wholesale Investors (not Retail Investors). A Managed Account service means you hold the assets in your own name with a regulated broker, and the Fund Manager has execution access only. For more information, please click here.

(This article is commentary and the author’s personal opinion only. It is general in nature and should not be construed as any financial or investment advice. To obtain guidance for your specific situation, please consult a licensed Financial Advice Provider.)