When you’re investing — running portfolios — you’re often juggling several vital objectives.

Preserving your capital. Generating increasing income to live. Growing your capital. Speculating on market events, sectors and trends.

The hedge-fund industry I was involved with in Europe is adept at managing these objectives.

Preservation of capital

For me and many of the investors I work with, the key objective is preservation of capital. For people who have already generated some wealth, it’s important to protect the downside and minimise any risk of loss or major drawdown.

I well remember some of my meetings with Family Offices and Trust Companies in Europe. One looked after one of the old shipping fortunes of England. The modern office floor was filled with old mahogany furniture and treasures on display from the ancient ships. Another had the largest collection of rare Scottish art in the world.

And we would show them portfolios that had achieved double-digit returns.

Then the penny would drop.

When your family has made (and retained) assets worth hundreds of millions of pounds over generations, your main concern is to protect that wealth — not necessarily double it over the next few years.

Generating income

As you go through life and build up some capital, you’ll notice there are two types of people.

- Those who become wealthy and financially independent by putting their money to work and optimising their capital.

- Those who save little and depend on their jobs.

Studies show many high-earning professionals often have lower levels of wealth than expected because they fail to put their money to work for them.

Highly-paid surgeons and doctors often fall into this category. Very high relative incomes. Net worth often tied up in unproductive assets like upscale homes, baches, boats and BMWs.

If you want to increase your income and have the option to be financially free — where you’re not dependent on your salary — you need to put your capital to work.

One way to do this is with a dividend-rich portfolio.

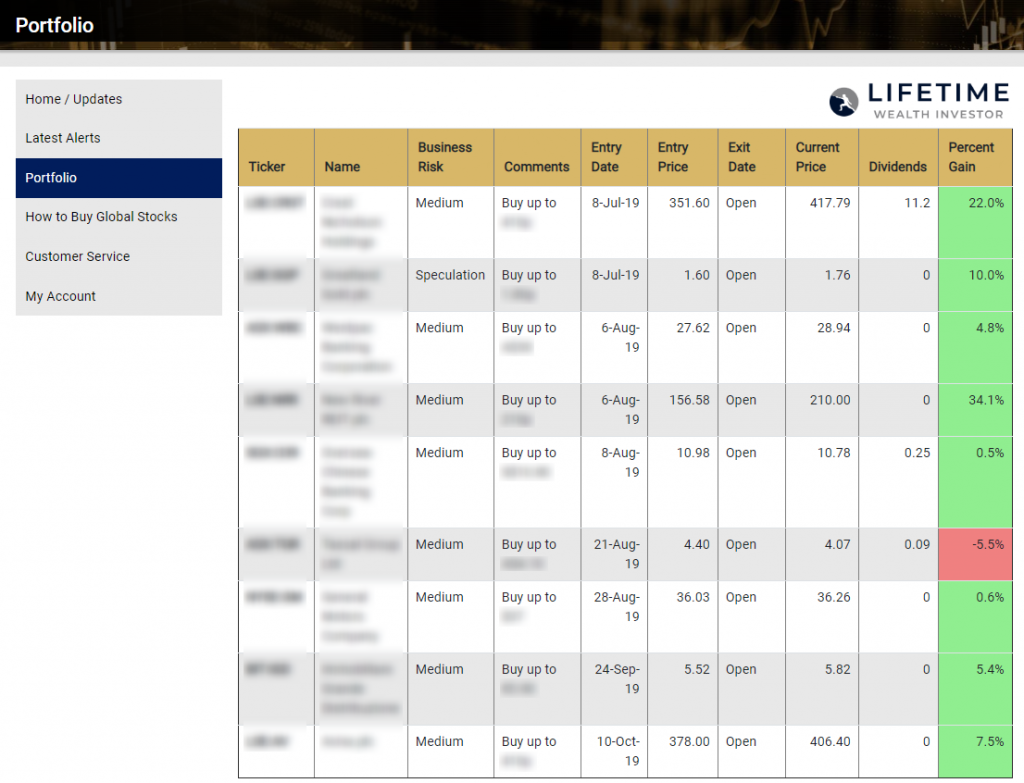

The Lifetime Wealth Investor portfolio that we’re recommending to our premium subscribers currently has a running yield of around 6% per annum. Meaning, even if the portfolio stands still, holdings of around a million dollars could still yield a living wage of about $60,000 per year.

Of course, dividends are not guaranteed. They can rise, fall or get cut altogether. So, as part of this work, we’re also monitoring the dividend policies and dividend cover of our target companies.

Dividends may also increase alongside favourable earnings, increasing the yield from the initial expectation.

Growing capital

The sweet spot is where you can both grow your income (yield from dividends), while growing your capital at the same time, while minimising risk to your capital.

Hedge funds approach this in a different way. They go long and short. They look for turnaround situations. Or macro events.

My favoured strategy in this volatile world environment is to use macro events to drive capital growth — with income.

For example, when we started Lifetime Wealth Investor, we recommended a number of positions that could benefit through Brexit volatility. What was happening on the London Stock Exchange (and with the pound) offered us the opportunity to capture a macro situation.

As I write, our lead position here is up over 30% (since recommending on 6 August 2019). It’s on track to pay dividends in excess of 10% per annum. And the capital invested has good preservation qualities, since the value of the shares is underpinned by specific property assets.

Please click here for more info and to join this research.

(Note: Past performance is not an indicator for future performance.)

Asymmetric returns

While much of the above strategy seeks to combine goals of capital preservation and income with growth, you’ll note we also have one ‘speculation’ stock.

In the early days of an exciting new business, there is sometimes the opportunity for asymmetric returns, where you could accelerate your capital at an extreme level.

For example, a2 Milk [NZX:ATM].

Had your purchased at 9c in March 2009 and held to the earlier high over $15 this year, you’d have enjoyed a return of over 16,000%. You could have turned $10,000 into over $1.6m !

But, in March 2009, you would have also taken speculative risk. You could have also lost your $10,000 if the hopes and dreams of the (then) young company failed to materialise.

Certain speculative opportunities like this can produce what is known as asymmetric returns.

The 1991 Gulf War is an excellent example of asymmetric return.

The American involvement in the war led to American casualties of 150, due to their superior technology and military prowess.The Iraqi side experienced casualties in the range of 30,000 to 56,000.

Iraqi casualties were expected. The American casualties — in relation to the scale of the war — were asymmetric.

Speculative stocks that can produce asymmetric returns are, of course, highly risky. They’re suitable only for the deployment of funds you can reasonably afford to lose.

We don’t focus on them in Lifetime Wealth Investor — but from time to time, we will highlight opportunities that may be of allocation interest in this regard.

So put your capital to work. Once you’ve done so, consider how your strategy combines the goals of capital preservation, income and growth.

Take a look at our Lifetime Wealth Investor portfolio.

Now is a great time to come on board.

Let us know what you think of this strategy?

Regards,

Simon Angelo

Editor, WealthMorning.com

Simon is the Chief Executive Officer and Publisher at Wealth Morning. He has been investing in the markets since he was 17. He recently spent a couple of years working in the hedge-fund industry in Europe. Before this, he owned an award-winning professional-services business and online-learning company in Auckland for 20 years. He has completed the Certificate in Discretionary Investment Management from the Personal Finance Society (UK), has written a bestselling book, and manages global share portfolios.