It was a question everyone was asking five years ago.

Should I buy power company shares during the government float?

I recall asking that question to a fund manager friend of mine.

‘I wouldn’t,’ he said. ‘They’re power companies.’

As if that classification guaranteed slow growth.

Then an old friend of mine I’d known since I was 13 asked me the same question.

I’d been thinking about it long and hard since the government announced the floating of Mighty River Power, Meridian, and Genesis.

At the time, I was working with a successful direct-response marketing company. I had a pretty simple view of business. If you had regular repeat customers that paid you good margins — it was a good business. Of course, the more the better.

Genesis Energy [NZX:GNE] alone has 650,000 customer connections across New Zealand.

Couple this with a simple view on the risk of shares.

Market movements are fine. Upswings and downswings on cyclical earnings are fine. Long-term demise and the business going belly-up is not.

When the New Zealand government owns 51%, the belly-up thing is pretty low-risk.

Then there’s the ‘in-farm rule’. If you’re going to get milked, you may as well share in the profits. In other words, if you’re a customer contributing to revenues, why not own a piece of the action too?

This is the reason I only fill up at Z Energy [NZX:ZEL], but that’s another story.

So, I told my friend I’d be buying Genesis.

In fact, I missed the boat. I should have maxed out on all three of the floats.

The float of the big power companies has put a significant number of Kiwis into shares. And by the looks of things, the power companies have been good to them.

How good?

The Genesis share issue price was $1.55 in 2014.

Today it’s $2.77.

The average dividend yield annually has been approximately 8%.

If you’d managed to get 5,000 shares in Genesis in 2014, you’d have made $6,100 in tax-free capital gain and about $4,240 in gross dividends.

On ‘the back of the envelope’, that’s an average annualised return of nearly 27% (capital gain plus dividends).

Where do you get 27% per annum with very little risk or downside?

One of the other floated power companies, of course.

What’s in store for the power companies?

Well, many of them are losing customers.

In the 2018 financial year, Genesis shed 2%.

They’re expensive. At least in NZ.

Right now, Meridian [NZX:MEL] trades at a PE (price-to-earnings ratio) of 46.5.

Compare that with another large renewables focused generator — SSE plc [LSE:SSE] in the UK, which trades at 18.24.

People are using less power off the grid.

We’re building more efficient homes and adding alternative energy sources like solar.

So why am I still hunting shares in electric utilities? [openx slug=inpost]

I feel about electricity the same way I feel about salmon. Limited stocks, production difficulties, and growing world demand.

Many analysts see demand being flat. They may be wrong. That’s leading to some well-priced electric stocks in other markets.

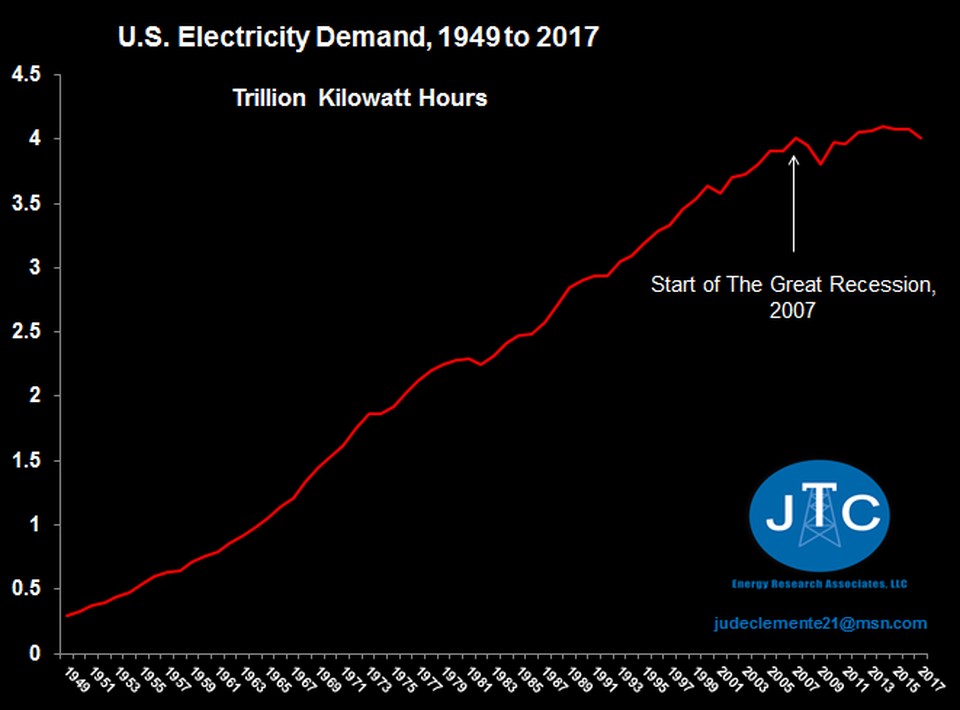

If we follow a big market like the US, electricity demand has flattened off since the GFC:

|

|

Source: EIA |

Consider the long-term, though.

Climate change

Here in Auckland, we’re having the hottest summer I can remember. Thermometers don’t lie. Climate change seems to be happening.

Last year, I put in a central air-conditioning system.

Now I’ve gone soft, and so have my kids. It gets us through balmy nights. And our summer power bills match our winter ones.

More and more people I talk to are sleeping with the AC on. And that’s only going to increase as climate change warms up.

Electrification

To combat climate change, a powerful movement is afoot to electrify fossil-fuelled transport.

That means electric cars, buses, trains, and short-haul aircraft.

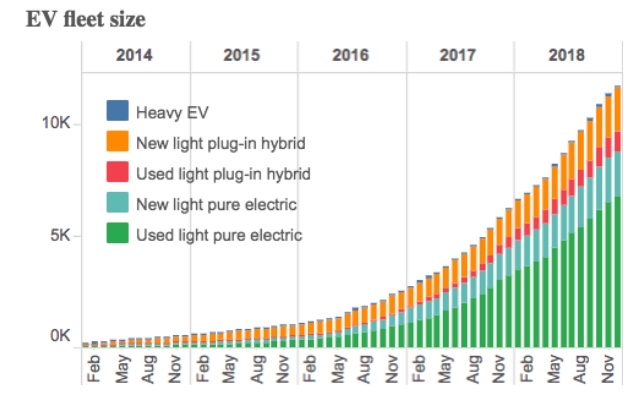

Look at the surging EV fleet size here in New Zealand:

|

|

Source: Ministry of Transport |

If our whole fleet went electric, we’d need to almost double our electricity generation capacity to cope. And my bet would be big producers like Genesis will grow on the back of this direction.

Population inclinations

There are two big trends we see in developed countries like ours.

- Continued population growth

- Popular demand to bring back manufacturing

Here in Australasia, we are somewhat insulated from the hollowing out of working incomes because we can achieve trade surplus by selling commodities. Dairy, meat, logs, iron ore.

More acutely, the US, Britain, France, Italy, and other big economies have felt the pain of offshoring and the savaging of real incomes.

Should anything threaten our cyclical commodity exports, we’d experience this even harder.

Trump and Brexit are the result of populist dissatisfaction — people are seeking a manufacturing renaissance.

There’s now loud demand for China to open up its markets, not just its factories. It’s starting to happen, and it’s going to change the way the world trades.

I’m not sure how this will go, but one thing’s for sure — a whole lot more power might be needed.

Regards,

Simon Angelo

Analyst, Money Morning New Zealand

Important disclosures

Simon Angelo owns shares in Genesis Energy [NZX:GNE], Contact Energy [NZX:CEN], Z Energy [NZX:ZEL] and SSE plc [LSE:SSE] (via wealth manager Vistafolio). Prices as at 13 Feb, 9:59 am.